Growth Prospects and Challenges Ahead for the U.S., U.K., Eurozone, China, and Japan

SUMMARY

- Truce, Not Peace

As announced at the G20 Osaka summit last weekend, trade talks between the United States and China will resume after a seven-week hiatus. This is a welcome development for Asian and European economies, which find themselves in the middle of the impasse. But turning this into something more permanent requires a concrete settlement on key issues, not a temporary truce. Experience shows this will not be easy.

In our base case, economic activity will remain subdued in major economies as tariffs will likely remain in place through 2019, maintaining downward pressure on global trade. In addition, geo-political tensions (most recently in Iran) are expected to remain elevated, limiting any rebound in sentiment. As a result, the world’s major central banks are likely to ease their policy stances to provide insurance against recession.

Overall, while downside risks to the global outlook have not increased, they haven’t declined, either. Following are our outlooks for the major countries/centers:

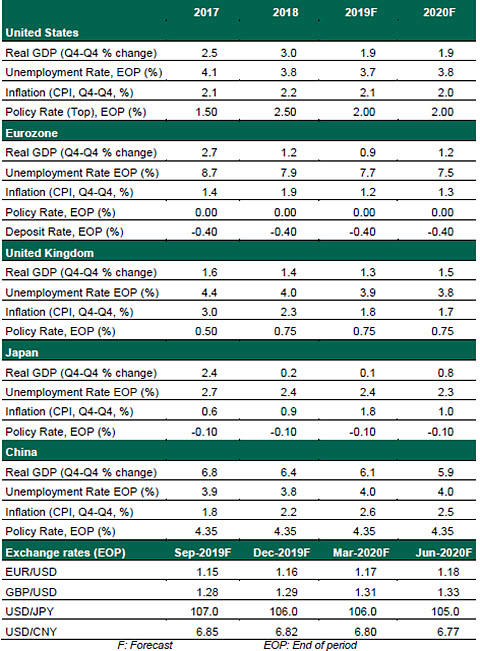

United States

- Economic circumstances are slowing but not yet contracting. The June manufacturing Purchasing Managers Index fell to 51.7, still expanding but not by a strong margin. Retail sales have yet to grow any faster than 3.8% year-over-year in any month thus far in 2019, a slower pace than was observed throughout 2017 and 2018. We expect economic growth to return to a more balanced pace of 1.9% year-over-year, near its long-run potential rate. Unemployment is likely to remain below 4%, while inflation should fall no further.

- The Federal Reserve has continued its rapid change in tone. In 2018, it raised overnight rates four times and ended the year by setting expectations for more. The Fed has since rescinded those forecasts and most recently set the stage for a cut. We expect to see two insurance cuts of 25 basis points each to the federal funds rate, in July and September, holding steady thereafter.

Eurozone

- The region appears to be flirting with recession, with Germany and Italy under particular stress. In view of persistently weak incoming data, we have revised our growth projections down for this year and next. We think recession can be avoided, if global trade tensions cool. A no-deal Brexit, U.S. car tariff threats and budget disputes between member states and the European Commission are the key downside risks.

- Continued industrial sector woes amid external exposures have reinforced European Central Bank (ECB) President Mario Draghi’s case for easing monetary policy. We expect the ECB to embark on an easing path using tools other than interest rates.