To cut or not to cut is no longer the question. Now the question is the quantity, magnitude and timing of rate cuts for the rest of the year.

This week was an important one in that we were privy to several important Fed speeches as well as some informative data about the state of the economy. The takeaway in aggregate was muddled. On one hand we had both Chairman Powell as well as St. Louis Fed President Bullard hinting that the Fed would start with a 25bps point cut in July. This came as a bit of a disappointment because Powell last week during his press conference indicated a 50bps cut in July could be in the cards. Bullard did say that another cut later in the year (read October or December) could be warranted, but this was somewhat of a disappointment for markets since Bullard is one of the most dovish of Fed policy makers.

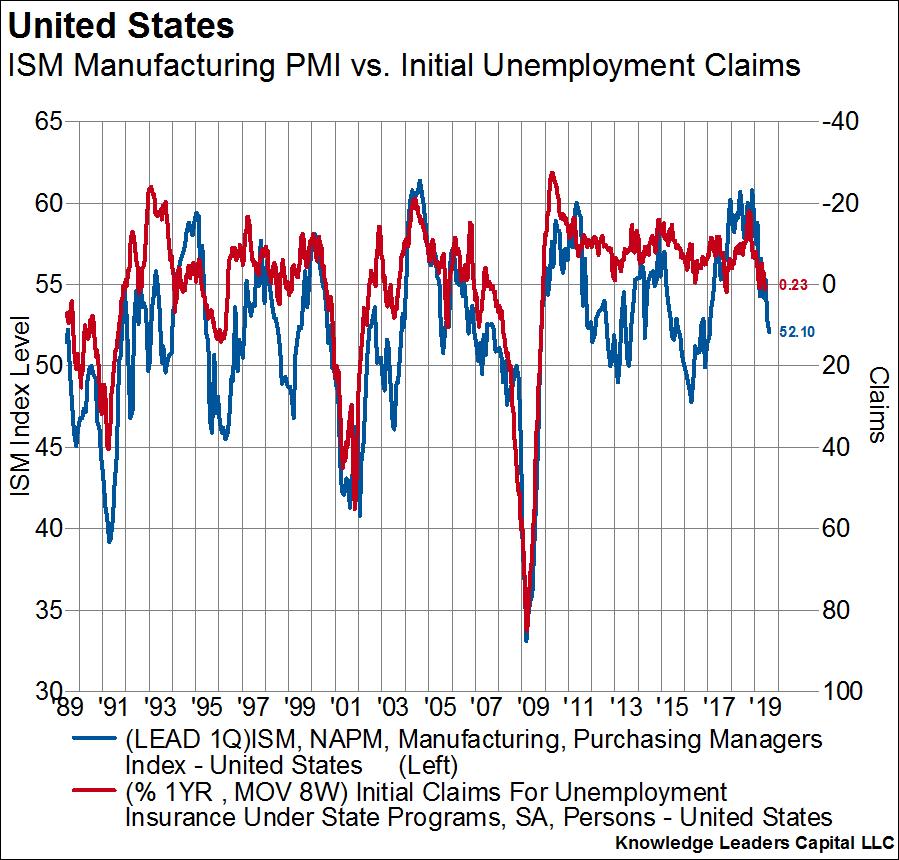

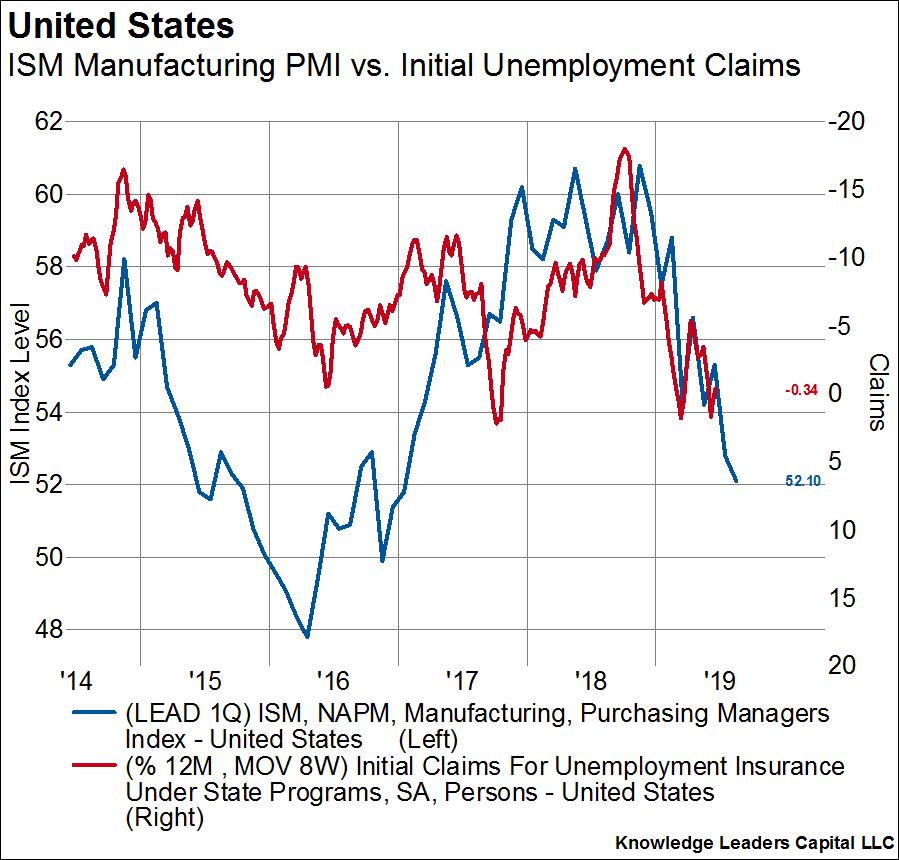

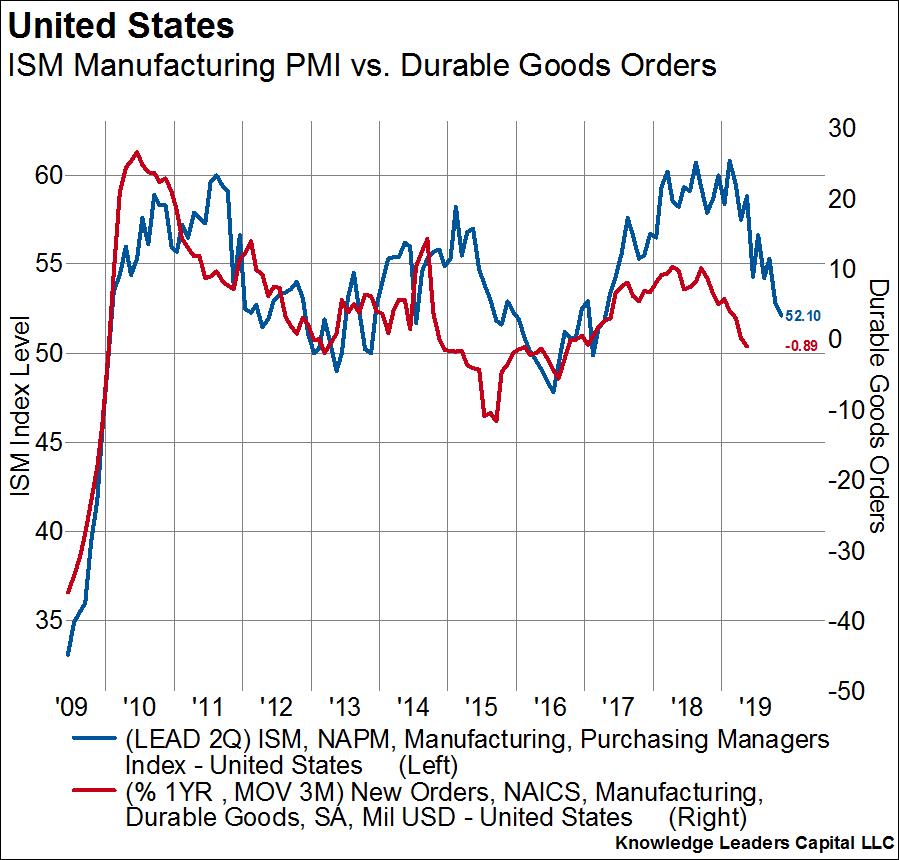

On the other hand, data has continued to come in on the weak side including durable goods orders and initial unemployment claims that both missed expectations. Data misses like we have seen this week would warrant a far more aggressive rate cutting campaign than what is being signaled by the Fed currently.

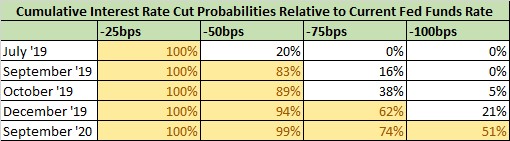

Where there is less ambiguity is what the market is expecting – and the market appears to be much more in line with the incoming economic data and the future trajectory of that data than the Fed, as we will show. Currently, the market places a 100% probability on a cut of at least 25bps points in July and a 20% probability of a 50bps cut. Those odds are in line with the Fed speeches this week. Moving ahead, the market places an 83% probability that the Fed Funds rate will be 50bps lower than today by September – well ahead of Fed signaling. By December the market assigns a 62% probability that the the Fed Funds rate will 75bps lower than today and by next year the market is pricing greater than a 50% probability than the Fed Funds rate will be 1% lower than it is today. Therefore, the market is placing higher odds on 75bps of cuts in 2019 than 50bps of cuts, and at the same time the market is expecting another 25bps of cuts in 2020.

So what path of policy is the more likely outcome, the Fed’s or the market’s?

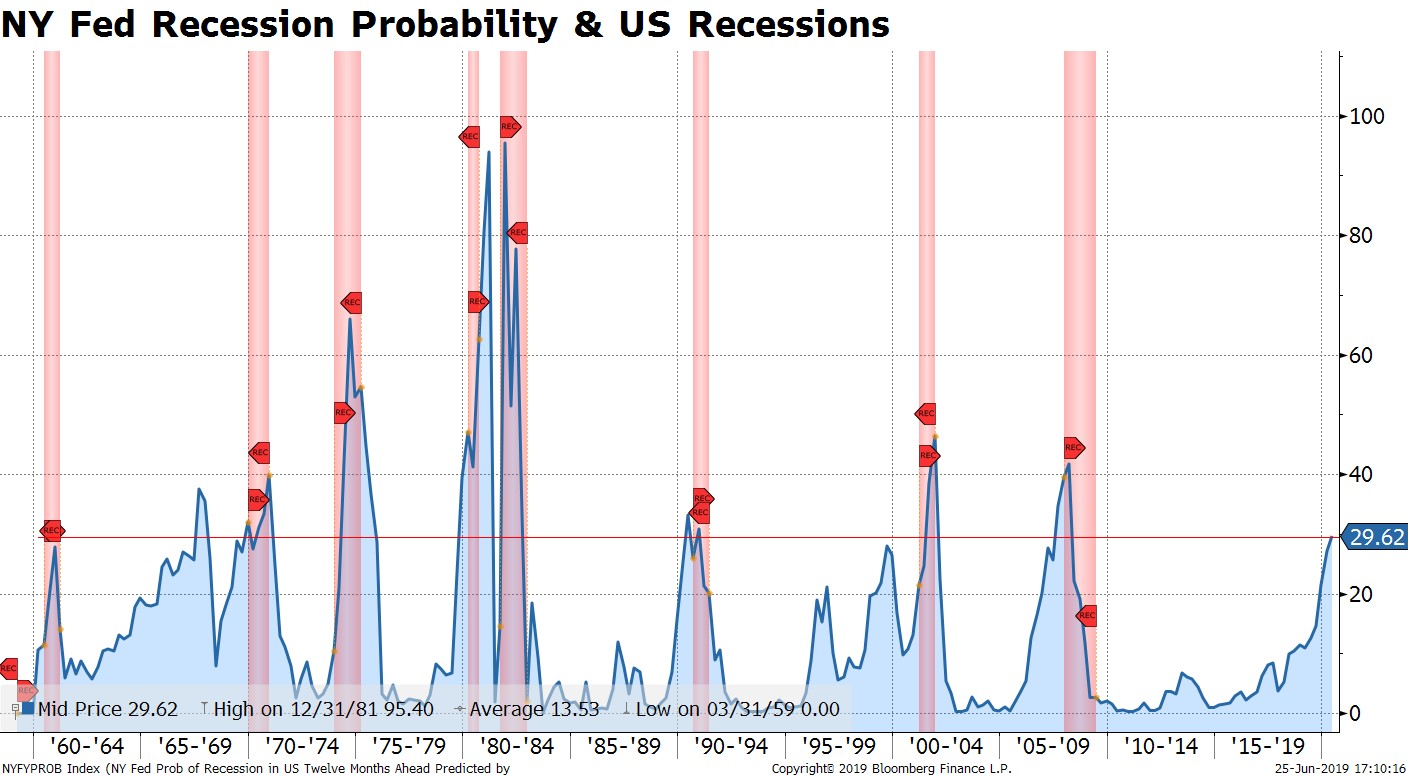

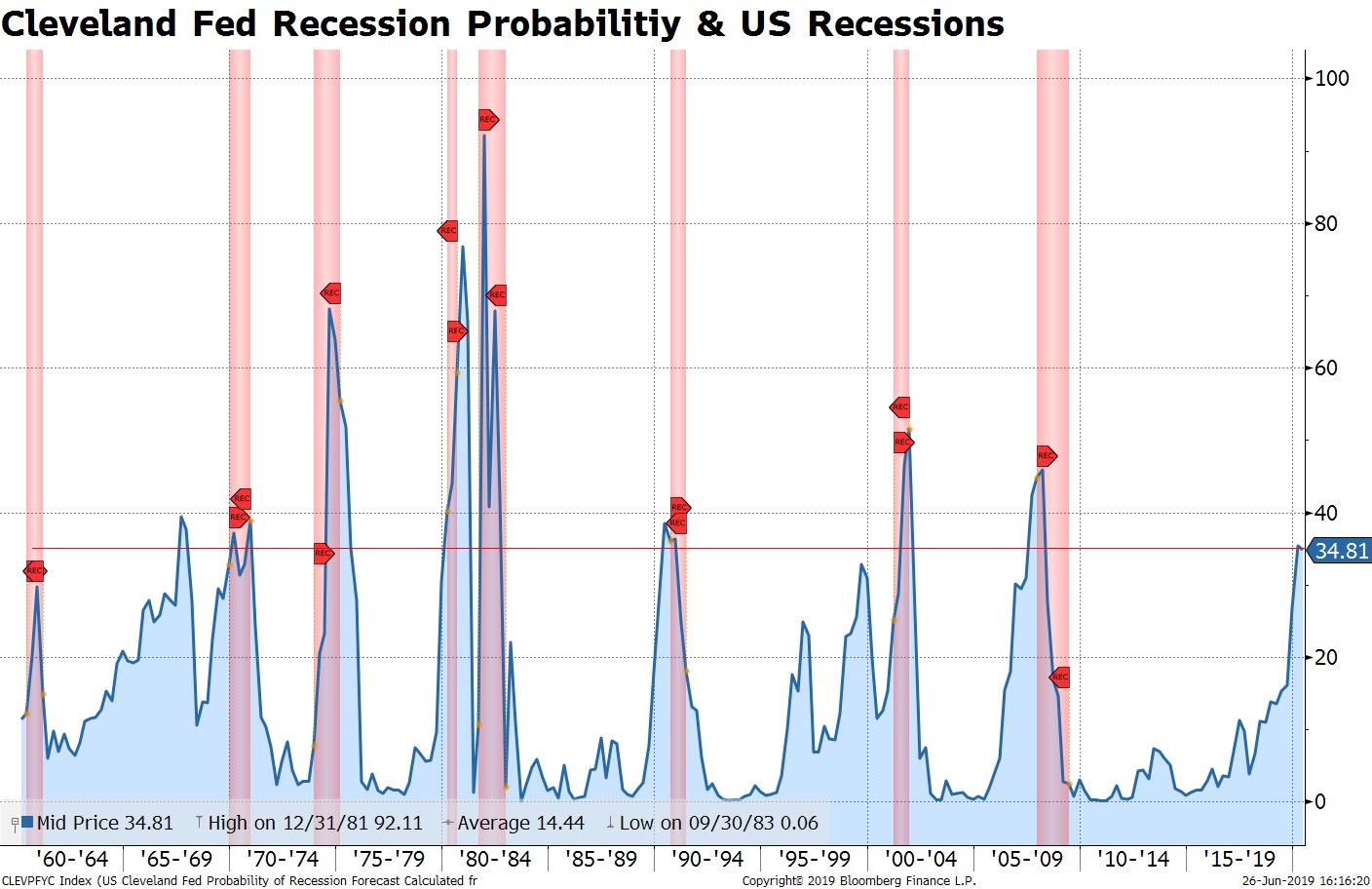

Let’s start with recession probabilities as published by the New York and Cleveland Fed offices. Based on the shape of the 10Y-3M yield curve, the New York Fed’s recession model predicts a 29.6% of a recession within the next 12 months. A probability of 29.6% by this model is relatively high and readings this high have preceded recessions every time but once (in 1967). The Cleveland Fed’s model incorporates the yield curve as well as GDP growth and is pointing to an elevated 34.8% of a recession in the coming 12 months. Here again, only once (in 1967) did the model predict a higher probability of a recession and a recession did not come. These models were correct in predicting 8 of the last 9 recessions for an 88% batting average. Of further importance is that the smaller spikes in recession probability in 1996 and 1999 that did not result in immediate recessions occurred after the Fed had provided some “insurance” rate cuts. The recession probability is higher today than it was in either of those two instances and the Fed has not yet started the rate cutting cycle. This indicates that the Fed needs to act sooner rather than later and probably to a degree that is larger in magnitude than their base case calls for.