Summary: SPX made a new all-time high (ATH) last week. DJIA and NDX were not far behind. And the broadest measure of the US stock market comprising 98% of stocks came just 0.1% shy of a new ATH.

By contrast, small caps are lagging. They have retained none of their gains made over the past 1-1/2 years and haven't been close to a new ATH in 10 months. Should investors be worried?

By most measures, the answer is probably not. Small cap underperformance has more often marked a low in SPX, not a high. Investors should be more worried when small caps - which are highly speculative and high beta - lead, as this has most often been a feature of major bull market tops, the reverse of the situation we have now.

Last week, SPX made a new all-time high (ATH). The DJIA equaled its ATH from October 2018 and NDX came within 1% of its ATH from just last month. The broadest measure of the US stock market, the Russell 3000, which comprises 98% of stocks, exceeded its May high and came within 0.1% of its October 2018 ATH. By most measures, US stock prices are doing well. Enlarge any chart by clicking on it.

So naturally some investors are highlighting the relative weakness of the small cap index, the Russell 2000, which is lagging every other index. It's currently 12% below its ATH from August 2018, under both its 50-d and 200-d and has retained none of the gains made since November 2017, 1-1/2 years ago.

There's no doubt that RUT is weak and that investors in small caps should take note. But should investors in the broader market care more about the weakness in RUT or the strength of the other indices?

Fund managers interviewed by Bloomberg believe they should care more about RUT, calling small caps a good barometer on the economy and a leading indicator for the broader indices (that article is here).

In particular, the relative weakness in RUT versus the broader market is highlighted as being prescient of domestic economic weakness that usually presages a fall in the large cap indices.

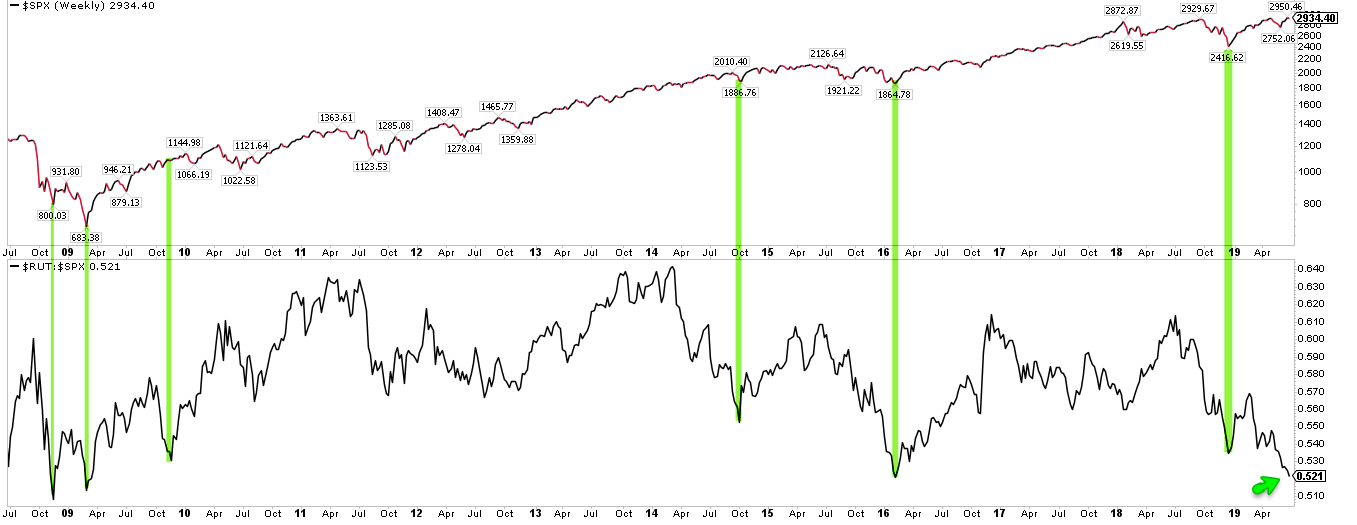

In truth, however, that has usually not been the case. The next chart shows those times in the past 11 years where RUT has significantly lagged SPX (the lower panel is the same as the chart above). Most have not signified valid economic weakness and SPX (upper panel) has, in fact, been near a low.

Going back further, it is also hard to make the case that RUT has been a useful tell for the economy or the broader market. Most of the 1990's boom (green arrow) was accompanied by persistent underperformance in small caps (red arrow). That divergence lasted 6 years. Moreover, the exact final top in 2000 came after a year in which small caps strongly outperformed (circle).

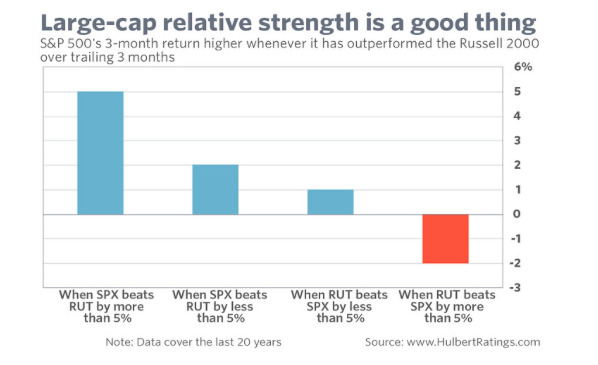

That RUT's underperformance should not be a primary concern is further shown by two studies from Mark Hulbert.

First, SPX has done much better when it leads RUT than when RUT leads SPX. In fact, RUT leadership has been market negative.

Second, in the 29 bull market tops since 1926, RUT has peaked after SPX in more than half the cases. That means that strong outperformance by RUT now, after SPX's recent ATH, would be a concern. A lagging RUT has marked a top in the broader stock market in just 1/3 of these cycles. Recall that RUT last made an ATH 10 months ago.

What's going on here?

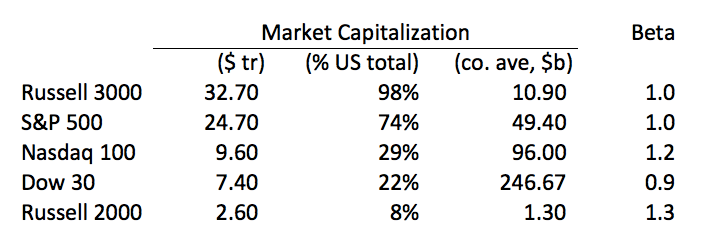

First, RUT is a much smaller index than SPX, DJIA or NDX. SPX represents about 74% of the total market capitalization of US equities. RUT is just 8%. The 6 largest components of DJIA have a greater combined market capitalization than all 2000 components of the RUT. It's not clear why a small subset should be expected to provide more useful insight on the health of US equities than SPX itself.

Second, RUT comprises 2000 companies with an average market capitalization of $1.3b. For the 500 companies in SPX, the average is nearly $50bn. These are small companies, much less followed by Wall Street analysts, in turn making them more speculative. The average beta of RUT is about 30% higher than SPX. This is key. When investors are bullish, you should expect RUT to outperform SPX, as it has most often done into an important top. The reverse is also true when investors are bearish; investors sell speculative small cap stocks into an important low.

Finally, it's worth putting the recent underperformance of RUT in perspective. The index's performance is in line with SPX since both the October 2007 bull market top and the March 2009 bear market bottom. Since then, periods of outperformance have been followed by periods of underperformance. In other words, what we are seeing now could well be nothing more than mean reversion, similar to mid-2010, mid-2011, early-2016 and late-2018.

In summary, the main stock indices in the US are near their ATHs. The small cap index is the exception. Their underperformance has most often marked a low in SPX, not a high. Investors should be more worried when small caps - which are highly speculative and high beta - lead, as this has most often been a feature of major bull market tops, the reverse of the situation we have now.

© The Fat Pitch

More ETF Topics >