The “rise of the middle class” has been a ubiquitous theme touted by emerging market (EM) investors for several years. In reality, upward social mobility and the emergence of a middle class in EM has been largely confined to China over the past decade. Given that China’s significance in the emerging world tends to obfuscate everything else when it comes to EM-related generalizations, it is not surprising that this misperception has taken root.

In this, the first in a two-part series on False Narratives in EM Equities, we demystify what the “rise of the middle class” truly means in an EM context. In part two, we delve into the controversial claim that emerging markets are the growth engine of the world.

“Companies, not countries,” we contend, is the narrative that should drive investment in emerging market equities. That said, neither narrative detracts from the fact that for long-term investors, we believe emerging markets provides a multitude of opportunities. As active, bottom-up investors, we focus on high-quality companies with sustainable advantages and options that are positioned to manifest over time. While these extraordinary companies are rare, they exist throughout the emerging markets. However, we believe that most investors’ adherence to false narratives clouds their ability to identify those unique opportunities, which creates an advantage for managers willing to take a more idiosyncratic approach over the long term.

What Constitutes the Middle Class?

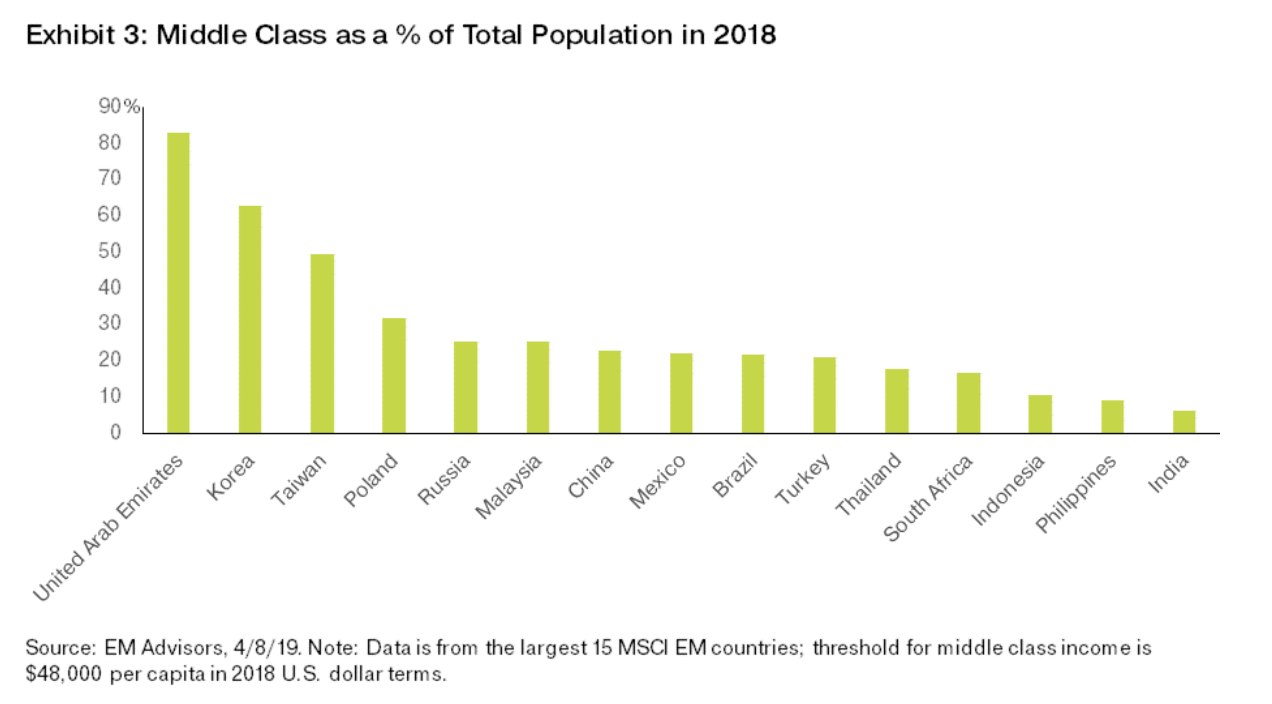

Defining the term “middle class” is problematic, as there is no consensus. There is simply no authoritative way to develop consistent estimates across the heterogeneous landscape of EM economies as each has its own structural quirks in terms of income distribution and inequality. Countries like Qatar (which boasts the highest GDP per capita in the world) and the United Arab Emirates with small populations and lots of hydrocarbons distort the picture as they are very rich. East Asian countries with strong manufacturing bases and proximity to China are closer to developed nations in some respects. With a GDP per capita of approximately US$32,360 and US$24,400, respectively, South Korea and Taiwan have enjoyed such strong economic growth that they are as rich as developed markets like Italy and Spain.1 However, while there is little agreement on an approach to measuring the middle class in emerging markets, the trends evidenced by the data are strikingly similar.

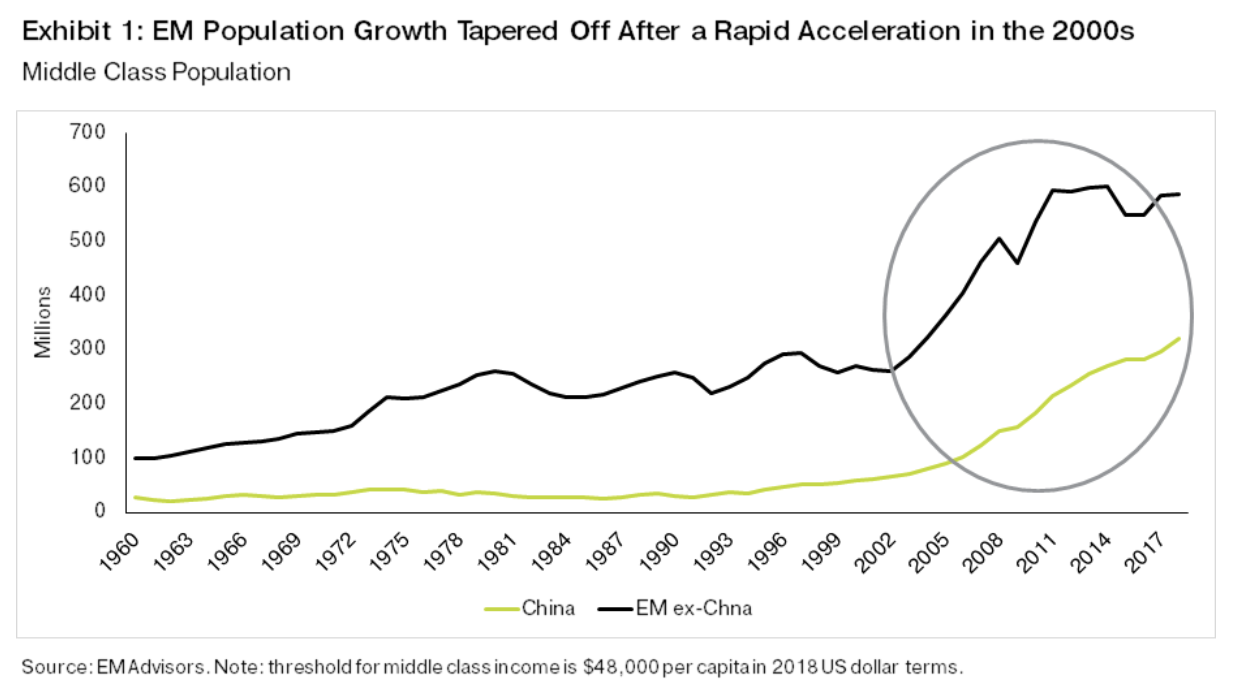

For example, EM Advisors Group uses a threshold of $48,000 per household2 to determine the size of the middle class in EM. The World Data Lab’s Homi Kharas defines a four-person middle-class household as one that earns between $14,600 and $146,000 (in 2011 purchasing power parity terms). While these two organizations come to somewhat different conclusions about the ultimate size of the middle class, both show that there was modest growth in the 1990s followed by a huge acceleration from 2000-2010, before leveling off after 2010.

EM’s Missing Middle Class

While people often look around the emerging markets for a repeat performance of China’s economic boom, in reality the overarching theme of a broad, rising EM middle class scarcely exists. Rather, optimism about this theme was largely conjured up by investors and multinational corporations that observed the nascent expansion of discretionary income in EM and extrapolated it into the next big opportunity across the entire asset class.

In absolute terms, most of the outsized gains in the EM middle-class population were posted in China and India, accompanied by a handful of their Asian neighbors including Vietnam, South Korea (arguably a “developed” country), and the Philippines. Meanwhile, large EM countries like Russia, Brazil, Turkey, Mexico, South Africa, and Argentina saw only a small uptick in growth in their middle class relative to total population over the past two decades.

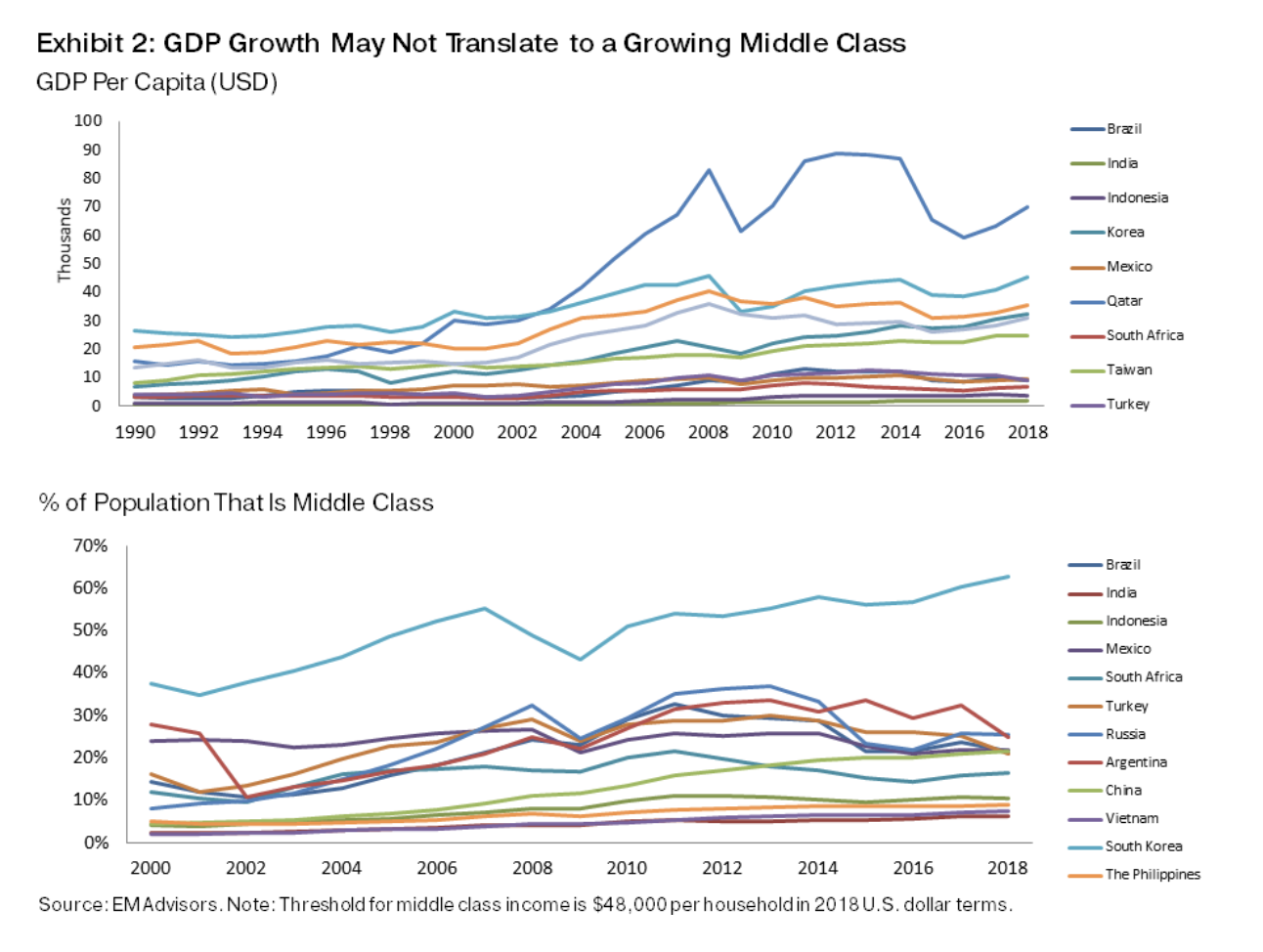

Investors have been searching across EM for a replica of China’s economic boom. To many, India seems like the obvious heir apparent. But the chances of India developing a middle class to match China’s are, in our view, distant and unlikely. The social progress behind middle class expansion is the result of a rare combination of faster economic growth and falling income inequality. India’s middle class accounted for only 9% of the total population in 2018, up from 5% in 2000, and its GDP per capita is one-fifth of China’s at just under $2,000. But India’s uninspiring per capita GDP growth reflects the country’s remarkably deep-rooted problems of income inequality and a dual-track economy. While its middle class are far from wealthy, the rich are truly rich – there are over 200,000 millionaires in India.

India is not analogous to China, and it still faces considerable challenges on its journey to becoming an industrialized, modern economy. However, it has enormous potential to grow into a significant regional economic power over the next 10 to 20 years, driven by increasing capital investment, urbanization, and its capacity for significant labor absorption into the formal sector, which currently employs only one-fifth of the population. In addition, India has relatively high levels of domestic savings, averaging 32% of GDP over the past five years, with which it can fund much needed investments in infrastructure and capital stock.

Mexico is the second largest economy in Latin America, behind Brazil. After a decade marked by the start of NAFTA, the tequila crisis and multiple recessions, the share of Mexico’s middle class to total population has stabilized at around 20%. Mexico’s oligopolistic structure leaves it with a rising concentration of wealth in the hands of a few families. The top 10 Mexican families account for more than a fifth of its total stock market value3 – one of the highest concentrations throughout EM.

Similar to India, Mexico has a sense of urgency to bring its informal economy into more productive, modern sectors. Close to 57% of the employed population are working in the informal sector.4 And amid high rates of informality, low productivity growth, and the shock of the 2008 financial crisis, wage composition has deteriorated markedly since 2008, stalling the growth of its middle class.

We see hope in Mexico – and perhaps much of the developing world – in the potential for a fintech revolution. Low credit penetration across the developing world reflects constraints on funding, rather than an absence of demand. In our opinion, fintech has the potential to reach the 50%-plus of Mexico’s population that does not have access to formal bank accounts, bringing greater funding into the system that can be intermediated through banks. And through the modern wonder of the fractional reserve banking system, savings and investment can grow potentially much faster (and more sustainably).

Brazil, a country that has always been known for its socioeconomic inequality, saw a promising rise of its share of the middle class in the 2000s. After peaking in 2011 at 33%, however, the country began a dramatic reversal and, today, Brazil’s middle class accounts for less than 22% of the total population.

There is no doubt that Brazil’s economic expansion in the 2000s pulled a huge number of low-skilled workers out of the informal sector and into jobs in services and construction. While labor income inequality fell, however, it was not enough to offset the growing accumulation of wealth in the hands of the elite. According to the World Wealth and Income Database, between 2000 and 2015, the share of income in the bottom 50% of earners rose from 11% to 12%, reflecting only 18% of the country’s total income growth during that period. The top 10% grew their share of income from 54% to 55% – from a substantially larger base, of course. While the elites and the poor made gains, the middle 40% saw their share of income decline from 34% to 32%, posting less growth than the average for the whole economy.

Brazil remains gripped by recession and continues to generate political noise and volatility, while exhibiting deteriorating external imbalances, low inflation, and falling interest rates. The opportunity for reform to address the economy’s two fundamental problems – low savings and structurally unsound fiscal balances – is percolating. We see clear evidence of a willingness in government and society to undertake material hard decisions to improve social mobility and growth potential across income classes. We will see if Brazil’s messy democracy can deliver.

The issue of the “squeezed middle” is mirrored in other large EM countries such as South Africa, where the middle class as a share of total population has shrunk from 22% in 2011 to around 16% in recent years. Over in Southeast Asia, a whole host of countries are poised to embrace a once-in-a-generation opportunity to compete for labor-intensive, manufacturing-led export growth, which has been hugely instrumental in fostering China’s own economic miracle. But the growth of their middle class as a share of national population remains largely anemic across these countries.

The Exception that Is China

Since the turn of the century, China’s middle class has grown from 5% to over 20% of the total population,5 or a continent-sized c.300 million people. This represents more than 35% of the entire middle class population across emerging markets, and its share will continue to increase as growth in the rest of EM has stalled. At present, China almost singularly represents the rise of the EM middle class.

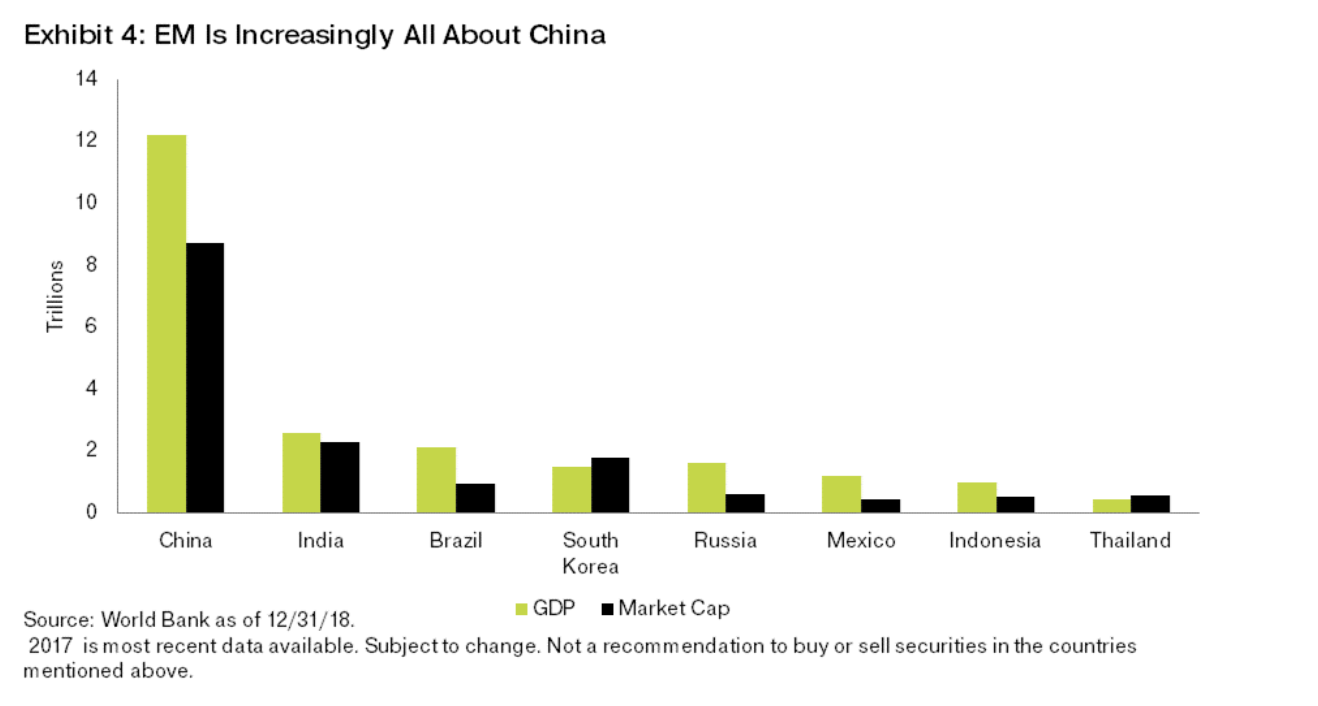

China’s meteoric rise in the 2000s was the most striking example of the benefits of opening up an economy to global markets and introducing major structural reforms. In the midst of the slowdown throughout EM, China stood apart. To be sure, as its twin engines of growth – infrastructure/real estate investment and exports – fade, the country’s overall growth has slowed. But this is largely by design, and an inevitable outcome of a healthy rebalancing to an economy led by domestic consumption. Indeed, growth in China will continue to slow. The popular myth that China’s GDP has to grow by 6%-7% or higher is inherently flawed. Even at a 5% pace, China will account for 30%-40% of global GDP growth; and at US$12 trillion, China’s economy is larger than all of Africa, Latin America, and India combined.6

We are unlikely to see a “next China” growth story out of any EM given the profound depth and size of the economic expansion unleashed over the past three decades through a combination of powerful reforms, urbanization, and the massive expansion of trade, property market development, and significant capital formation.

Where to From Here?

The prevalence of dual-track economies is a core obstacle for middle class expansion and social mobility improvement, and therefore EM growth. This will be addressed in detail in a subsequent blog, but in short, the prevalence of oligopolistic and rent-seeking behaviors in EM means that crony capitalists and a limited formal-sector workforce capture a disproportionately large share of economic expansion. Economic growth is constrained as the mass poor tend to have a higher propensity to spend as their wealth increases, particularly in consumer discretionary categories.

Still, we end with a more optimistic macroeconomic outlook for the next decade, driven by the politics of change presently developing across the EM landscape. There is hope on the horizon. For the first time since the Asian Financial Crisis in 1997, a deep aspirational yearning for change oriented toward better social mobility and conditions for growth is surging in EM.

As new leaders in many EM countries come to power – more a progressive movement than a populist one in our view – the next decade looks exciting. The stage is being set for another bout of structural reforms, which increases the potential for endogenous growth in markets where globalization may no longer be the solution.

Our Philosophy

Understanding the economic growth implications of an underdeveloped EM middle class is interesting, but it does not affect our core approach to investing. While most investors focus on credit cycles, elections and one-off events (the noise), and have a tendency to flock to prevalent macroeconomic predictions, we remain focused. Over the history of this Fund, we have been able to uncover opportunities, even in low-growth economies, that have generated superlative returns.

Our focus is on finding idiosyncratic companies with sustainable competitive advantages, durable growth, and a host of real options that will emerge over many years. In the absence of favorable macroeconomic backdrops, two types of high-quality companies tend to have the intriguing potential of gaining vast ubiquity and, in turn, outperforming over the long term.

The first type are companies that have established a large overseas market. This applies to Novatek, a Russian-listed private gas company, which we have owned for 11 years (and counting). The company built all its assets from scratch and has transformed itself multiple times over the last twenty-five years to become Russia’s second largest domestic gas producer. Its technological edge allowed it to discover condensate – essentially a wet gas that is more profitable than domestic gas. And a second miracle – success in developing the LNG industry in one of the most inhospitable places on earth, the Yamal Peninsula – sets it apart from any global competitor. We are at the beginning of a massive LNG revolution as China and other parts of North Asia want a reliable, economic source of clean energy. Novatek not only began unlocking vast Arctic hydrocarbon resources, but also commercially introduced a completely new sea passage, the Northern Sea Route, which is the shortest destination from Russia’s Yamal to LNG-hungry China. Despite its home country’s sluggish growth of 1%-2%, Novatek embraces a much more intriguing set of real options in the global market.

The second type of idiosyncratic companies are those offering competitive advantages in terms of scale and efficiency, which they leverage to introduce new business models. Mexico’s Femsa, the largest coke bottler in Mexico, falls into this category. Given that the economy is growing at 2%-4% annually, we do not anticipate a discretionary income boom in Mexico’s domestic consumer market. However, by introducing an innovative convenience store operation called Oxxo, Femsa is taking market share from independent stores. Today, Oxxo is by far the largest convenience store chain in Mexico. Subsequently, Femsa continues to roll out new store formats, including drugstores and fuel stations within Mexico and across Latin America, which together with Oxxo, provide a long growth runway for the company.

We invest in extraordinary companies, not countries, meaning that we focus on unearthing companies with sustainable advantages and underappreciated options, that are focused on long-term earnings. In the midst of stagnant economic conditions, extraordinary companies stand out and have the potential to gain market share because of their efficiency and competitive advantages.

Source: 1 EM Advisors Group, as of 2018, the GDP per capita was US$35,200 and U$31,000 for Italy and Spain, respectively.

2 US$12,000 per person, or US$48,0,00 for a family of four in current US dollar terms.

3 HSBC estimates, 3/5/19.

4 National Survey of Employment and Occupation, as of 4Q 2017.

5 EM Advisors designation, 4/8/19

6 World Bank as of 12/31/18, 2017 is the most recent data available.

Important information

The opinions referenced above are those of the author. These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

Holdings are subject to change and are not buy/sell recommendations.

Because the Fund may hold a limited number of securities, a change in the value of these securities could significantly affect the investment value of the Fund.

The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

The Fund is subject to certain other risks. Please see the current prospectus for more information regarding the risks associated with an investment in the Fund.

Invesco Distributors, Inc., and Invesco Canada Ltd. are indirect, wholly owned subsidiaries of Invesco Ltd.

Invesco Oppenheimer Developing Markets Fund Top 10 Stock Holdings by Issuer

All holdings are as of 3/31/19, and subject to change.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Justin Leverenz, Team Leader and Senior Portfolio Manager

Justin Leverenz is a Team Leader and Senior Portfolio Manager for the OFI Emerging Markets Equity team at Invesco.

Mr. Leverenz joined Invesco when the firm combined with OppenheimerFunds in 2019. He joined OppenheimerFunds in 2004 as a senior research analyst. Prior to joining OppenheimerFunds, Mr. Leverenz was the director of Pan-Asian technology research for Goldman Sachs in Asia, where he covered technology companies throughout the region. He also served as head of equity research in Taiwan for Barclays de Zoete Wedd (now Credit Suisse) and as a portfolio manager for Martin Currie Investment Managers in Scotland. He is fluent in Mandarin Chinese and worked for over 10 years in the greater China region.

Mr. Leverenz earned a BA degree in Chinese studies and political economy and an MA in international economics from the University of California. He is a Chartered Financial Analyst® (CFA) charterholder.

More Fixed Income Topics >