Trade tensions caused investors to back away from emerging markets in May, but there are many reasons to be optimistic about the asset class and the earnings outlook ahead, according to Franklin Templeton’s Emerging Markets Equity team. The team outlines recent news and events influencing the market and where pockets of potential opportunity might be found.

Three Things We’re Thinking About Today

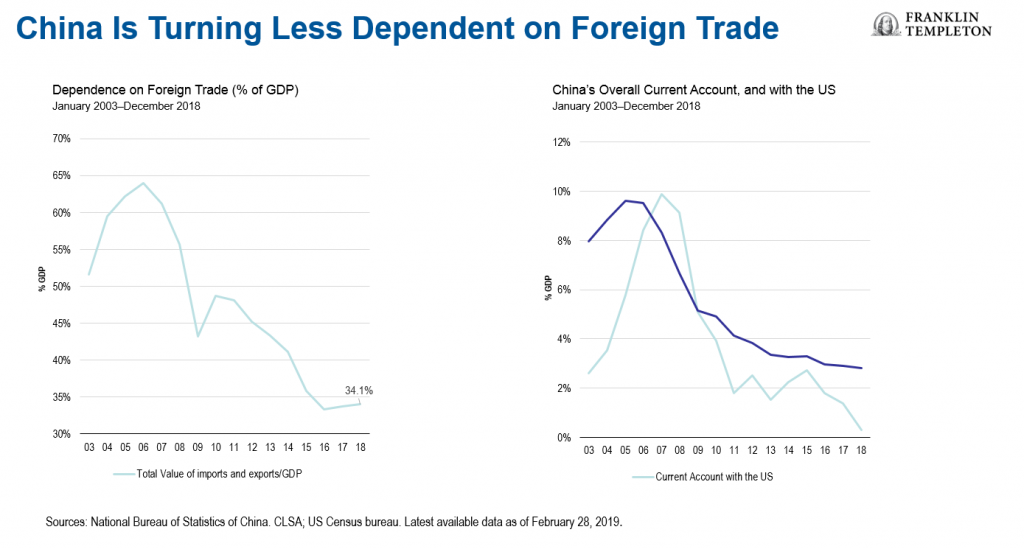

- Market sentiment turned negative in May, when concerns emerged of an escalation in the US-China trade war following US President Donald Trump’s decision to impose a 25% tariff on US$200 billion in Chinese imports, followed by China’s announcement that it will impose new tariffs on US$60 billion of American goods in response. The decision to include Huawei in the US Entity List only further acerbated the situation. Undoubtedly, the increase in tariffs will impact many Chinese producers, with some companies already shifting manufacturing to other countries. However, China is turning less dependent on trade—at present about a third of its gross domestic product (GDP) comes from foreign trade compared to almost 65% more than a decade ago.1 Instead, the key underlying drivers of China’s growth have been shifting toward innovation, technology and consumption. If China’s rebalancing efforts result in an economy that is more sustainable, in our view, it would almost certainly continue to be a structural growth driver for emerging markets (EMs) in the decades to come.

-

MSCI’s semi-annual rebalancing, which was accompanied by the inclusion of Saudi Arabia in the MSCI Emerging Markets Index2 and the reclassification of Argentina from frontier market (FM) to EM status, took place on May 28. MSCI also increased the inclusion factor of China A shares to 10% from 5%, doubling its index weighting to just under 2%. A change in methodology also led Thailand’s weighting in the MSCI Emerging Markets Index to increase to about 3%. MSCI’s decision to upgrade Saudi Arabia to EM status puts it firmly on the radar of international investors, and in our view, is a positive step for the Middle East region’s transition into mainstream EM investment. Following its addition to the FTSE Emerging Markets Index last year, Kuwait is on MSCI’s watchlist, with an announcement for upgrade expected shortly. The rebalancing likely led to portfolio inflows into these markets from passive investment strategies, while markets which saw their weightings trimmed, such as South Korea and Taiwan, saw outflows. Active portfolio managers, however, have more flexibility and can focus on company fundamentals as opposed to being restricted by market index weightings.

-

Russia remains one of the most undervalued markets globally, in our view, despite a very strong performance over the past three years. Many international investors have avoided this market because of economic sanctions against the country. However, we believe Russia’s fairly self-sustained economy has limited the impact of sanctions. While the economy has proven to be resilient, we have seen many companies take steps to adapt and flourish in the current environment. In some cases, restricted access to Western technology has spurred Russian companies to invest in building their own ecosystems, which contributes to more sustainable growth. Moreover, corporate governance in many Russian companies has improved significantly. For example, many companies have increased dividend payouts and undertaken share buybacks to improve shareholder value. Overall, we believe Russia continues to offer interesting opportunities for investors and exposure to select well-established companies across the information technology, financials, energy, materials and consumer-related sectors could serve well for diversified EM mandates.

Outlook

EMs have generally performed well over the last three years, with the MSCI Emerging Markets Index returning over 30% during the period.3 However, we believe the asset class still has significant potential, especially after the correction last year and in May.

Following the realization of some earnings shortfalls, we expect to likely see superior corporate performance next year. We believe 2020 could be a strong year for EM earnings based on cyclical recoveries that have started to emerge.

This outlook, of course, is not withstanding the recent trade conflict. In the near term, with the increase in tariffs, some repercussions can be expected. However, over a longer period of time, we think markets and companies will adjust and as they do so, earnings should likely recover as well.

We are of the opinion markets have also started to factor in these issues, and there remains scope for an agreement that could satisfy both the United States and China. In the meanwhile, we think there is an opportunity for many other companies and countries to potentially benefit from this trade tension.

Emerging Markets Key Trends and Developments

An unexpected spike in trade tensions and renewed global economic growth concerns in May caused EM equities to notch their first monthly loss of the year. EM stocks fell more than their developed market peers amid capital outflows and broad currency weakness against the US dollar. The MSCI Emerging Markets Index decreased 7.2% over the month, compared with a 5.7% decline in the MSCI World Index, both in US dollars.4

- Asian equities tumbled in May as a re-escalation of US-China trade tensions weighed on investor sentiment. Markets in China, South Korea and Taiwan were amongst the weakest regional performers. Washington raised tariffs on US$200 billion of Chinese imports and imposed sanctions on Chinese telecommunications company Huawei, while Beijing hit back with higher tariffs on US$60 billion of US goods. Fears of a potential US-China technology war weighed on technology heavyweights in South Korea and Taiwan. Bucking the downtrend, stocks in the Philippines and India rose modestly. The Philippine central bank reduced its benchmark interest rate and the reserve requirement ratio for banks to support the domestic economy. In India, Prime Minister Narendra Modi secured his second term in office as the Bharatiya Janata Party emerged victorious from the country’s general election.

- Although Latin American markets declined as a group, the region outperformed the broader EM asset class on the back of positive performances in Argentina and Brazil. The Argentine market ended May with a double-digit gain supported by its inclusion in the MSCI Emerging Markets Index. Progress on the social security and tax reform front and an improving political climate eased investor concerns in Brazil. Economic activity, however, remained weak with first-quarter GDP growth easing to a two-year low. At the other end of the spectrum, markets in Colombia, Chile and Mexico declined. Disappointing economic data and a hawkish central bank weighed on equity prices in Mexico. US President Donald Trump’s announcement of a progressive tariff on all Mexican exports to the United States at the end of the month further weighed on investor sentiment.

- While the Europe, Middle East and Africa (EMEA) region performed better than its EM and developed market counterparts, most markets still ended the month in negative territory. Russia and Greece recorded gains, while Saudi Arabia, South Africa and the United Arab Emirates declined the most. The Russian market was one of the top EM performers in May, driven by its undemanding valuations and a search for investment opportunities believed to be relatively more insulated from the US-China trade conflict. Geopolitical risks and lower oil prices impacted markets in the Middle East. Shares in Saudi Arabia saw some profit-taking following its inclusion in the MSCI Emerging Markets Index, as investors sought to lock in recent gains. Although the ruling African National Congress party in South Africa emerged victorious in the national elections, the global sell-off and depreciation in the rand dragged the stock market lower.

Important Legal Information

The comments, opinions and analyses expressed herein are solely the views of the author(s), are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FT affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

1. Source: National Bureau of Statistics of China. CLSA; US Census Bureau. Latest available data as of February 28, 2019.

2. Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results.

3. Ibid.

4. Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments