Trade tensions have dominated market news for the past month. A trade deal with China has not emerged, leading to a significant rise in tariff rates and an expanding set of industrial restrictions. A threatened U.S. tariff on imports from Mexico was avoided at the last minute, but the administration’s willingness to use trade restrictions as a weapon has not diminished.

Turning points in business cycles can only be identified in hindsight. Those who have lived through them recall feelings of uncertainty, heightened sensitivity to new information and an increasing emphasis on contingency planning. Those old feelings are coming back to us today. Our baseline still does not call for a recession, but downside risks are growing.

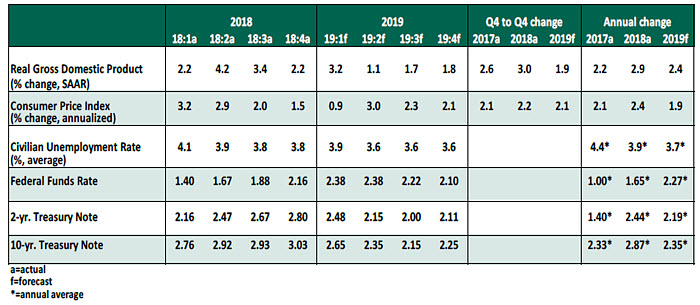

Key Economic Indicators

Influences on the Forecast

- Comments from Federal Reserve officials have hinted at willingness to intervene in markets if support is deemed necessary. Conditions are deteriorating, and we believe the Federal Open Market Committee will respond with two rate cuts in the second half of 2019. While markets are widely anticipating at least one cut this year, we caution against excessive jubilation; the Fed’s recent mantra of patience means a cut would only take place after conclusively poor economic data has started to arrive.

- Uncertain market conditions have weighed on the fixed income market, with yields on Treasury debt falling. The spread between 3-month and 10-year Treasuries has gone negative, more substantially and durably than the brief inversion in March. The risk-off sentiment prompted by trade uncertainty has caused global flows into all tenors of Treasuries, lowering yields across the curve.

- The May employment report disappointed, with only 75,000 jobs created. Employment growth was effectively zero, with last month’s gains negated by downward revisions to the prior two months’ payroll estimates. The unemployment rate held at 3.6%. The labor force participation rate has undone much of the gain witnessed in the second half of 2018. Encouragingly, initial jobless claims continue to hold at low levels, suggesting a labor market in stasis, with no substantial workforce reductions yet.

- First-quarter real gross domestic product (GDP) growth was affirmed at an annualized rate of 3.1%, an insignificant revision to the initial estimate. This outperformance was inflated by transitory increases in inventories and a fall in imports. A slower rate of growth in the balance of the year is virtually certain. At best, slower growth will be simply a return to a normal rate, not a recession.

- Higher-frequency data releases reveal slower economic activity. The Purchasing Managers’ Index (PMI) fell to 52.1 in May, its lowest reading since 2016, though still a level indicating expansion. Retail sales grew by only 3.1% year-over-year in April, holding below the consistent range of 4-6% growth observed in 2017 and 2018. Industrial production showed a similar slide to 0.9% annual growth in April.

- Inflation remains tepid, with personal consumption expenditure (PCE) price indices for May rising by only 1.5% year-over-year in both the headline and core (excluding food and energy) measures. The consumer price index (CPI) showed a firmer result for April, rising by 2.0% (core 2.1%). The unexpected decline in oil prices over the past month will be the latest factor holding headline rates in check in the months ahead. However, wage growth has persisted above 3% year-over-year for ten months, which may push inflation higher.

- The increase in the tariff rate from 10% to 25% on $200 billion of Chinese goods will take time to manifest. Goods shipped before the implementation on May 10 were granted an exemption. Any capacity to absorb the tariffs through margin tightening and supplier discounting was probably consumed with the 10% tariff; the escalation will lead to more noticeable volatility in prices.

- A threatened tariff of 5% on all imported goods from Mexico added to uncertainty across sectors, and its suspension has averted certain economic damage. Though this episode passed without incident, it did not encourage positive sentiment for continuing negotiations with other trade partners and ratification of the U.S.-Mexico-Canada Agreement.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation

northerntrust.com/disclosures

© Northern Trust

More Tax Planning Topics >