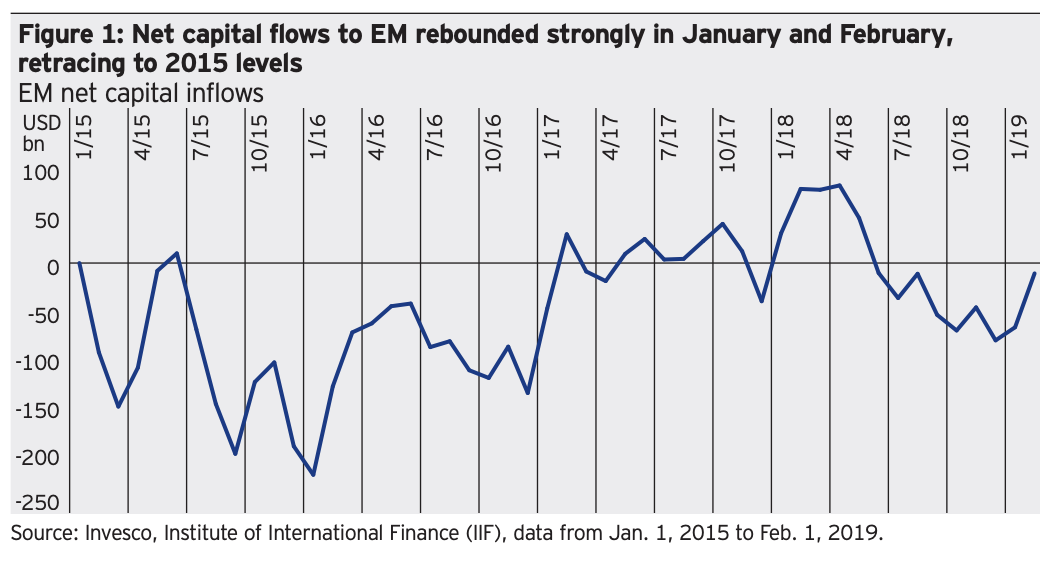

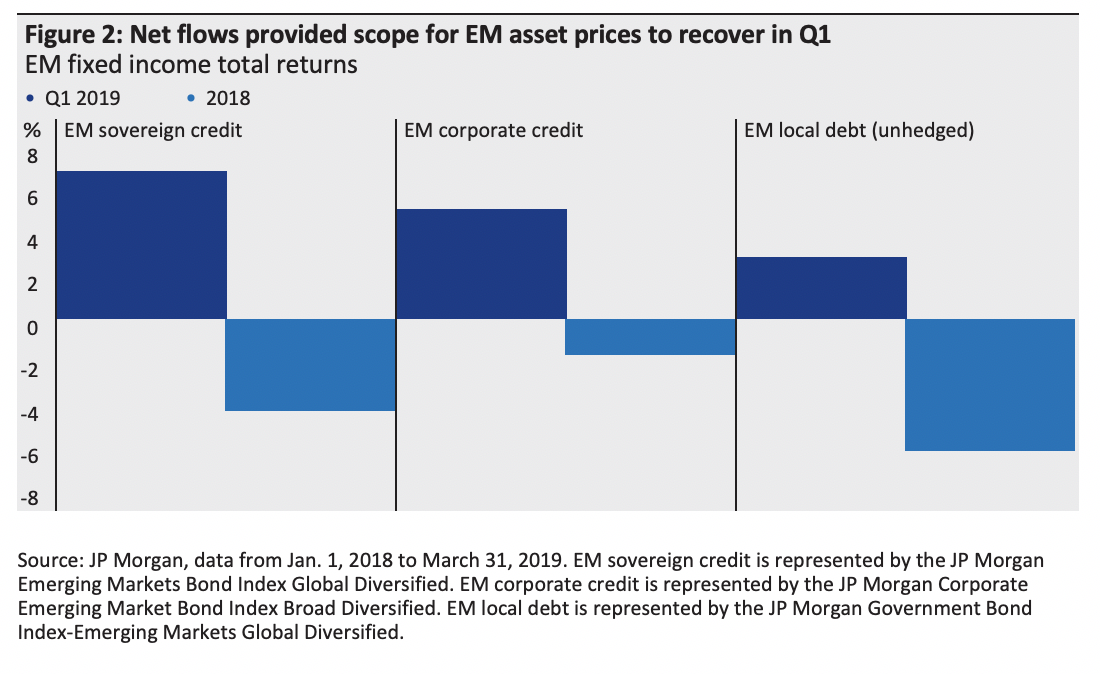

2019 started off strong for EM and broader risk markets, which recovered from the selloff in late 2018. We believe EM assets benefited from an improvement in external funding conditions, as data indicated a slowdown in US economic activity. This manifested in a weaker US dollar and lower core-market yields. However, concerns over global growth persisted over the quarter, leading to bouts of US dollar appreciation and weakness in EM currencies in February and early March. EM credit remained resilient, with credit spreads trading in a tight range over most of the quarter. We attribute this EM credit performance to strong demand for higher yielding fixed income assets, as core-market yields moved steadily lower. EM sovereign credit outperformed the EM fixed income complex with first quarter total returns of 7%, compared to 5.2% for EM corporate credit and 2.9% for EM local debt (in US dollar terms) over the period. (Figure 2)

Base-case scenario Q2 2019: Ascending, with turbulence

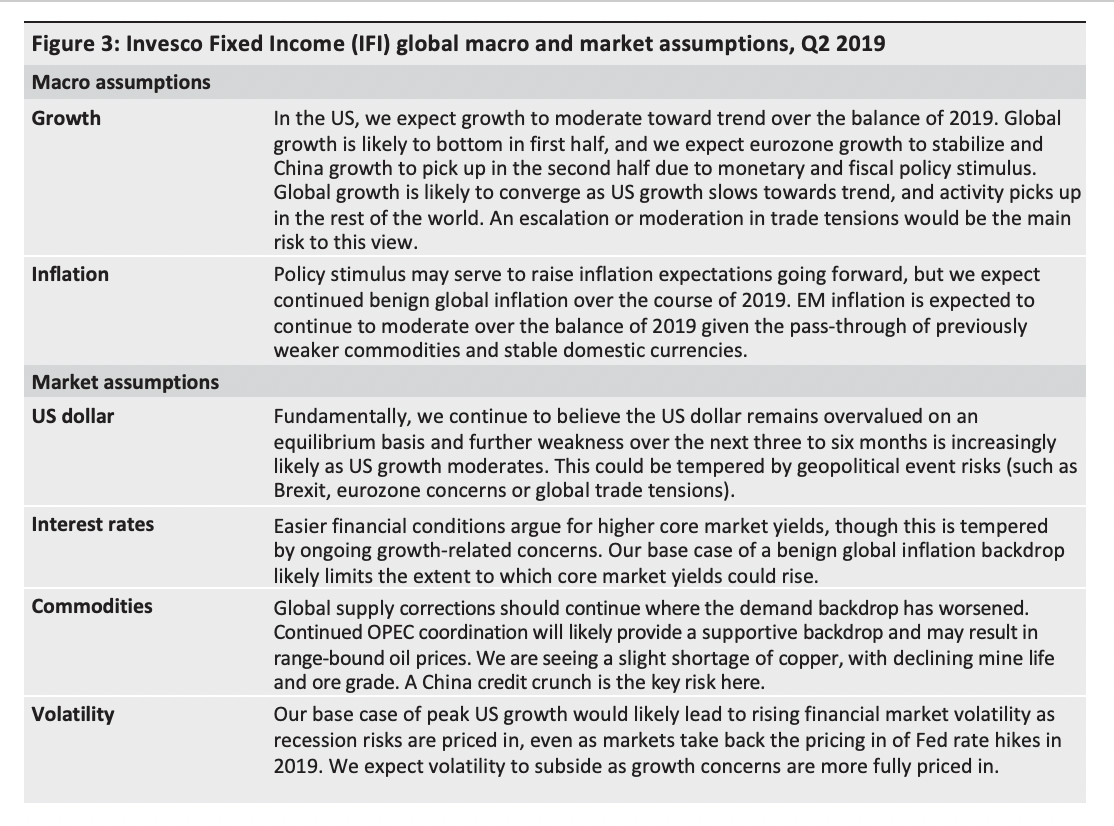

The improvement in financial conditions experienced since the first quarter provides scope, in our view, for further gains for EM assets in the second quarter. In addition to shifts toward policy accommodation by the European Central Bank (ECB), the People’s Bank of China (PBoC) and most notably the US Federal Reserve (Fed), we expect EM assets to be supported by steady global growth convergence, with US growth slowing and the rest of the world stabilizing. These outcomes would likely manifest in a weaker US dollar, which should strengthen EM currencies and lead to compression in EM credit risk spreads and local bond yields. In fact, this backdrop is expected to lend support to EM assets over the balance of the year.

However, we anticipate higher volatility in the second quarter. We expect global growth to slow over the first half of the year, albeit towards trend, and clearer signs of stabilization to show in the second half. This outcome likely limits scope for material improvement in underlying EM macro fundamentals and creditworthiness. In the near term, economic data may prove to be volatile, adding uncertainty to the global growth outlook.

As of this writing, trade negotiations between China and the US are ongoing and could be an additional source of uncertainty. Additionally, the currently heavy election period across EM may raise policy uncertainty in a number of key countries, even if the election results themselves do not throw up big surprises. Therefore, we believe EM valuations will be bounded to the upside over the quarter. Underlying fundamental improvement may remain elusive, making asset performance increasingly reliant on demand for higher-yielding assets, thus limiting the scope for an immediate decline of EM credit risk premia.

As we highlighted in our previous outlook, capital flows to EM depend on prospects for not only interest rates but also growth, in the US and the rest of the world. Therefore, declining US interest rates, due to the recently more-dovish Fed, are likely not sufficient to drive capital towards EM if coupled with slowing global growth. As such, a backdrop of improved US dollar funding conditions but lingering uncertainties over global economic growth provide context for bouts of EM volatility over the quarter. That said, we will seek to use periods of volatility to add exposure to EM due to our expectations for global growth stabilization and a weakening US dollar in the second half of the year. These events may provide context for fundamental improvement and a decline in underlying credit risk premia.

Risks to our view: pricing in of US recession

The most important risk to our view continues to be a material pricing in of recessionary risk in the US, which could support safe-haven assets, strengthening the US dollar and further weakening EM currencies. This would likely place additional funding pressure on EM issuers and lead to a downward repricing of EM assets. An escalation in trade tensions between the US and trading partners (China and Europe) could also lead to a material pricing in of global recessionary risks. Additionally, should China’s efforts at economic stabilization falter, concerns over the pace of global economic growth may rise.

IFI asset allocation: EM sovereign credit, currency preferred

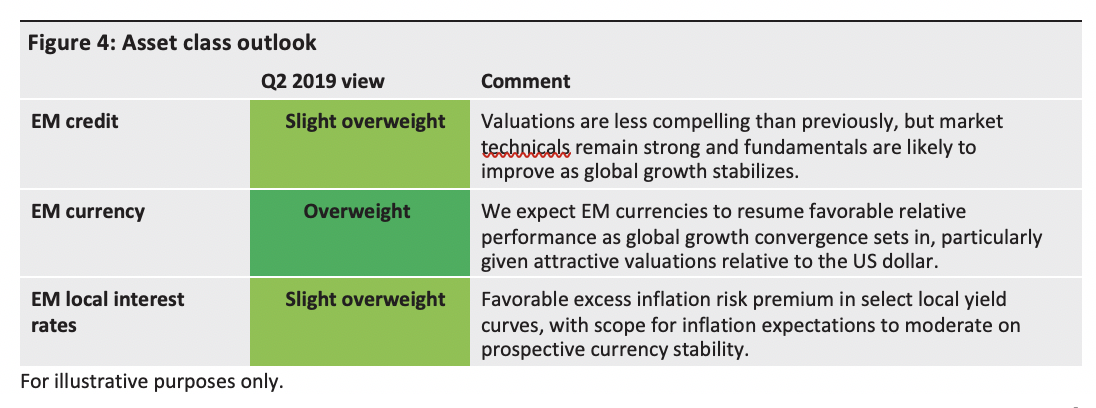

Our asset allocation favors EM sovereign credit and local currency bonds, unhedged, over EM corporate credit (Figure 4). Since the February selloff in EM local currencies, valuations are attractive, in our view, especially given the prospect of steady US dollar weakening into the second half of the year. Local duration performed well in the first quarter, and with an expected backdrop of still-moderating EM inflation, we believe further compression in inflation risk premia is likely.

In EM credit, we believe valuations are less compelling than last quarter, but market technicals continue to be supportive on favorable net supply and continued scope for crossover investors to reallocate to the asset class. Though broader credit market concerns may limit gains for EM credit over the course of 2019, we believe EM credit is a better value than US investment grade and US high yield on historical valuation grounds. The fundamental EM outlook of renewed growth impulse and earnings momentum is likely to improve in the second half of the year as funding conditions continue to ease. Therefore, we believe there is opportunity to capture value in EM credit as global growth moderation becomes fully priced in, allowing for steady spread compression and earning carry as 2019 progresses. We favor EM sovereign credit over corporate credit, largely on valuation grounds. We also prefer EM high yield over EM investment grade as we see better value in high yield and expect it to exhibit a more favorable response to improvements in global growth conditions as we head into the second half of the year.

We continue to believe that EM currencies stand to benefit from a pricing in of US growth moderation versus the rest of the world. As stated previously, this may weaken the US dollar and induce broader credit (and equity) volatility. In our view, EM currency valuations are not compelling on a broad, trade-weighted basis. This factor limits the case for benefits to net trade resulting from currency valuation, with the exception of Argentina and Turkey, a factor that boosted growth outcomes for many EM countries into 2016 after EM saw large currency adjustments between 2013 and 2015. That said, we believe there is value in select EM currencies on a narrower basis, relative to the US dollar. As stated in our previous outlook, the appreciation of many EM currencies versus the US dollar was considerable in January, arguing for allocating to EM currencies at better entry levels. EM currencies have since retreated versus the US dollar, providing compelling entry levels, in our view.

EM local interest rates have continued to compress along with core market yields, but we continue to see excess inflation risk premium in several EM local yield curves. Coupled with currency stability, this will likely lead to favorable gains for EM local assets in 2019, in contrast to the volatility experienced in 2018. Therefore, we believe EM local bonds, currency unhedged, may outperform EM credit over the course of 2019 as the US dollar retreats. We are cognizant of the downside risks to global growth. Even in the context of moderating US growth, this could lead to sharp bouts of volatility for EM, particularly in the local currency space. That said, reward versus risk has improved, and we will look for opportunities to continue to add exposure to EM local rates.

Country selection: politics take center-stage

We continue to expect ever-widening divergence in fundamental outcomes among countries, suggesting that idiosyncratic developments will likely be prominent drivers of overall EM performance in 2019.

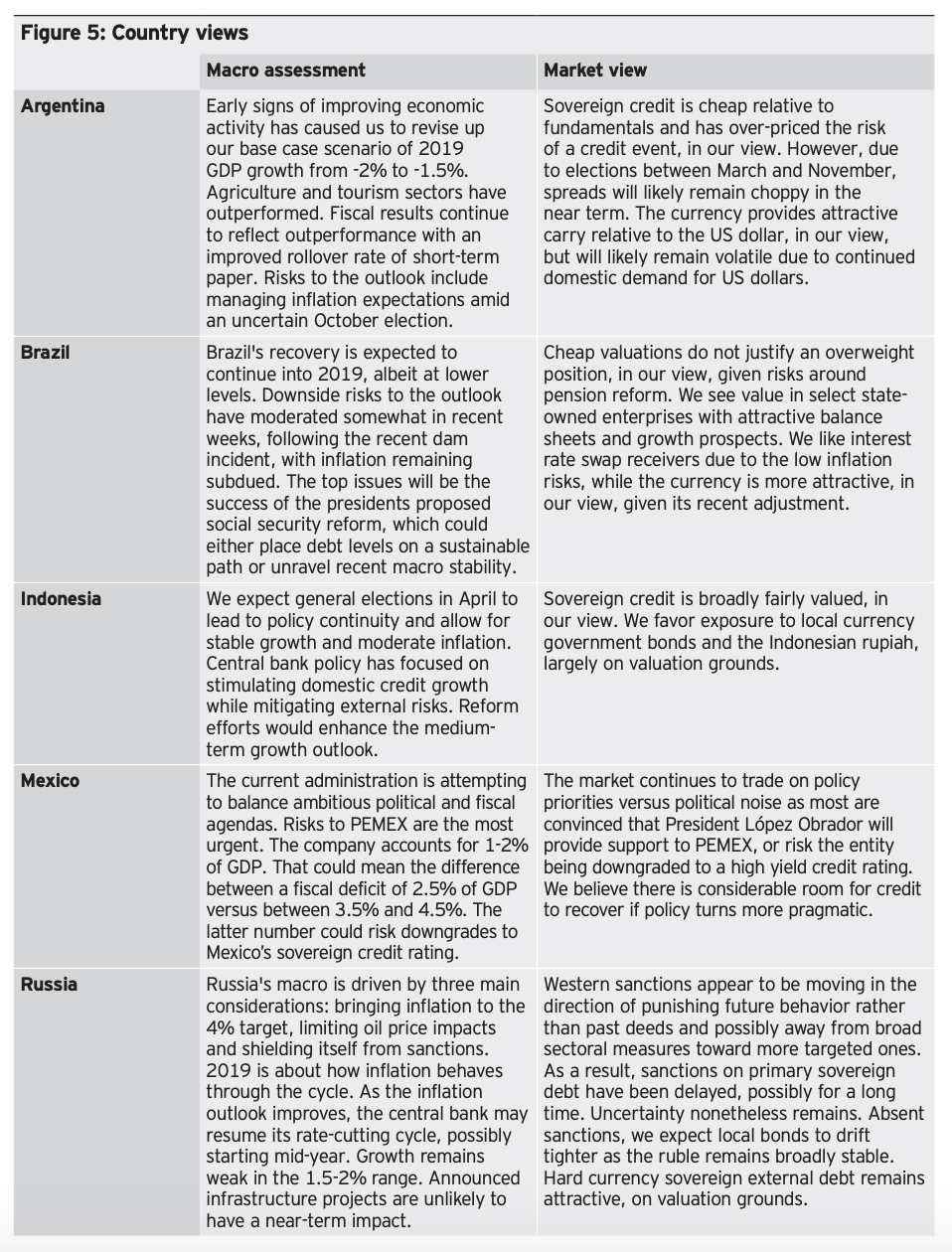

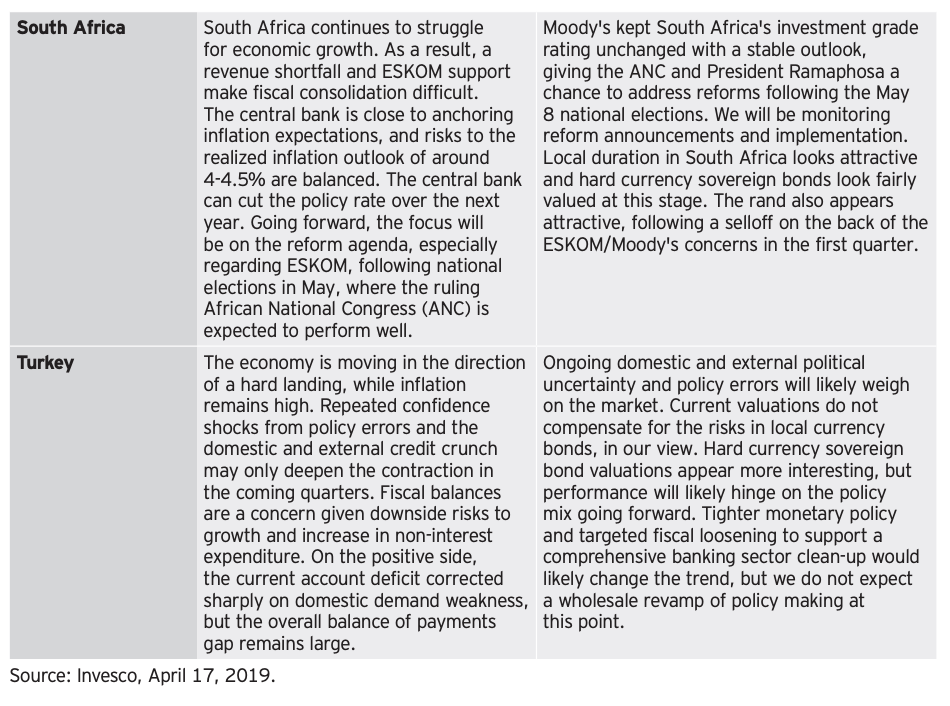

Politics in EM will likely be a focus for markets over the quarter. For starters, the quarter will continue to be marked by several elections, including those scheduled in India and South Africa. Already this year, there have been elections in Nigeria, Thailand, Turkey and, Ukraine and most recently, Indonesia. Indonesia's elections met our expectations, and similarly, we do not expect a surprise in South Africa. Incumbent parties will likely secure victory and, depending on the strength of mandate, spur the ruling parties to push for deepened structural reform.

Recent election results have been a mixed bag. In the Ukraine, a run-off on April 21 for the Presidential election pits two market-friendly candidates against one another, and in Turkey local elections seem to have decreased support for the ruling Justice and Development Party, at least at the municipal level, with opposition victories in Ankara and Istanbul. This result, if upheld, may complicate domestic policymaking, which is already an area of concern among market participants as the country navigates an economic slowdown.

We continue to believe fiscal outcomes will be critical in assessing creditworthiness for many sovereigns. The fate of long-awaited social security reforms will be closely watched in Brazil. Markets anticipate eventual passage. So far, signals from the new government are encouraging but need backing from the Congress. The extent of state support for government-owned entities in Mexico and South Africa – PEMEX (the state-owned oil company) and ESKOM (the state-owned power utility), respectively – are also being closely monitored and may influence sovereign creditworthiness in the months ahead.1

1 PEMEX stands for Petróleos Mexicanos (Mexican Petroleum). ESKOM is the Electricity Supply Commission.

Investment risks

The value of investments and any income will fluctuate (this may partly be the result of exchange rate fluctuations) and investors may not get back the full amount invested. Past performance is not a guide to future returns.

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating. The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

The risks of investing in securities of foreign issuers, including emerging market issuers, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

The performance of an investment concentrated in issuers of a certain region or country is expected to be closely tied to conditions within that region and to be more volatile than more geographically diversified investments.

Commodities may subject an investor to greater volatility than traditional securities such as stocks and bonds and can fluctuate significantly based on weather, political, tax, and other regulatory and market developments.

All material presented is compiled from sources believed to be reliable and current, but accuracy cannot be guaranteed. This is not to be construed as an offer to buy or sell any financial instruments and should not be relied upon as the sole factor in an investment making decision. As with all investments there are associated inherent risks. This should not be considered a recommendation to purchase any investment product. This does not constitute a recommendation of any investment strategy for a particular investor. Investors should consult a financial professional before making any investment decisions if they are uncertain whether an investment is suitable for them. Please obtain and review all financial material carefully before investing. The opinions expressed are those of the {author/speaker}, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

There is no guarantee that these views will come to pass.

These materials may contain statements that are not purely historical in nature but are “forward-looking statements.” These include, among other things, projections, forecasts, estimates of income, yield or return, future performance targets, sample or pro forma portfolio structures or portfolio composition, scenario analysis, specific investment strategies and proposed or pro forma levels of diversification or sector investment. These forward- looking statements can be identified by the use of forward looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” “target,” “believe,” the negatives thereof, other variations thereon or comparable terminology. Forward looking statements are based upon certain assumptions, some of which are described herein. Actual events are difficult to predict, are beyond the Invesco's control, and may substantially differ from those assumed. All forward-looking statements included herein are based on information available on the date hereof and Invesco assumes no duty to update any forward-looking statement.

Invesco Advisers, Inc. is an investment adviser; it provides investment advisory services to individual and institutional clients and does not sell securities. Invesco Distributors, Inc. is the US distributor for Invesco's retail products and private placements. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

Read more commentaries by Invesco