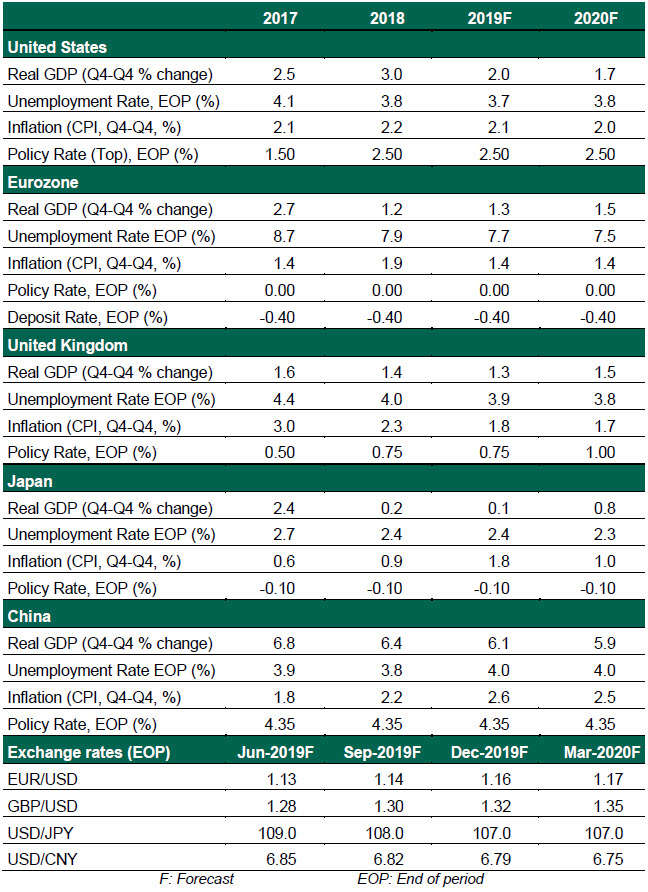

Growth Prospects and Challenges Ahead for the U.S., U.K., Eurozone, China, and Japan

SUMMARY

- Raising the Stakes

It is never easy to forecast economic trends, but the process is especially perilous at the moment. The sudden escalation of trade tensions that have originated from Washington is casting doubt over the outlook. If the escalation continues, the global economy will continue to decelerate and recession risks will rise.

Our base case anticipates that economic and political discomfort will limit the aggression and bring world leaders back into productive conference. In particular, we expect U.S.-China trade tensions to remain elevated through most of 2019 before the two sides find common ground. We do not anticipate further escalation of trade restrictions, but the month of May illustrated the potential for error around this assumption.

An alternative scenario would see a sharp slowdown in China and impaired activity in the United States, which would hit activity across the American, Asian and European continents. The risk of the U.K. crashing out of the European Union without a deal is rising again. Most recently, President Trump threatened tariffs on all imports from Mexico to curb migration from central America. With several threats on the horizon, the risks remain tilted to the downside.

United States

- U.S. economic indicators suggest the economy is slowing. First-quarter gross domestic product (GDP) growth of 3.1% was elevated by transient factors. In April, retail sales declined and business inventories were flat, manifesting in a slower trend. We believe this is a return to typical levels of growth and not yet the beginning of a downturn. The labor market remains strong, with low weekly jobless claims, providing assurance of continued economic momentum.

- Though U.S. trade tensions with China and Mexico have escalated recently, some progress is emerging on other fronts: the U.S. lifted its steel and aluminum tariffs against Mexico and Canada. Further, the U.S. deferred threatened tariffs on imported vehicles from Europe and Japan. On balance, the trade tensions are creating uncertainty, and the cost of new tariffs will add slightly to inflation in the near term.

Eurozone

- As in the first quarter, incoming data suggests domestic demand will continue to remain a key driver of the eurozone economy. The prospects for the export-reliant industrial sector remain bleak in the near term, reflected in weak survey readings. Potential U.S. auto tariffs on European imports and Italy's fiscal position are key risks for the region’s outlook.

- A fragmented European Parliament means policymaking is set to become more challenging in the region, with consequences for future trade policy, immigration and further EU reforms. A showdown between Italy and the European Commission over its rising debt is imminent. The union isn’t facing an existential threat, but consensus on important legislation will become hard to achieve.

United Kingdom

- The Brexit saga that led Prime Minister Theresa May to announce her exit will continue to keep policymaking in limbo. The success of Nigel Farage’s Brexit Party in the European elections will only push Tory leaders closer to supporting a “no deal” Brexit. Boris Johnson, the lead Tory candidate to be the next prime minister, has already stated that “we will leave the EU on 31 October, deal or no deal.” We are still hopeful for an agreement later this year that largely preserves the existing provisions of business and finance, but the odds of a hard Brexit are clearly on the rise again.

- Though the U.K. economy gained decent momentum in first quarter, the activity was supported by transitory factors including Brexit-related stockpiling ahead of the initial March deadline. The resilience of the British economy will be put to a serious test in the coming months as lingering uncertainty continues to take its toll on businesses and their investment decisions.