Executive Summary

♦ Emerging Markets Debt is a sizable and growing asset class offering much higher yields than traditional fixed income

♦ Given idiosyncrasies and exploitable inefficiencies, the asset class lends itself to active management

♦ Mondrian’s systematic and consistent approach to portfolio construction has yielded strong long- term results

♦ Current valuations, especially in local currency Emerging Markets Debt, are attractive.

1 – The Rise of Emerging Markets Debt

Over the past couple of decades, Emerging Markets Debt (EMD) has matured into a large, diverse and growing asset class. According to the Bank of International Settlements (BIS), there is currently more than US$20 trillion of emerging markets bond issuance outstanding – about a fifth of the total global fixed income universe. Within the most commonly followed indices, published by JPMorgan, there are more than seventy countries, with issuers including both sovereign and corporate entities. The strategic case for Emerging Markets Debt is in our opinion compelling. Firstly, it offers considerable potential for return enhancement and, secondly, it provides substantial diversification benefits.

Emerging market countries represent more than 80% of the world’s population, 75% of its land mass, more than 60% of its natural resources and more than 60% of its economic output; their debt markets cannot be ignored. Moreover, due to the idiosyncrasies of the countries involved and the inefficiencies of the asset class itself, our research suggests the Emerging Markets Debt asset class particularly lends itself to prudent active management.

In addition, we believe not only is the case for a long term strategic allocation to EMD compelling but the tactical case, given current valuations, suggests that the time is now ripe for entry.

2 – Anatomy of the Asset Class

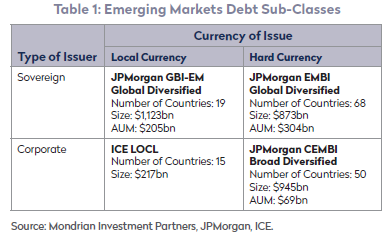

The EMD asset class as a whole can be divided into four distinct sub-classes depending on the type of issuer (sovereign or corporate) and the currency of issue (domestic or external). Table 1 below shows the industry leading benchmark for each of these sub-asset classes along with the number of countries covered by that index, the amount of debt represented in that index and, for three of the indices, the assets managed to that index. By far the largest, most actively traded and therefore most liquid, segment of the market is in the sovereign sector and it is this that we focus on in this paper. However, it should not be forgotten that corporate debt is a significant part of our EMD opportunity set.

2.1 Hard Currency EMD

Hard currency EMD refers to the issuance of debt by emerging market countries not in their own local currency but in a so-called “hard” currency that is generally more acceptable internationally as a store of value and means of payment. Principally, such debt is issued in the hardest of currencies, the US dollar. Due to the manner in which global emerging markets debt evolved, hard currency EMD has a longer track record than local currency EMD, since less developed countries were initially compelled to borrow mostly in US dollars, a phenomenon known as “original sin.” The US dollar denominated bond market grew out of the Brady Plan from 1989 (named after US treasury secretary Nicholas Brady) that enabled a number of countries to restructure their bank debt after it became distressed in the 1980s.

As noted above, the most widely-followed sovereign benchmark is the JPMorgan EMBI Global Diversified index¹, with returns going back to the beginning of 1994. Hard currency EMD is essentially a credit product offering a yield premium over US Treasuries, compensating for default risk and liquidity risk. As well as offering a yield pick-up over developed market yields, it offers diversification benefits, allowing a portion of fixed income exposure to be moved away from US rates without the worry of currency risk.

The risk-return profile of hard currency EMD compares favorably to high yield and investment grade corporate bonds. Historically, the yield pick up over US Treasuries has been around 350bps and defaults have been relatively rare, averaging around about one per year over the past 20 years. In addition, recovery values tend to be higher than in corporate defaults. Although the asset class will be affected by any rise in US rates, the generally higher yields offer a greater cushion for performance.

Today more than 50% of the EMBI Global Diversified bond index is investment grade, although there are a number of issuers at the very other end of the credit quality spectrum (that still suffer from “original sin”) that may still offer value when spreads compensate for that risk. Hard

Currency EMD offers exposure to a highly varied set of credits including many so-called frontier markets (over 60 countries versus 19 in the local currency benchmark).

2.2 Local Currency EMD

Local currency EMD benchmarks started in the mid-2000s as improved fundamentals and institutional development meant more countries could begin issuing substantially more debt in their own currencies. The drivers of return to local currency EMD primarily come via currency appreciation along with yield curve shifts driven by changes in inflation expectations and creditworthiness.

Given that countries can be at different stages on the economic cycle, interest rates and returns can be quite uncorrelated to those in developed markets. In addition, with deepening domestic markets, local currency bonds tend to be more liquid than hard currency ones as evidenced by

bid-offer spreads which remained relatively narrow even during the market stress of 2008 in comparison to those of hard currency USD-denominated EMD. Those emerging markets with a longer track record of issuing debt are increasingly supplanting external debt with local currency debt in order to reduce foreign exchange risk.

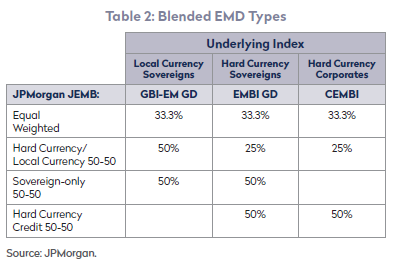

2.3 Blended Currency EMD

For those investors that wish to have exposure to a mixture of these EMD sub-classes, a blended EMD approach might be considered. Due to the increasing prevalence of such mandates, JPMorgan has just launched a suite of EM blended suite of indices (JEMB). These include four types of blend shown in Table 2 based on their three flagship indices shown earlier in Table 1 above.

Due to the more liquid nature of sovereign issuers, we suggest a sovereign only 50-50 blend with the tactical ability to invest in corporate credit when appropriate.

3 – The Strategic Cases for Investing in EMD

3.1 The Strategic Case 1: Return Enhancement

One of the key motives for an allocation to EMD is the prospect for long term return enhancement. There are three fundamental reasons why we believe EM debt should provide higher returns than traditional developed market fixed income assets:

• Higher yielding assets

• Improving fundamentals

• Potential for FX appreciation

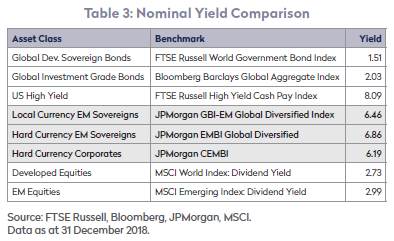

3.1.1 Higher Yielding Assets

EM countries as a whole provide higher yields both in nominal and real terms. Table 3 below shows that EM debt is amongst the highest yielding of all fixed income asset classes and offers yield considerably higher than those generally available in developed markets.

There are two sources to these generally higher yields. Firstly, in emerging economies the return on capital tends to be higher than that in advanced economies. Emerging markets can grow faster than developed ones since they have more scope for productivity enhancement through investment in both physical and human capital. This idea is called economic “catch up” and in order to attract the capital necessary to finance this growth, yields tend to be higher.

The real world, however, can be a bit more complicated. There are certainly examples of countries that have managed to catch up with more developed ones – for instance, Japan, South Korea and the Asian tigers, such as Hong Kong and Singapore. But equally there are many that have so far been left behind, including most of Sub-Saharan Africa and Latin America. Although economists endlessly debate the reasons for this divergence, one obvious one is that the structure of the economy must incentivize and reward productive behavior. Unambiguous property rights, the rule of law and good stable governance are all fundamental pre-requisites for economic development. The incredibly variegated nature of emerging markets is one reason why a blanket passive approach to investment is inappropriate: it pays to be cognizant of the fundamental idiosyncratic risks involved in each market.

This brings us to the second reason that yields tend to be higher and that is that there is often a risk premium built into the each market’s yield that compensates for the increased risk involved in EM investment. It is important to recognize this and adjust valuations according to their inherent risk. The good news is that the market often overcompensates for risk and defaults among EM sovereigns are actually quite rare and generally confined to the smaller frontier markets. In fact, among local currency issuers, not one country in the JPMorgan GBI-EM Global Diversified index has ever defaulted in the entire history of the benchmark. Indeed, in many cases fiscal policy is more prudently run in emerging markets than in developed ones. Over time, an improvement in credit risk can provide another source of excess return and we

consider this next.

3.1.2 Improving Fundamentals

As noted above, one of the reasons that EM bonds provide a higher yield is that they carry a risk premium. However, over time and as fundamentals improve there is no reason why this premium should not dissipate providing an additional driver of returns. Many emerging markets have already made impressive strides in terms of reform. Indeed those countries issuing local currency debt in the JPMorgan GBI- EM Global Diversified are on average investment grade. Moreover, there remains scope for much more reform and, while there are notable exceptions,

fundamentals have generally been improving across the EM world.

In local EM markets, investor bases are becoming broader, deeper and more stable. Local institutions, such as pension funds, are growing in importance with many countries moving from a pay as you go pension systems to a funded one. Increasing financial development also helps, as banks offer financial products such as savings vehicles and insurance. This helps liquidity in local markets and creates demand for governments to issue into. It also provides a source of demand in times of market stress. The growth of local bond markets is also important for the development of local pension plans, providing them with a natural home for duration and cash flow matched pension assets. There is therefore a virtuous circle involved in the twin development of pension funds and local bond markets.

Fiscal rules which impose long-lasting legal constraints on fiscal policy have also become more prevalent. These set limits on government expenditure, revenue, the overall deficit or debt levels. Of the eighteen countries in the JPMorgan GBI-EM Global Diversified index in 1995 only two countries (Indonesia and Malaysia) had fiscal rules in place. As of 2015, thirteen do as shown in Table 5 below.

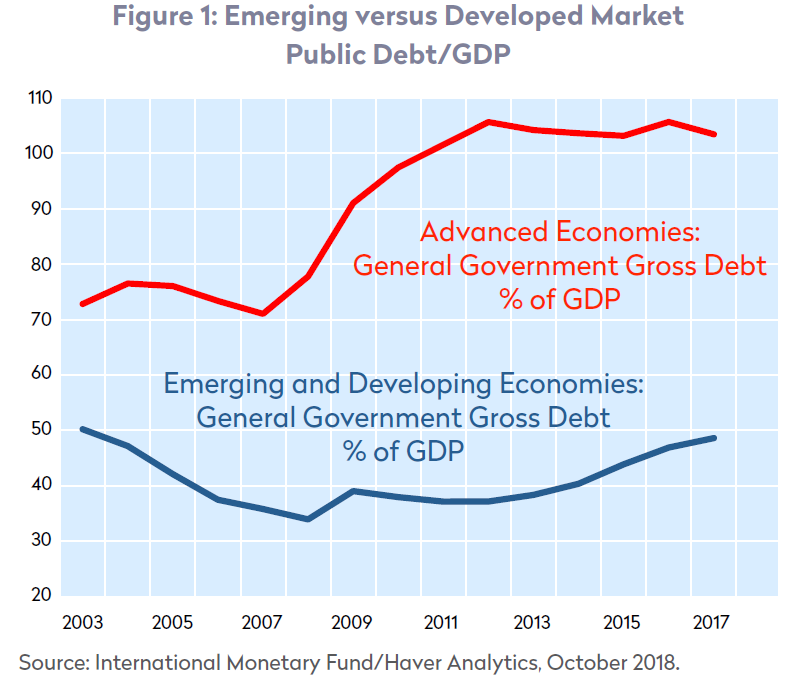

Of the countries in the JPMorgan hard currency index (EMBI Global Diversified) but not in the local currency one, none had fiscal rules in place in 1995 but twenty-one did by 2015, including Armenia, Costa Rica, Cote d’Ivoire, Mongolia and Senegal to pick a small sample. Also, against this backdrop, debt levels in general are much lower than in developed markets as shown in Figure 1.

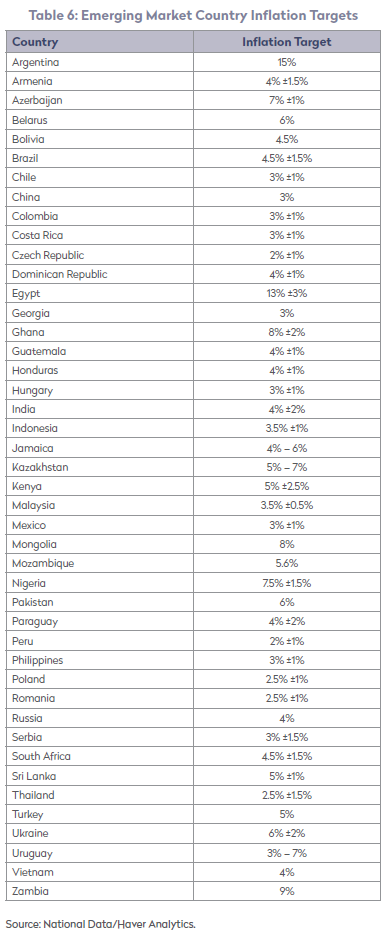

In addition, independent central banks, whether de facto or de jure, are now commonplace with formal inflation targets being followed reducing the scope for destabilizing monetary financing of government deficits. All countries in the JPMorgan GBI-EM Global Diversified index of local currency EMD issuers now have formal inflation targets, as do many in the EMBI index of hard currency issuers, as shown in Table 6 below.

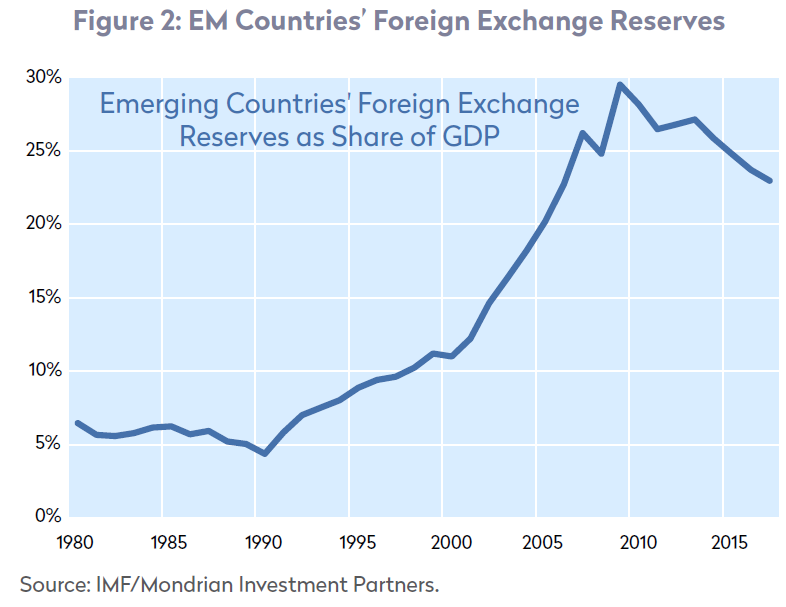

Not only this, but the external sector has also become stronger as more countries have adopted freely-floating or managed floating exchange rates rather than rigidly defended pegs that can become difficult to maintain, as witnessed in the Asian currency crisis of 1997. In general, as shown in Figure 2, countries also now maintain much larger FX reserves in order to protect against destabilizing capital flows.

Mondrian considers all of these fundamental drivers of relative creditworthiness along with the Environmental, Social and Governance (ESG) strengths and weaknesses of the countries we invest in.

3.1.3 Potential for FX Appreciation

As well as more attractive yields, emerging markets offer the prospect for real FX appreciation over the long term. This again stems from the potential for higher productivity growth in emerging markets. Anyone who has visited a less developed country will know that money tends to go further. For instance, a haircut that costs $20 in New York might cost just $5 in Jakarta. In other words the “real” exchange rate is low. However, over time productivity growth in the tradeable sector will cause wages to rise. Since labor is free to move between tradeable and non-tradeable sectors, this will also cause wages to rise in the non-tradeable sector (including the market for haircuts) too and the overall real exchange rate will rise. This can happen via a combination of inflation and nominal exchange rate appreciation and is known as the Balassa-Samuelson effect.

3.2 The Strategic Case 2: Diversification Benefits

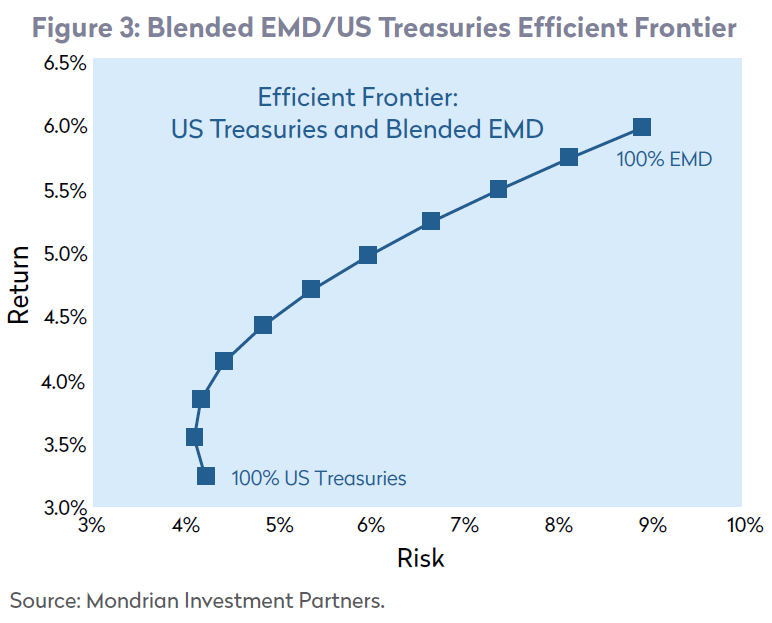

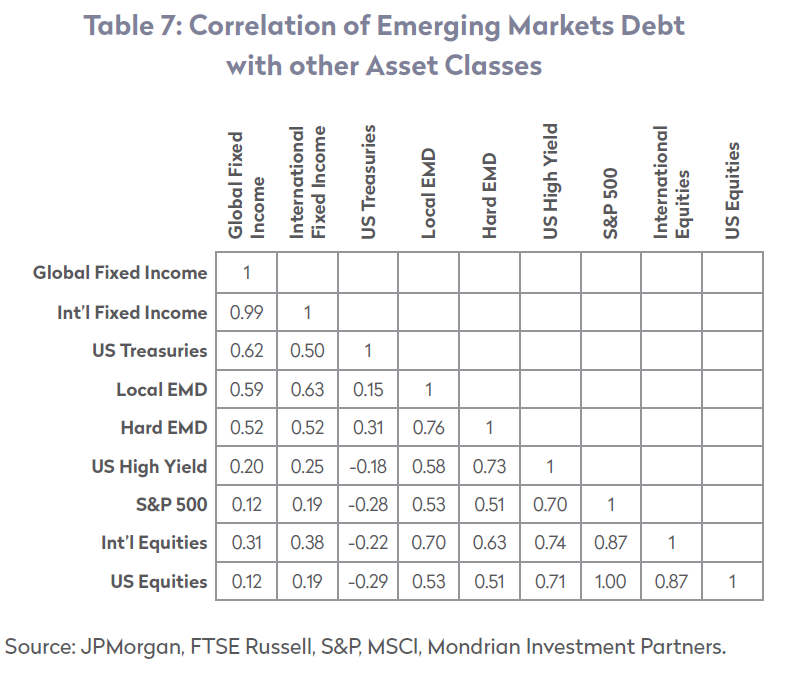

With the Emerging Markets Debt asset class encompassing a very wide range of countries (nineteen in the local currency benchmark and around seventy in the hard currency benchmark), it provides opportunities for diversification away from the main developed markets as well as offering those higher yields than many other asset classes. In Table 7 below, we can see that there is a weak correlation between emerging markets debt and other asset classes, demonstrating the ability of the asset class to be a good diversifier. Figure 3 demonstrates the point in terms of an efficient frontier based on a portfolio of blended currency EMD (50% local currency EMD/50% hard currency EMD) and US Treasuries.

It is often posited that, given an allocation to EM equities, there is no justification for an allocation to EM debt as the overall exposure to EM has already been gained through the equity allocation. We argue that this is incorrect, especially when one takes into account the geographical spread of the benchmark EM equity index.

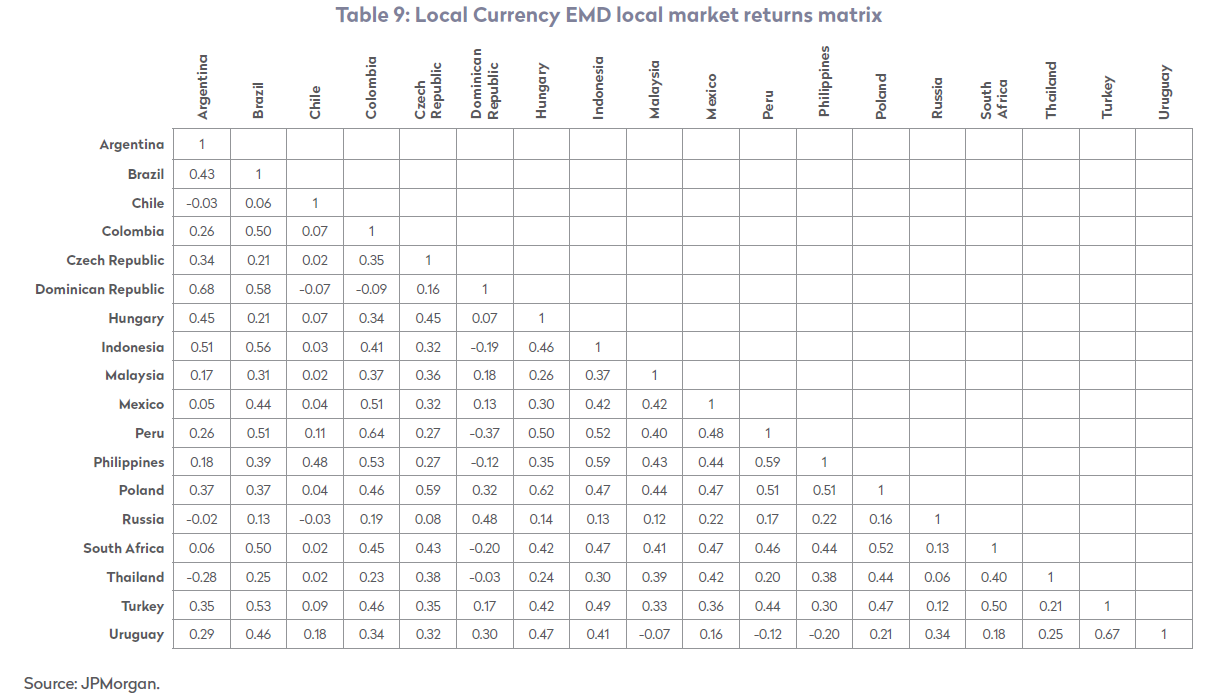

Tables 8 and 9 above show how investing across geographical regions aids diversification given weak correlations between them. However, with close to 75% of the EM equity index accounted for by Asia-Pacifi c countries

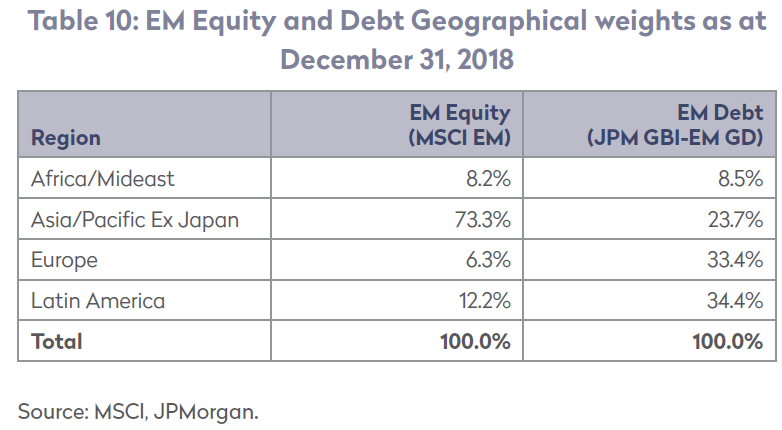

(with China comprising over 30% alone) little geographical diversification (and hence diversification of returns) is offered by the benchmark EM equity index. Table 10 shows the geographical spread of the EM equity index (MSCI EM Equity) against that of the (local currency) EM debt index (JPMorgan GBI-EM Global Diversified). It can be seen that the geographical spread of the EM debt index is much more even than that of the EM equity index, with the spread between Asia, Latin America and Europe being roughly equal. In light of the above tables, this suggests allocations to EM equity and debt should be seen as complementary to one another as you are effectively gaining exposure to different sets of countries and thus enhancing diversification by investing in both indexes.

4 – Active Management of EMD – The Mondrian Approach

We believe that EMD lends itself ideally to active management as the asset class has a number of inefficiencies that can cause valuations to become unmoored from their fundamentals. Currency trading and access to certain bond markets can be restricted for non- residents and there are often unwarranted bouts of risk aversion, contagion and exchange rate overshooting. These can all be exploited by an active approach to investing in emerging markets.

The Mondrian approach to country and currency allocation relies on the selection of markets that compensate for both inflation and credit risk. It has three principal components:

• Sovereign risk analysis

• Inflation forecasting

• Real exchange rate analysis

Our heritage is as a global investor and our approach has always been based on the combined analysis of each of these factors. Our dedicated Local Currency EMD product was spawned as an outgrowth of our Developed Market product which was already investing in EM markets. Following an extensive back test in the mid-2000s, the standalone product was launched. The approach has been proven to work in the fi eld with strong, consistent long-term outperformance: we have one of the longest and strongest track records in the industry.

In the 2010s we conducted a similar study of hard currency markets, performing an academically audited back test covering eighteen years and which provided equally promising results. This led to the launching of a hard

currency and blended currency product towards the end of 2016.

Although it is not the focus of this paper, corporate bond analysis plays a significant role in what we do and allocations between corporate and government issuance may vary over time.

5 – The Tactical Case for EMD

In addition to the strong long-term strategic case for EMD, the last twelve months have seen a substantial and, in many ways, unwarranted sell-off across emerging markets. Much of this has been due to fears of monetary tightening in the US and worries of political turbulence with a number of high-profi le elections causing particular concern. However, given the deceleration in global growth, continued Federal Reserve tightening is not a given and with general elections in the Czech Republic, Russia, Colombia, Turkey, Mexico, Brazil, Hungary and Malaysia now past, we believe a significant source of uncertainty regarding the direction of policy within these countries has been removed.

As a consequence, we are now at a point where in our opinion both currency and bond market valuations look attractive which could suggest an opportune entry point –particularly to the local currency EMD segment of the asset class.

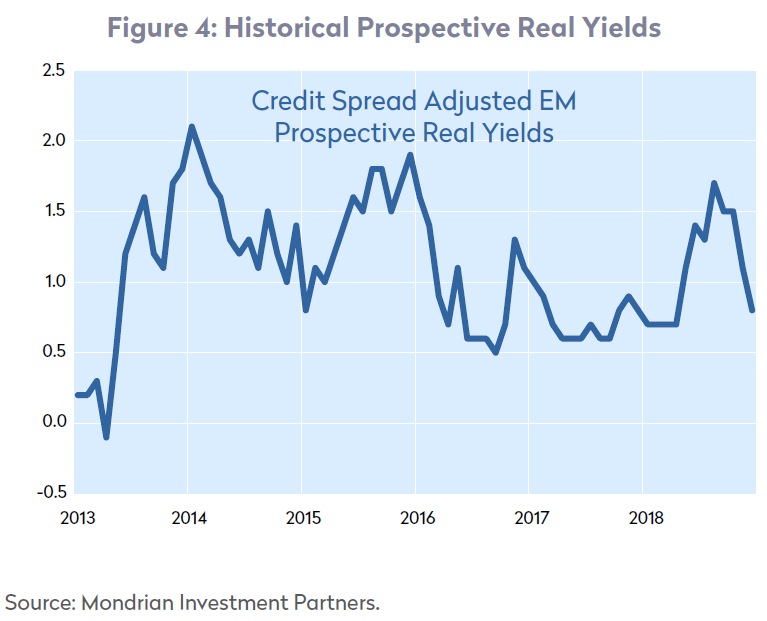

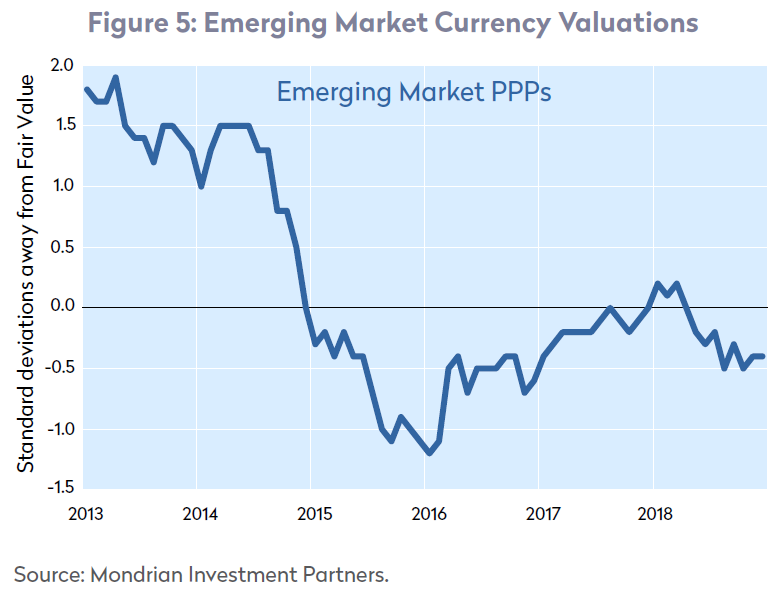

Prospective Real Yields (in other words, nominal yields adjusted for prospective inflation and credit risk) are close to post-financial crisis highs and EM currencies are now cheaper in real terms than during the financial crisis. Figure 4 and Figure 5 below show the overall Prospective Real Yield and Purchasing Power Parity (PPP) valuations respectively for the JPMorgan GBI-EM Global Diversified.

In conclusion, EMD offers considerable potential for both return enhancement and diversification. It is highly conducive to active management and valuations suggest a favorable entry point to the asset class now.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. Views should not be considered a recommendation to buy, hold or sell any security and should not be relied on as research or investment advice. The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. All information is subject to change without notice. This document may include forward-looking statements. All statements other than statements of historical facts are forward- looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those reflected in such forward-looking statements.

This document is an internal research paper. The material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors. Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate. There can be no assurance that the investment objectives of the strategy will be achieved.

This document is solely owned by and the intellectual property of Mondrian Investment Partners Limited. It may not be reproduced either in whole, or in part, without the written permission

of Mondrian Investment Partners Limited.

¹ This index includes not only bonds issued by sovereign governments but also those issued by so-called quasi-sovereigns which are 100% government owned or guaranteed entities.

© Mondrian Investment Partners

Read more commentaries by Mondrian Investment Partners