Infrastructure is a topic that has been in the news consistently over the past year. Importantly, everyone seems to agree that whatever infrastructure is, the country needs more of it. Given this rare moment of national consensus, I want to welcome you to the second installment of my blog series focusing on the different types of alternative investments. My last blog focused on real estate. Today, we will drill down into the infrastructure sector and a popular subsector, master limited partnerships (MLPs).

Overview of infrastructure

Merriam-Webster defines infrastructure as “the basic equipment and structures (such as roads and bridges) that are needed for a country, region, or organization to function properly.” This definition is a good starting point as it links infrastructure to meeting the needs of society. Roads, bridges, airports, tunnels, power lines, water distribution systems, shipping ports and railroads are examples of infrastructure assets.

On a global basis, there is a need for increased investment in infrastructure, both among emerging and developed economies. Emerging economies need infrastructure to support growth and increased urbanization. Developed countries need to make ongoing investments to maintain and upgrade existing infrastructure. For example, New York recently replaced the dilapidated Tappan Zee Bridge with the new Mario M. Cuomo Bridge, and is also in the middle of a multi-year redevelopment of LaGuardia Airport. If you’ve ever had the misfortune of driving over the old Tappan Zee or flying through LaGuardia (as I have), you know those projects were desperately needed!

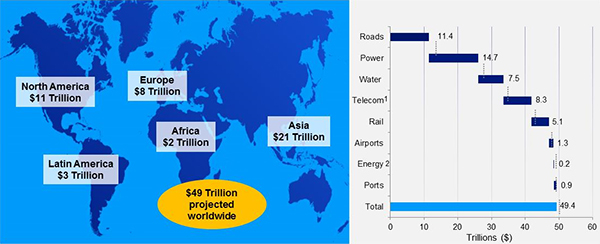

As shown below, there is a global need (currently estimated at $49 trillion1) for sizeable investments in infrastructure. The challenge is how to pay for investments of such magnitude when global gross domestic product (GDP) is approximately $86 trillion.2

Global infrastructure investment need estimated at $49 trillion

Map Source: Invesco Real Estate, IHS Global Insight, ITF, GWI, National Statistics, McKinsey Global Institute analysis. This is not financial advice or a recommendation to buy / hold / sell these securities. There is no guarantee that Invesco will hold these securities within its funds in the future. Chart Source: OECD; IHS Global Insight; GWI; IEA; McKinsey Global Institute analysis as of June 2018. $=US. OECD telecom estimate covers only OECD members plus Brazil, China and India. Energy estimate through 2023. There is no guarantee that these estimated needs will be funded.

While many governments acknowledge their strong need to make infrastructure investments, resources are often limited due in part to ongoing budget deficits. For this reason, government investment in infrastructure has been falling as a percentage of GDP, as illustrated below:

Despite need, global infrastructure investment has been declining as a percentage of GDP

Source: Invesco Real Estate using data from World Bank and McKinsey Global Institute Analysis as of 2015. Latest available data. Europe is represented by the European Union. Infrastructure investment is defined by gross fixed capital investment as a percent of GDP. Past performance is no guarantee of future results.

Public-private partnerships

Given the limited ability of governments to meet the need for infrastructure investment, private investors have rushed in to fill the void. For example, the LaGuardia Airport project is being built through a public-private partnership.

While the use of private funds for infrastructure is viewed as novel within the US, it is actually quite common elsewhere. Most airports outside the US are publicly listed and generate significant earnings from their retail business tenants (in addition to airline passenger fees). During my recent trip to Spain, I was struck by how much the airports resembled shopping malls.

Infrastructure investment options

Investors looking to gain exposure to infrastructure have several options:

- Listed infrastructure securities (such as the equity of firms that own and operate infrastructure)

- Mutual funds that invest in listed infrastructure securities

- Unlisted infrastructure investments (either through direct asset purchases or shares of privately placed funds)

Typically, only large investors such as institutions and high-net-worth individuals can access unlisted investments, whereas listed infrastructure securities can be purchased by anyone, either directly or through mutual funds.

Overview of master limited partnerships (MLPs)

MLPs represent a subset of infrastructure securities – these are publicly traded limited partnerships that are generally focused on energy infrastructure within the US. Pipelines, storage facilities and processing plants are all examples of assets that MLPs build, own and operate.

MLPs are typically classified into three categories:

- Upstream MLPs are involved in the exploration, recovery, development and production of crude oil and natural gas.

- Midstream MLPs are involved in the gathering, processing, storage and transportation of oil and gas.

- Downstream MLPs are involved in the distribution of fuels to end customers such as residential, industrial and agricultural entities.

MLPs are limited partnerships and, as such, do not pay federal income tax. Rather, MLPs pass income through to the limited partners who are then subject to income tax. Also, unlike many private limited partnerships with limited liquidity, MLPs are publicly traded and provide investors with the same liquidity as a publicly traded stock.

Production gains create corresponding need for more infrastructure

From 1980 through 2006, US production of crude oil and natural gas fell by approximately 20%.3 We believe this decline was primarily caused by the decreasing productivity of existing oil wells. Since 2006, the US has enjoyed strong growth in energy production and is projected to become a net exporter of energy in 2020.4

The growth in US energy production has been driven by new technologies such as hydraulic fracturing. This has allowed upstream producers to extract oil and gas from previously uneconomical locations.

As production has increased and new technologies have come online, the geography of US energy production has changed. For example, the Bakken formation in North Dakota and Montana and the Marcellus formation that spans New York, New Jersey, Pennsylvania, Ohio, West Virginia, Kentucky and Tennessee has turned those states into energy producers. One of the biggest challenges in those regions is how to transport and ship all the oil and gas. For natural gas, this challenge can be seen in the illustration below.

The challenge of getting natural gas to ports

Sources: Invesco Real Estate Research and Bloomberg as of December 2018. For illustrative purposes only.

The increasingly diverse geography of US energy production, combined with gains in overall production, has created a strong need for more energy infrastructure. The American Petroleum Institute estimates as much as $1.3 trillion in total direct investment of oil and gas transportation and storage infrastructure will be needed through 2035 to support US energy production levels.5 MLPs are expected to play an important role in providing the capital to build this infrastructure.

The evolution of MLPs

As the energy industry has evolved, so have MLPs. Today, most MLPs focus on midstream energy infrastructure with natural gas (rather than oil) as the primary focus.

MLPs often favor midstream infrastructure because demand has been growing for the plumbing that transports and stores oil and gas. Furthermore, revenue from midstream infrastructure is based on the volume of oil and gas processed and tends to be insulated from price fluctuations.

Gas MLPs have emerged as a popular investment for a number of reasons. The US is now the world’s top producer of natural gas with several competitive advantages over second-place Russia, including superior geology and more efficient infrastructure. Within the US, natural gas is quickly replacing coal in the generation of electricity. Globally, demand for natural gas (particularly in China and Japan) has been increasing. As a result, the US is on track to become a net exporter of natural gas in the near future.

Why investors should consider infrastructure and MLPs

We believe there are four primary reasons to consider making an infrastructure-related investment:

-

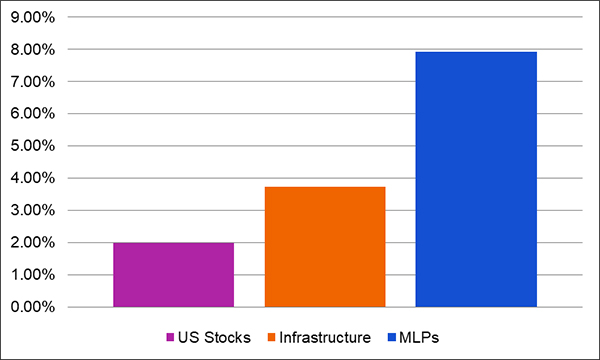

Attractive return potential. As illustrated below, infrastructure and MLPs have historically provided competitive returns relative to broad markets.

Historical returns of infrastructure and MLPs

Source: Bloomberg L.P., Infrastructure represented by Dow Jones Brookfield Global Infrastructure Total Return Index. MLPs represented by Alerian MLP Index. US Stocks represented by S&P 500 Index. Past performance is no guarantee of future results.

-

Potential to generate attractive yield. Both infrastructure and MLPs have the potential to offer attractive yield to investors. This is especially important given the current low yields offered in the equity and fixed income markets. As can be seen in the chart below, infrastructure and MLPs have been providing investors with a yield well above that of equities.

Current dividend yield on infrastructure and MLPs as of Feb. 28, 2019

Source: Bloomberg L.P., Infrastructure represented by Dow Jones Brookfield Global Infrastructure Total Return Index. MLPs represented by Alerian MLP Index. US Stocks represented by S&P 500 Index. Past performance is no guarantee of future results.

-

-

Inflation protection. An investment in infrastructure and MLPs may help investors hedge against inflation. During inflationary periods, infrastructure and MLPs may see an increase in both value and in current income generated (typically by raising prices and fees).

Historical correlation of infrastructure and MLPs to stocks and bonds

| |

US Stocks

|

US Bonds

|

Infrastructure

|

MLPs

|

| US Stocks |

1.00

|

|

|

|

| US Bonds |

-0.13

|

1.00

|

|

|

| Infrastructure |

0.72

|

0.27

|

1.00

|

|

| MLPs |

0.66

|

0.03

|

0.69

|

1.00

|

Source: Bloomberg L.P., Infrastructure represented by Dow Jones Brookfield Global Infrastructure Total Return Index. MLPs represented by Alerian MLP Index. US Stocks represented by S&P 500 Index. US Bonds represented by Bloomberg Barclays US Aggregate Bond Index. For the 10-year period ending Feb. 28, 2019.

Summary

It’s not every day that a consensus is reached on government spending priorities, but with regard to infrastructure, all US political parties seem to agree that the country needs more. As such, I cannot help but have a positive outlook for this sector. We hope this overview of MLPs and infrastructure, the second in our series featuring alternative investments, was timely and helpful. My next blog will focus on commodities.

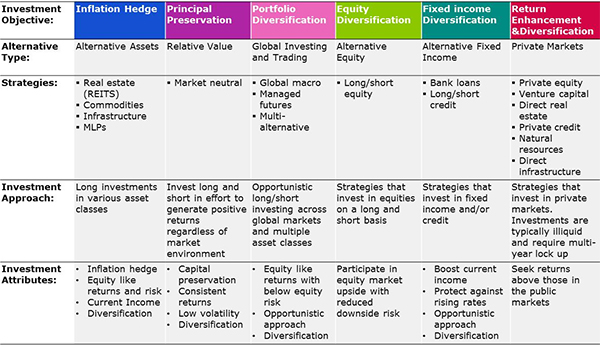

For a review of alternative investment types and related strategies, please see the Invesco framework below. To learn more about Invesco and its alternative capabilities please visit our website at www.invesco.com/alternatives.

A special thanks to David Wertheim for his assistance on this blog.

The Invesco alternative investments framework

1 Source: OECD; IHS Global Insight; GWI; IEA; McKinsey Global Institute analysis as of March 2017, latest data available.

2 Source: OECD; IHS Global Insight; GWI; IEA; McKinsey Global Institute analysis as of March 2017, latest data available.

3 Source: US Energy Information Administration report issued December 4, 2014

4 Source: CNBC, “US to become a net energy exporter in 2020 for time in 70 years, Energy Dept says”, Jan. 24, 2019.

5 Source: “API: Big investments needed in U.S. energy infrastructure”, UPI, June 22, 2018

Important information

Blog header image: JP Danko/Stocksy.com

Gross domestic product is a broad indicator of a region’s economic activity, measuring the monetary value of all the finished goods and services produced in that region over a specified period of time.

The Dow Jones Brookfield Global Infrastructure Total Return Index measures the stock performance of companies that exhibit strong infrastructure characteristics.

The Alerian MLP Index is a composite of the 50 most prominent energy master limited partnerships calculated by Standard & Poor’s using a float-adjusted market capitalization methodology.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The Bloomberg Barclays US Aggregate Bond Index is an unmanaged index considered representative of the US investment-grade, fixed-rate bond market.

Fixed income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Diversification does not guarantee a profit or eliminate the risk of loss.

A master limited partnership (MLP) is a publicly traded limited partnership in which the limited partner provides capital and receives periodic income distributions from the MLP’s cash flow and the general partner manages the MLP’s affairs and receives compensation linked to its performance.

Energy infrastructure MLPs are subject to a variety of industry specific risk factors that may adversely affect their business or operations, including those due to commodity production, volumes, commodity prices, weather conditions, terrorist attacks, etc. They are also subject to significant federal, state and local government regulation.

Alternative investments can be less liquid and more volatile than traditional investments such as stocks and bonds, and often lack longer-term track records.

Alternative products typically hold more non-traditional investments and employ more complex trading strategies, including hedging and leveraging through derivatives, short selling and opportunistic strategies that change with market conditions. Investors considering alternatives should be aware of their unique characteristics and additional risks from the strategies they use. Like all investments, performance will fluctuate. You can lose money.

Short selling is a speculative investment and may require investors to meet margin requirements and repurchase the security at a higher price, causing a loss. As there is no limit on how much the price of the security can increase, loss potential is unlimited.

Investment in infrastructure-related companies may be subject to high interest costs in connection with capital construction programs, costs associated with environmental and other regulations, the effects of economic slowdown and surplus capacity, the effects of energy conservation policies, governmental regulation and other factors.

Read more commentaries by Invesco

Source: Bloomberg L.P., Infrastructure represented by Dow Jones Brookfield Global Infrastructure Total Return Index. MLPs represented by Alerian MLP Index. US Stocks represented by S&P 500 Index. Past performance is no guarantee of future results.

Source: Bloomberg L.P., Infrastructure represented by Dow Jones Brookfield Global Infrastructure Total Return Index. MLPs represented by Alerian MLP Index. US Stocks represented by S&P 500 Index. Past performance is no guarantee of future results.