Weighing the Week Ahead: Stalemate?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar has plenty of important data. Fed speakers will be on the circuit. There is plenty of political and geopolitical news. On all of these fronts we see a stalemate.

(Learn more about stalemate tricks from Grandmaster and PhD mathematician Karsten Müller)

The financial punditry will ask:

What does political stalemate mean for financial markets?

Last Week Recap

- In last week’s installment of WTWA, I noted the light calendar and nearness to market highs, asking whether investors should fear a market top. That question was never raised, since the day I published, the first of the many Presidential tweets sent stock futures tumbling. I provided a brief update last Sunday night. I reviewed the latest Presidential tweets, the likely market effect and my reason for believing in an (eventual) deal. At mid-week I described some of the economic effects.

The President “marveled” at how one of his tweets seemed to move the stock market! (Business Insider).

Paul Schatz (Heritage Capital) writes:

After 30 years in the business, I keep saying that few things surprise me anymore, but I have to say that watching traders and market participants glued to Twitter for any sign of tariff walk back by the president is certainly a first for me. I can’t imagine what the great investors of yesteryear are thinking as they down on us from up above. Are the masses really hanging on every tweet from the leader of the free world? Apparently so.

Mike Williams (TruVestments) captures the action.

The tweets hit a vacuum of other news, and we can see the effect in our one-chart story.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Investing.com. If you visit their interactive chart you can check out each of the highlighted news events. There is also a chart for the futures, which is great for getting the sense of overnight trading.

Tweet and news-driven volatility resumed as part of a loss of 2.2%. The trading range was nearly 4% and Friday’s trading highlighted the possibility of deeper losses. As always, our indicator snapshot in the quant section below summarizes volatility and the VIX index in various time frames.

Personal Note

Thanks to the Intelligent Economist for including A Dash of Insight in the Top 100 Economics Blogs of 2019. This list has many great blogs, including a few I haven’t seen. Choices are made on quality, not school of thought, politics, or popularity. This makes the suggestions especially helpful.

Noteworthy

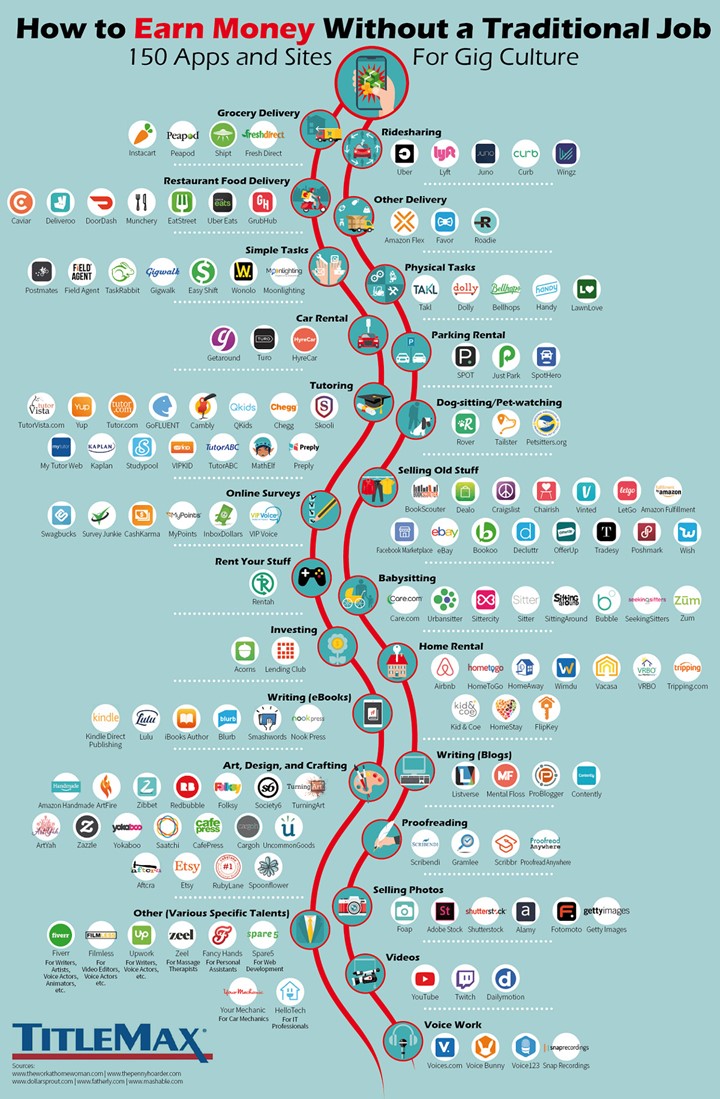

Part of the reason for low unemployment, based on whether people say they are working, and labor market slack is the gig economy. The Visual Capitalist shows the amazing list of apps that “power the gig economy.”

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

When relevant, I include expectations (E) and the prior reading (P).

New Deal Democrat’s high frequency indicators are an important part of our regular research. In his post this week he reports that indicators in all time frames remain positive. Since he attributes this partly to a “flight to quality” in bonds, NDD remains watchful.

The Good

-

Inflation remains tame.

- PPI increased 0.2%, in line with expectations and much better than March’s 0.6%. Core PPI increased only 0.1%, E 0.2% and P 0.3%.

- CPI increased 0.3% on the headline (beating expectations and the March results of 0.4%) and only 0.1% on the core.

- Earning reports continued a beat rate higher than in the last five years. (John Butters, FactSet). Brian Gilmartin reports improvement in expected earnings for the rest of 2019 and 2020.

- Hotel occupancy increased 1.2% on a year-over-year basis. The 2019 results are now only slightly behind 2018. (Calculated Risk).

- Mortgage applications increased 2.7% much better than the prior result, a decline of -4.3%. (Calculated Risk).

- Mortgage delinquencies in March were down to 3.65% and foreclosures at 0.51%. These rates are close to record lows. (Calculated Risk).

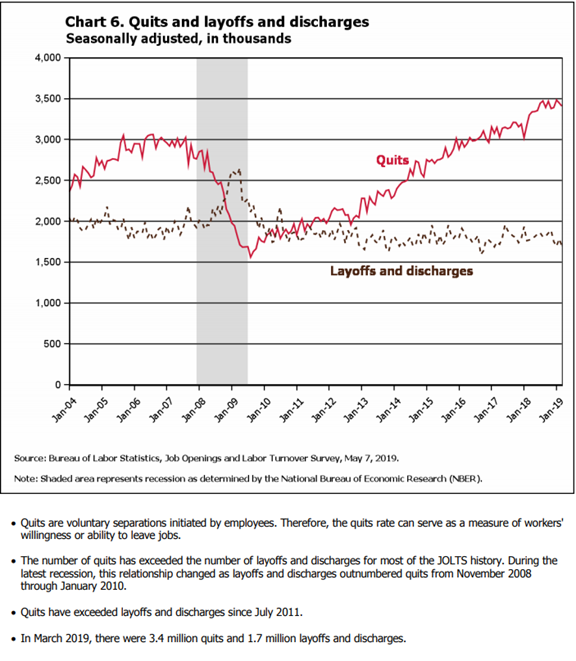

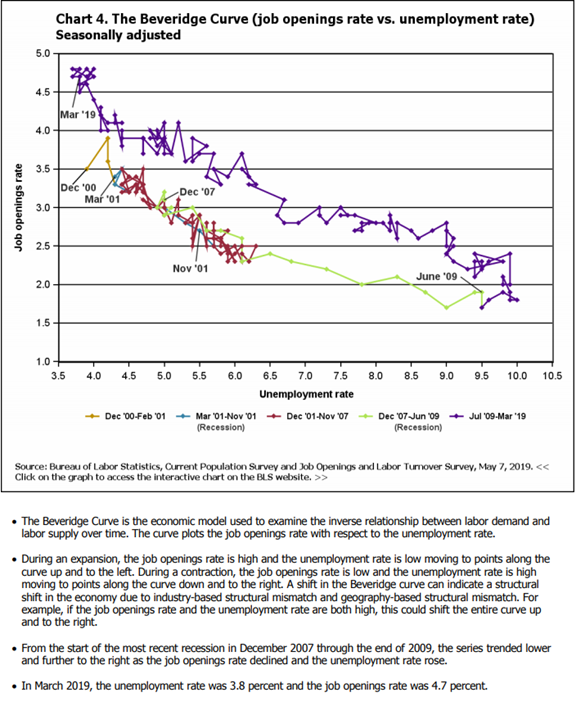

- The JOLTS report shows continuing labor market strength without excessive tightness. The official BLS site has plenty of data for analysis and a group of excellent charts.

The Bad

-

Initial jobless claims continued at a higher level, 228K. This is about the same as last week’s 230K, but worse than expectations of 220K.

-

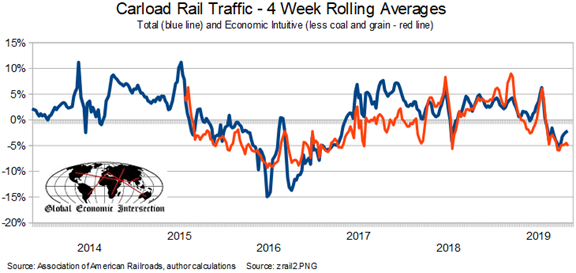

Rail traffic continues to decline. Steven Hansen (GEI) uses year-over-year rolling averages to smooth the series. He also tracks separately the “economically intuitive sectors,” down -5%. Here is one of the charts in this through analysis.

-

Swine fever is devastating China’s pork industry and seems to be spreading. (TIME).

-

The 10-year note auction was the poor. The yield rose from 2.448% on Tuesday to 2.479% in the auction. This created a “tail” of 0.013 percent. These are big moves in bond terms. The WSJ attributes part of the reason to the failing trade talks and a Trump tweet. For context, readers should look at our weekly indicator snapshot, including past interest rates.

-

US/Chinese trade deal was not completed before the most recent deadline, Friday morning. Rumors and tweets whipped markets around during the week. There is no solid evidence for the timing or nature of a deal. Meanwhile, the US increased tariffs on another $200 B of Chinese goods, and China vowed to retaliate.

The Ugly

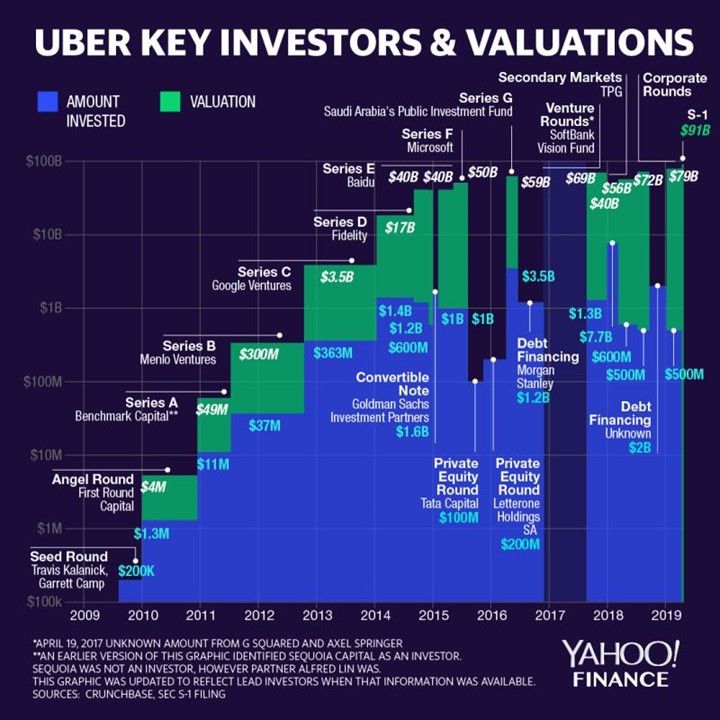

The Uber IPO. The pre-determined IPO price reflects the judgement of the company and its bankers about investor appetite. The early trades were expected by many to be in the 60’s, far above the offering price of $45. The stock closed at $41.57. It was the largest IPO in five years and the worst performing in history. (NYT, Gizmodo). The final valuation was barely higher than those used for the recent private investment rounds.

If you have been following Beth Kendig, one of our best sources and my colleague at FATRADER, you had advance warning on this one.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

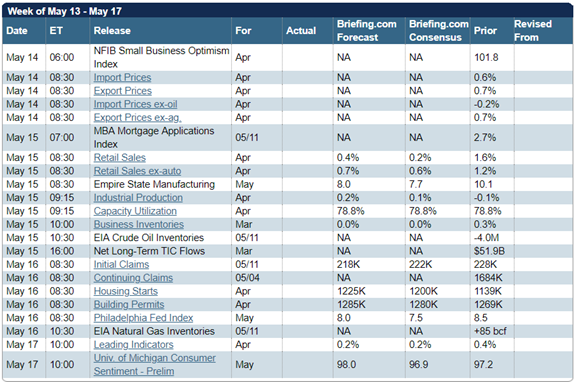

The calendar is a big one. Earnings season is winding down, but there is plenty of FedSpeak on the agenda. I am especially interested in retail sales and industrial production – two important elements in recession dating. Housing starts and building permits are important indicators in an important sector. Michigan sentiment remains important to determine consumer spending potential. Others emphasize leading indicators and the Philly Fed, but they are lower on my list.

And of course, we can wonder whether it matters in the world of tweetstorms and news “hints.”

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Despite the important economic calendar, I expect a different focus for the week ahead. Economic data has had little market effect since the December-January period. Even then the emphasis was on the Fed, not the economy. Since then we have traversed an earnings season with good results versus expectations with little market effect.

The market has focused on geopolitical issues, particularly trade. The big issues seem to be at a point of stalemate. That leaves us to ponder:

Does political and geopolitical stalemate imply the same for financial markets?

Background

The financial markets have returned to the “delicate balance” I wrote about last autumn. It is popular to personify organizational behavior and describe this as “complacency.” This lazy shortcut prevents us from seeing the wide range of investor attitudes. A lack of change in price and modest volume can simply represent a roughly equal balance of underlying supply and demand. There are plenty of skeptical investors.

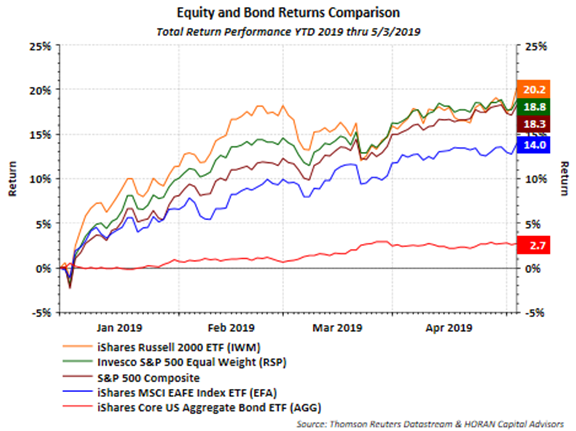

- David Templeton (HORAN) shows the large flows from equity funds and ETFs into bond and fixed income investments. This is true for 2019 despite the lower performance of fixed income.

- What happened to the “earnings recession?” Mike Williams cites Dr. Ed Yardeni’s note saying that it had been “averted.”

At the start of the Q1 earnings season, analysts had expected earnings growth to turn negative. But with nearly 83% of S&P 500 companies having reported revenues and earnings for the quarter, earnings continue to beat forecasts, and growth is trending net positive.

As they often have done in the past, industry analysts were too aggressive in cutting their numbers going into the latest earnings season. At the worst of it, analysts had S&P 500 earnings expectations down for Q1-2019 by as much as 2.5% y/y; that was during the 4/12 week. During the 5/2 week, the blended figure including reported results and estimates for yet-to-be-reported results was up 1.8%

He continues…

It’s already working (fear that is) as money leaves those ugly, very risky 15x to 16x earnings stocks, and floods into the 41x to 43x times earnings 10-year bond.

Note: This is the same spot where the experts have told you to be dreadfully afraid of higher interest rates and inflationary pressures as the demons of QE come home to roost.

Alas, no. Interests did not skyrocket after all.

By the way, that is why Mr. Gundlach, the current favourite child of financial media wants you to feel a bear is coming and the market is doomed.

He manages Bonds after all…and a lot of them.

And finally….

The Trade Deal

My own “prediction” before the first US/China meeting last autumn was a flexible deadline and an eventual agreement. It was not going to be easy. The reason is that the initial effects do not seem that harmful. The real-time lesson in economics takes time to play out. Even when we see the second-order effects it may be difficult to link them to trade policy. Blocking foreign trade, traditionally associated with Democrats and unions, has always played well to the public. It has a focus on jobs. The impact on reciprocal trade and consumers is much more difficult to see. This is why trade is the issue with the largest deviation between the conclusions of professional economists and those of the average person. This duality has played out even more badly than I expected.

The President claims that China is paying the taxes. The “get tough” policy plays well with his base. The Pundit-in-Chief, turning his expertise to political strategy, points out that the recent economic data provide shelter for policies that may introduce an economic drag. On this occasion he may be correct. Mainstream news shows focus on the GDP number and the unemployment rate. The Trump approval rating has moved higher, especially on his handling of the economy.

I do not expect China to capitulate soon, largely because they don’t need to.

The result is a stalemate, even though everyone is worse off. It may not be resolved until the 2020 election or shortly before. Some assert that Trump “needs” a trade deal, but why? (NYT) (Business Insider)

Impeachment, Subpoenas, and Investigations

Our daily news is full of new accusations and denials. “Witch hunt” and “case closed” represent one viewpoint. The other sees scores of violations that are certainly prosecutable violations and might be impeachable offenses.

What does it mean? Nothing. The Executive branch is resisting the House in an assertion of power. It may eventually be decided in the Supreme Court. Legislation related to investigations is easily blocked by the Senate or a Presidential veto. The Democratic leadership (although not all of the members) sees the futility of impeachment without a solid case and consensus support. Is there anything more we can expect to learn before the election?

Iran and North Korea

Presidential diplomacy has not advanced the case with North Korea and has escalated tensions with Iran. There are more issues with Palestine and Israel. These are disturbing situations for us as citizens – well worth learning about and expressing opinions to our friends. The implication for financial markets is murky. It is difficult to find immediate impacts, and the issues may continue in current form for many years.

A stalemate.

Implications for Markets?

Most sources continue the piecemeal approach to these stories, highlighting the negative features. As always, I recommend focusing on fundamentals – valuation, earnings, and economic risk. These all remain attractive for long-term investors who ignore the emotional Mr. Market.

The conclusions above are widespread in mainstream media. I have some conclusions of my own in today’s Final Thought.

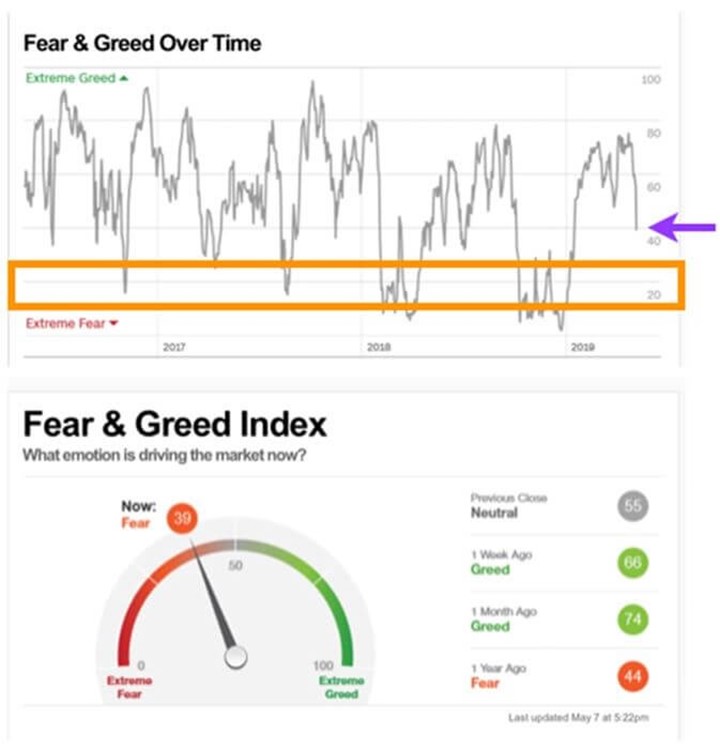

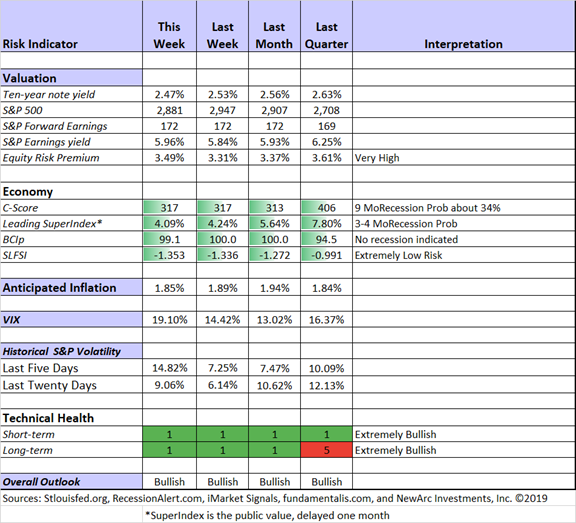

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Short-term and long-term technical conditions both continue at the most favorable level. Our fundamental indicators have remained bullish throughout the December decline and rebound. The C-Score has stabilized despite a flatter yield curve and increases in headline inflation. I continue to watch this closely, analyzing signs of possible confirmation of higher recession odds. Our methods give us an early warning, helping us to avoid costly “false positives.”

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession and he has pushed back the date for possible concern indicated by his employment model.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Guest Commentary

Professional forecasters in the Philadelphia Fed Survey see lower near-term growth (via GEI). 1.9% this quarter and 2.1% in Q3.

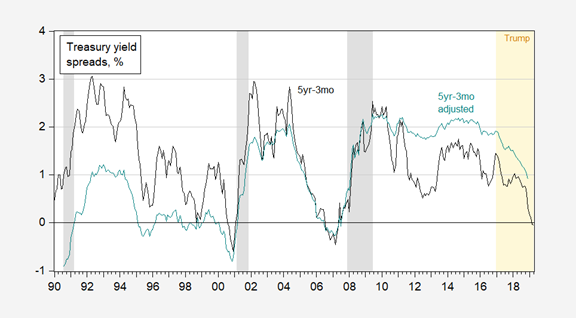

Menzie Chinn analyzes the 5-year/3 month spread. He looks at the current values, which imply a one-year probability of over 40%, higher than we are expecting. He also considers the curve distortions from Fed intervention. While the “reliably bearish” punditry claims this makes recession odds higher, Prof. Chinn correctly notes that the large scale asset purchases have pushed yields lower. He makes an adjustment, with citations for methods and background, and the result is dramatically different – about 6%.

Insight for Traders

Check out our weekly “Stock Exchange.” We combine links to important posts about trading, themes of current interest, and ideas from our trading models. Last week we discussed the news cycle effect on traders, asking whether they traded news cycles or market cycles. We cited some useful sources and discussed recent picks from our trading models. With all of the models back in action, there are more trading ideas and interesting contrasts with a fundamental approach. Felix rated the top twenty stocks in the Russell 1000 and Oscar did the same for the most liquid ETFs. Pulling this altogether was our regular editor, Blue Harbinger.

Insight for Investors

Investors should embrace volatility. They should join my delight in a well-documented list of worries. As the worries (shutdown, Fed policy, trade) are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be The Foundation of Every Proper Investment Plan by Christine Benz (Morningstar). She takes the amorphous goal setting and wealth-building concepts and translates them into a timeline with specific goals and priorities. The advice is clear and specific, but it defies summary. You should read the entire post.

I want to pair that wonderful advice with that of Trent Hamm (The Simple Dollar). In a logical fashion similar to that of Christine Benz, he clearly describes the steps in any financial decision – problem identification, research, and choice. Why is this important? It facilitates action, not dithering. Those who over-analyze seeking optimum solutions may wind up doing nothing.

If you took the steps outlined in these two articles, your investments would be much more likely to meet your goals.

Stock Ideas

Chuck Carnevale continues his sector-by-sector quest for attractively valued stocks. Each post in this series provides both interesting ideas and a lesson in how to perform solid analysis. He has reached utilities, which seems to be the end of the line. Not surprisingly he finds “slim pickings.” This is an extremely important post, describing the intertwined effects of valuation and dividends. Read his article carefully and you will understand this key conclusion:

Investing when overvaluation is manifest reduces your returns while investing when undervaluation is manifest can increase them. Therefore, when growth potential is low, there is little to no margin of error or safety. If you even slightly overpay for a slow growth stock such as a utility, you are very likely to earn unsatisfactory long-term returns. Moreover, you will earn these lower returns at elevated levels of risk. Higher risk and lower returns are the exact opposite of what prudent investors seek.

Bhavneesh Sharma has another interesting biotech idea, CRSPR Therapeutics (CRSP). Because of his experience in medicine, clinical work, and finance, he can spot ideas and explain them in a way you can understand. In this case, most investors know that CAR-T is a promising approach to fighting cancer through gene editing. Bhavneesh provides just enough technical detail. He reports clinical results and briefly touches on corporate financials. Even if you just want to learn more about the topic, this is a good read.

Barron’s highlights seven dividend stocks for “volatile times.” [Jeff – I’m not sure times will be very volatile and some of these names are expensive. That said, the list is worth a look].

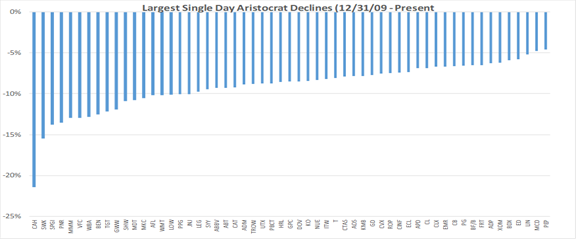

But beware. Ploutos provides A Brief History of Dividend Aristocrat Crashes.

Allen Good wonders Why Won’t the Market Shell Out for Shell?

He analyzes improvements in dealing with recent problems and compares Shell (RDS.A) to other integrated oil companies.

Want a cheap stock that is now attracting attention? Barron’s suggests Mosaic (MOS) may be at the bottom after an earnings cut this week. Why? Analyst upgrades after the 7% decline.

Or a sector that remains in the dumps? Barron’s discusses managed care companies.

Lyn Alden Schwartzer takes a close look at investing in Thailand via the iShares MSCI ETF (THD). She has a nice historical description as well as an analysis of investment fundamentals.

Index funds? Regular readers know that I am not a fan. Why buy the expensive along with the cheap? (See Chuck Carnevale above). Index funds overweight popular fad stocks. If you must invest in them, why not choose one that avoids this bias? Jack Hough (Barron’s) highlights reverse market cap.

Personal Finance

Abnormal Returns always provides interesting ideas on a wide variety of topics. I am a subscriber, and I read it daily. Each Wednesday’s editionincludes a post focused on personal finance. This week I especially appreciated Michael Batnick’s The Big Risk. Using some themes from Jeopardy champion James Holzhauer (a former resident of our town and a favorite of Mrs. OldProf) he examines the short-term risks of stocks compared to bonds. He writes:

Stocks are clearly a risky endeavor in the short-term, but over longer periods of time, when you think about why you’re investing, what feels safe carries a hidden risk.

See the full post for analysis, charts, and some tips from Holzhauer. Perhaps he should read another post Tadas cited on Wednesday, Adam M. Grossman’s After the Windfall.

Gil Weinreich’s series on Seeking Alpha (SA for FA’s) is ostensibly geared to financial advisors. The analysis is much broader than that. Most DIY investors will find it quite useful. This week I especially enjoyed the post, Your Money or Your Coffee. You will too. Gil takes a common current question about your investment returns from saving money on coffee. He cites some sources from each side of this debate – and there are two sides. He then notes the key principle: “The path to wealth and financial stability entails the active exchange of the transitory for the permanent.”

Spoiler Alert: He concludes that investors have room for “the occasional indulgence.” Whew!

Along the same lines, Ben Carlson discusses financial superpowers.

Watch out for…

Cornerstone OnDemand (CSOD). Gary Alexander has a nice post explaining why this possible value trap deserves its low price. It is a very good, very thorough job, serving as an illustration for investors. If you are not doing your own analysis, this is what to look for.

Troubled brokers. You should always use the FINRA site to check out a broker or advisor’s record. In fact, they are supposed to display the link on the site. This new regulation increases the obligations on “problem firms.”

Final Thought

First, a few random (but important) thoughts.

- The twitter effects seem to be wearing down. This is both my own observation and other comments I have seen. The longer these issues play out with the stalemate continuing, the less attention algorithms and traders will give.

- The typical causation blunder was seen in full force on Friday. Talking heads covering the Uber story debated whether the market was dragging down the IPO or vice-versa. No one even considered that they might be independent events! When the day closed with markets higher and Uber lower, writers stuck to their original stories, ignoring the evidence. This always happens when two events occur at the same time.

- No one knows what the Chinese leadership is thinking or what is motivating their actions. No one knows what the President is thinking or what motivates his actions. Despite this, many newly minted experts weave plausible stories based upon how you or I might think. This is totally irrelevant. It is just a way of filling otherwise dead air.

-

- A squeaky-clean White House and staff, consisting of people whose personal financial motives are secondary to the public interest;

- Complete financial transparency, as we typically see with government employees;

- Aggressive SEC monitoring of suspicious trades, one of their normal functions.

And finally, how to play the stalemate.

My own approach, and one that I strongly recommend to investors, is a focus on fundamental value with little attention to short-term movements. I elaborated on this in a webinar this week, joined by experts in different fields, all looking to the second half of 2019. Check out the free replay for my synthesis, charts, viewer questions, and the viewpoints of my colleagues.

If you are an investor, you should be focused on your personal goals and how to get there. Politics and geopolitics are sideshows on that journey.

And also, some longer-term items on my radar

I’m more worried about:

- US debt and the debt limit. The Bipartisan Policy Center has a good update and links to prior analysis. The debt limit “X Date” (at which point the federal government cannot meet all obligations in full and on time) is now projected for October or early November.

- International tensions. The US show of force in response to Iran and N. Korean missile tests lead the list. The investment implications of these events are unclear, but most find them unnerving.

I’m less worried about

- Chinese sales of US bonds. This seems to be the latest scare topic. China has to do something with the money from the trade surplus. There is a huge appetite for bonds from other investors. A big sale in the short term would be costly for the Chinese.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits