NewsLetter - May 2019

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits8 WAYS TO SPRING CLEAN YOUR FINANCES

An excellent piece by my friend Robert Powel in USA Today with a link to my partner Josh Mungavin’s free “Family Information Organizer”: https://www.amazon.com/Family-Information-Organizer-Emergency-Disaster-ebook/dp/B07HFG63CQ/

HOW LONG?

How long might you be around? A life expectancy calculator developed by the Janet and Mark L. Goldenson Center for Actuarial Research at the University of Connecticut.

https://apps.goldensoncenter.uconn.edu/HLEC/

NOT SUCH GOOD NEWS

“How much money will you need to retire? If you’re like the majority of Americans, you don’t know the answer.

A Bankrate survey from June 2018 found that 61 percent of Americans don’t know how much they will need to have saved to fund their retirement. Meanwhile, a separate March 2019 survey found that 21 percent of working Americans aren’t saving at all. It’s no surprise then that half of working households are “at risk” of not being able to maintain their standard of living when they retire, according to the National Retirement Risk Index (NRRI) from Boston College’s Center for Retirement Research.”

If you’re in the “don’t know” camp, check with us—that’s what we do.

https://www.bankrate.com/retirement/how-to-save-for-retirement/

NO COMMENT

Except you might want to consider the Fiduciary Oath.

“Wells Fargo, LPL, Raymond James, Stifel, Oppenheimer, RBC and 73 Other Firms Ordered to Pay Millions to Harmed Investors

The SEC has settled charges against 79 advisory firms that have been ordered to pay more than $125 million to mostly retail clients harmed in the sale of higher-priced mutual fund share classes when lower-priced share classes were available.”

SUCCOTASH

Barron’s recently published its 2018 “Fund Family Ranking: The Best Active Shops.” I must admit the concept and value of the “Best Shops” leaves me clueless. A fund family may rank highly due to a few of the managers posting outstanding performance while the majority are mediocre or worse. Kind of reminds me of the man who drowned in the lake that only had an “average” depth of four feet or the one who was comfortable with his head in the freezer and his rear in the oven. Investors put their money in individual funds, not families. Succotash may be fine for vegetables, but not investments.

HOW TO CALCULATE THE COST OF COLLEGE: A GUIDE TO FINANCIAL AID TERMS

An excellent guide from NPR for anyone facing the daunting task of funding college expenses.

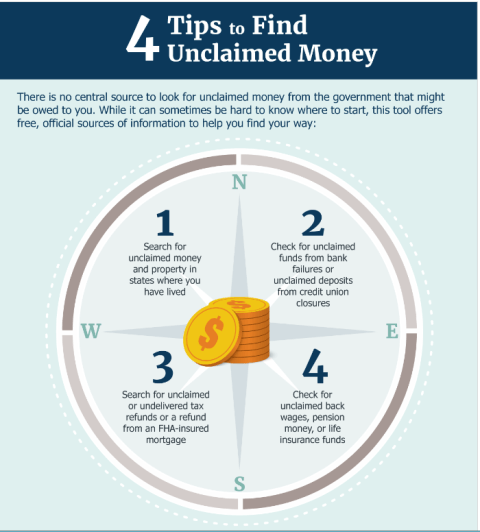

FREE MONEY (MAYBE)

A tip from AARP Magazine

https://www.usa.gov/unclaimed-money

BEWARE!

Of unrealistic guarantees and affinity marketing.

Getty Images Plus

“SEC Charges Texas Radio Host For $19.6 Million Ponzi Scheme”

William Gallagher, the self-dubbed “Money Doctor” and author of “Jesus Christ, Money Master” is principal of a firm that claimed “to be a vehicle of God’s peace and comfort to as many people as possible, helping first with their financial peace of mind.” Gallagher guaranteed investors risk-free returns in the accounts ranging from 5 percent to 8 percent per year, according to the SEC’s complaint.

The Securities and Exchange Commission charged a Texas radio host on Tuesday for allegedly operating a $19.6 million Ponzi scheme that targeted elderly Christian investors.

https://www.wealthmanagement.com/people/sec-charges-texas-radio-host-196-million-ponzi-scheme

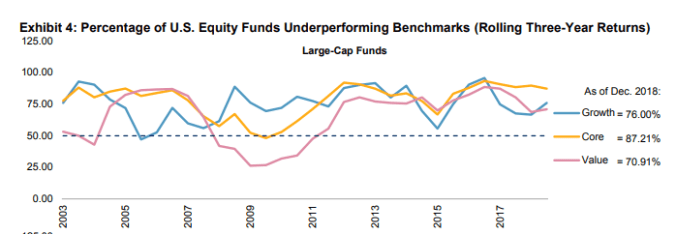

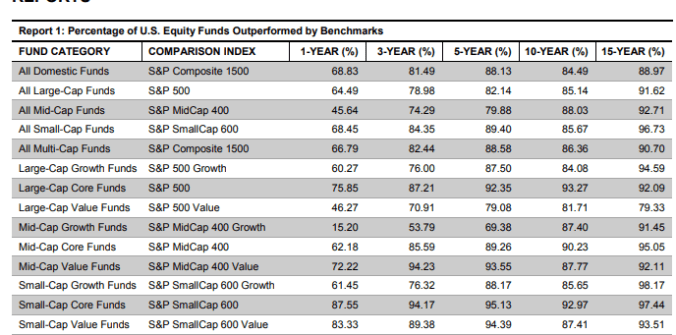

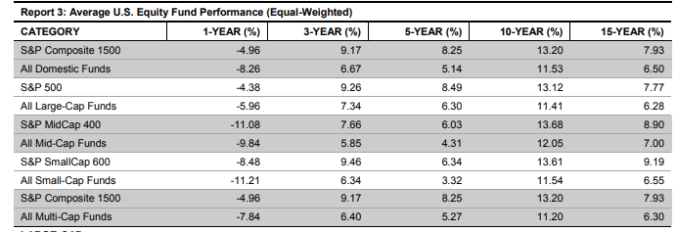

SPIVA UPDATE

The 2018 full year report is now in and it doesn’t look any better for active managers.

“For the ninth consecutive year, the majority (64.49%) of large-cap funds underperformed the S&P 500. The figures highlight that heightened market volatility does not necessarily result in better relative performance for active investing. Similarly, small-cap equity managers found it more challenging to navigate 2018’s market environment compared with 2017’s rangebound market movements; 68.45% of all small-cap funds lagged the S&P SmallCap 600 over the one-year horizon.”

https://us.spindices.com/documents/spiva/spiva-us-year-end-2018.pdf

AND MARKET TIMING DOES NOT HELP—IN FACT, IT COSTS

DALBAR: U.S. Investors Lost Twice As Much As The S&P 500 In 2018

A combination of volatile market conditions and bad timing caused the average U.S. investor to lose twice as much as the S&P 500 in 2018, according to a new study from DALBAR.

The research firm’s latest Quantitative Analysis of Investor Behavior (QAIB) found that investors were actually blown away by market turmoil last year, losing 9.42 percent over the course of 2018, compared with a 4.38 percent retreat by the S&P.

https://www.fa-mag.com/news/u-s–investors-lost-twice-as-much-as-the-s-p-500-in-2018-43995.html

GOOD ON YA

As my Aussie friends would say

From Financial Advisor

Grandparents Spending $179 Billion Annually On Grandkids: AARP

While grandparents spend an average of $2,572 annually, many are spending a good deal more on things like tuition assistance and even multi-gen vacations, according to new research from AARP, which found the financial impact that grandparents have on their grandchildren’s lives is immense.

https://www.fa-mag.com/news/grandparents-spending–179-billion-annually-on-grandkids–aarp-44245.html

I’M CONFUSED

“Maryland Lawmakers Get Earful On Proposed Broker Fiduciary Rule”

A recent story in Financial Advisor highlighted the debate over the fiduciary proposals now being debated in a number of states.

“Those both for and against Maryland legislation that would put brokers and insurance agents under a state fiduciary rule testified before state legislators on Wednesday…

Dually registered advisor and FSI member Bruce Robson, a partner with Comprehensive Financial Solutions (CFS) in Salisbury, Md., told Financial Advisor magazine that his smallest clients would likely be hurt by a state fiduciary rule that would force him to use only advisory accounts.

‘It would be harder to serve those clients because of cost,’ he said. ‘Our choices would be to stop working with smaller clients or to increase our fees to an unreasonable level, which would not just be a regulatory red flag, but put us out of compliance.’

Advisory accounts cost investors in the neighborhood of 0.75 percent to 1.0 percent of assets each year, while brokerage accounts can range from 3 percent to 5 percent in a one-time, upfront commission, which is amortized over the life of the account.”

- Why on earth would it be harder to serve small clients or cost them more? If the 3 to 5 percent is a reasonable upfront charge for the brokerage service and there is an issue with doing it as a commission, no problem: charge a 3 to 5 percent fee.

- I don’t understand the concept of “amortized over the life of the account.” After a commission sale there is NO “life of the account.” After the sale the obligation of the broker to the investor is over. If the broker never speaks to the client again they keep the 3 to 5 percent. In an advisory relationship, the advisor only continues to receive a fee if the client continues to receive advice they consider valuable.

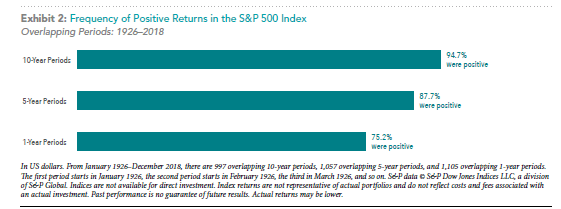

TIME IN THE MARKET, NOT TIMING THE MARKET

An interesting chart from DFA

DON’T KNOW WHY

They spent so much money trying to get their kids into a prestigious school. They should have focused on sports training.

HIGH-CLASS GARBAGE COLLECTOR

Our partner Katie is participating in a city program that invites community leaders to actively participate in various city services in order to gain an appreciation for the work of city workers. One of her first experiences was becoming a garbage collector. Her observation: It’s a lot harder than it looks! Coming soon, riding with the police for an evening. Mighty proud of her.

AND THE PRICE IS RIGHT!

NONSENSE

As much as I respect Fidelity, I can’t help but respond to this comment.

Baby boomers, heavily invested in stocks, are putting retirement savings at risk: study

“If there was a market downturn, they could lose a significant chunk of what they’ve worked so hard to save,” said Meghan Murphy, the vice president of thought leadership at Fidelity.

Roughly half of baby boomers have their 401(k) plans invested in riskier allocations than Fidelity suggests for their age group, Murphy said. (Fidelity recommends having around 54 percent in stocks and the rest in bonds, money market funds or certificates of deposit.)

First, assuming the portfolio is appropriately balanced and rebalanced and the investment is truly long term, they are unlikely to “lose a significant chunk of what they’ve worked so hard to save.”

Second, there is no reason to believe their 401K is their only form of saving.

Third, to advise an allocation based on age is wrong and often dangerous. Consider two families living next door to each other, both the same ages and health. One only has limited savings and their 401K, the other has significant savings, a high probability of a significant inheritance and/or the other spouse has a good pension and/or they spend significantly less than their neighbor, etc., etc. Obviously, age is a not very important factor.

Finally, it seems contradicted by what I believe is much more credible Fidelity advice

Long-term investors: Stick to your plan

If you are saving for retirement or another goal that is years away, the time to consider how much of a loss you can handle isn’t during a correction. Rather, you should consider the appropriate risk level for your portfolio when you are looking at your long-term goals, and thinking clearly about your financial situation and emotional reaction to risk.

If you haven’t created a plan, you should. If you have one, it may be worth checking in to see if your investments are still in line with that plan and if your plan continues to reflect your investment horizon, financial situation, and risk tolerance. If all that is so, you will likely be in a better position to manage the ups and downs of the market. If your mix of investments is off track, consider rebalancing back to a more neutral positioning

Key takeaways

- Given the inevitability of market pullbacks, it’s important to have an investment plan you can stick with through market ups and downs.

https://www.fidelity.com/viewpoints/investing-ideas/ready-for-stock-market-correction

NOT SO GOOD NEWS

Future of Retirement: Many Americans Will Run Out of Money; The Street.com

“The future of retirement is, in a word, bleak. Currently, only 58% of households between the ages of 35 and 64 are predicted to not run short of money in retirement, according to Jack VanDerhei, Research Director of the Employee Benefit Research Institute, and one of 16 experts who spoke at TheStreet’s Retirement, Taxes, and Income Strategies symposium held recently in New York. Or put another way: Roughly four in every 10 households between the ages of 35 and 64 (call it 27 million households) are predicted to run short of money in retirement, according to EBRI’s research.”

https://finance.yahoo.com/m/f0be4a7a-cad8-3e4a-a4ff-0ee98e933bb5/future-of-retirement%3A-many.html

MORE KATIE

Receiving her second consecutive Golden Apron Award from the mayor for raising the most funds at Beans and Cornbread, the fundraiser for Hospice of Lubbock.

PHILOSOPHERS OF THE TWENTIETH CENTURY

From my friend Alex

- When a man opens a car door for his wife, it’s either a new car or a new wife. ~ Prince Philip

- Having more money doesn’t make you happier. I have $50 million, but I’m just as happy as when I had $48 million. ~ Arnold Schwarzenegger

- If life were fair, Elvis would still be alive today and all the impersonators would be dead. ~ Johnny Carson

- The first piece of luggage on the carousel never belongs to anyone. ~ George Roberts

- As I hurtled through space, one thought kept crossing my mind—every part of this rocket was supplied by the lowest bidder. ~ John Glenn

- America is the only country where a significant proportion of the population believes that professional wrestling is real, but the moon landing was faked. ~ David Letterman

- I’m not a paranoid, deranged millionaire. Actually, I’m a billionaire. ~ Howard Hughes

- After a game of chess, the king and the pawn go into the same box. ~ Old Italian proverb

MENSA WINNERS

From David

The Washington Post’s Mensa Invitational once again invited readers to take any word from the dictionary, alter it by adding, subtracting, or changing one letter, and supply a new definition.

Here are a few of the winners…..

- Intaxication: Euphoria at getting a tax refund, which lasts until you realize it was your money to start with.

- Cashtration (n.): The act of buying a house, which renders the subject financially impotent for an indefinite period of time.

- Reintarnation: Coming back to life as a hillbilly.

- Giraffiti: Vandalism spray-painted very, very high.

- Sarchasm: The gulf between the author of sarcastic wit and the person who doesn’t get it.

- Inoculatte: To take coffee intravenously when you are running late.

- Karmageddon: It’s like, when everybody is sending off all these really bad vibes, right? And then, like, the Earth explodes and it’s like, a serious bummer.

- Decafalon (n): The grueling event of getting through the day consuming only things that are good for you.

- Dopeler Effect: The tendency of stupid ideas to seem smarter when they come at you rapidly.

- Arachnoleptic Fit (n.): The frantic dance performed just after you’ve accidentally walked through a spider web.

I THINK I SEE THE PROBLEM

As much as I loved growing up in New Orleans, it’s a bit depressing to see my home state ranked as the “Dumbest State for Financial Literacy: 2019.”

https://www.thinkadvisor.com/2019/04/09/10-dumbest-states-for-financial-literacy-2019/

BEST TIME TO BUY FLIGHTS

From Lifehacker

When to Buy Winter Flights

If you can avoid Christmas week and ski destinations, most winter destinations offer good value for the money.

- The average best time to buy is 94 days from travel (just over three months). The prime booking window is 74 to 116 days (about 2.5 months to nearly four months).

When to Buy Spring Flights

Plan ahead for spring flights. There are no major travel holidays in the spring, but both families and college students enjoy spring break for much of March and April. Take advantage of lower midweek prices to help keep costs down.

- The average best time to buy is 84 days from travel, or nearly three months. The prime booking window is 47 to 119 days (about 1.5 months to just under four months)

When to Buy Summer Flights

Americans travel a ton in the summer, and the peak summer dates of June 15 – August 15 are when the bulk of travel happens. You can find the best deals the closer you get to the end of the season (late August and September will give you the best odds to score low airfares).

- The average best time to buy is 99 days out from travel. The prime booking window is 21 to 150 days. Flying the second half of August on into September is the sweet spot for these deals.

When to Buy Fall Flights

Overall, fall offers great value for budget travelers. Fall is shoulder season for a lot of destinations, and people simply do not travel as much. Of course, the one exception to this rule is Thanksgiving week. Traveling during Thanksgiving? Better buy on the early side.

- The average best time to buy is 69 days from travel. The prime booking window is 20 to 109 days (about three weeks to 3.5 months)

https://lifehacker.com/the-best-time-to-buy-flights-in-2019-based-on-917-mill-1833514909

CHOOSING A FINANCIAL PROFESSIONAL

Some good advice from the Texas State Securities Board:

https://www.ssb.texas.gov/sites/default/files/2019_CORE4_Choosing_A_Financial_Professional.pdf

FINALLY

Keep your eye out for my “special report” on the December Rout, coming soon.

THE DECEMBER ROUT

In case you haven’t been paying attention, it’s been a bit rocky lately in the market, so I thought this might be a good time for a little recent history.

https://www.ft.com/content/73d3dd26-0ce0-11e9-acdc-4d9976f1533b

Hope you enjoyed this issue, and I look forward to “seeing you” again.

Harold Evensky

Chairman

Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits