Macro trends can run for a while, but they can also experience a quick end. Elections (Brexit, US Presidential Election) can cause the most powerful reversals in markets. Following the November 2016 election, US stocks went on a 15-month 60% rally. The Euro Bear Market started with Brexit in June 2016, which has been dragging on for the last three years. When US interest rates broke 2.5%-3.0% in January 2018, the S&P 500 entered into a wide trading range lasting about 15-Months. Here’s my guess how things play out going forward.

We may be at another one of those intersections. Trump rocked the market last Sunday with his Chinese Threats, and it took a few days before Wall Street got its bullish calls together. By mid-morning Thursday, the President said everything was fine, and stocks recovered. He got a letter from Chairman Xi. It says, your Flush no good. I have full house. They will make the deal. Mr. Market convinced the President that Recession was around the corner if he continued waging trade wars. That could be enough to re-assure markets, as it did Thursday. He must pull a rabbit out of his hat Friday. The Chinese are mad.

Currency and interest rate markets heard a different message, however, putting an end to the Powell put. Markets tricked him into a dovish stance last December. Last week, he said inflation in the US is going higher and rates ain’t going no lower. A cut was needed just to sustain the bond rally. Not happening. The $ has been shaky ever since the Q1 GDP report on April 26, and the Euro is showing signs of strength. If the Brits have a second vote and drop all plans for Brexit, the Euro could be headed higher.

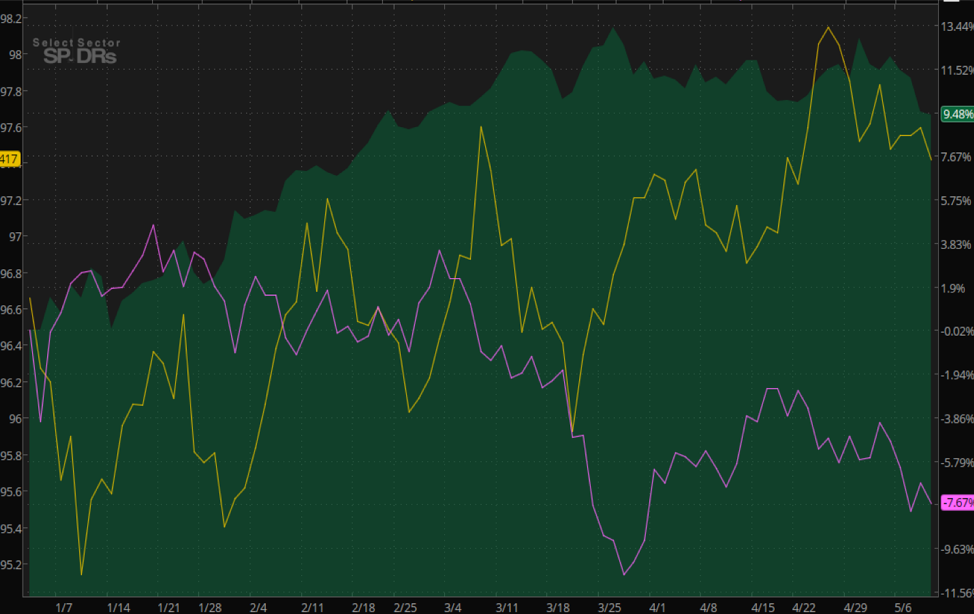

That’s bad news for the Utilities, surprisingly one of the best performing sectors in 2019. Few expected them to rally last year, because interest rates were so already low, and looked to be headed higher last Spring. But it still made sense to Euro and Asian Money Managers to park their excess reserves in $US and stock market via T-Bonds, ETF’s like TLT, and Utilities. As long as the $ was strong and US rates were rising. They might lose some, but it was a better than German Bunds or Japanese Debt, both of which guarantee a negative rate of return. So, Utilities it was until…

Wednesday. The XLU experienced a significant break down on Wednesday, slicing through support (Blue Line) at $57.50 on high volume. At yesterday’s close of $57, it is sitting at the exact level of their prior peak in December 2018. Utility stocks leveled off six weeks ago in late March, right about the time the market sniffed out better economic numbers from China (manufacturing & exports), a good spring in the US, and signs of life in Europe. With the on-again possibility of heavy tariffs announced Sunday, the US has too many risks to be risk-free for foreign investors. Europe is picking up market share.

A weaker $ could also bad for Transportation (IYT-ETF) stocks. If Utilities are a crowded arbitrage trade, bonds could sell-off simply because of the capital flows. It seems reasonable to think that US benefitted from negative yields in Germany and Japan, and they could get a lift from higher rates abroad. Is it possible that their economies may perk up if the US sets higher tariffs on China? The world is getting impatient with the US on a variety of issues, and might prefer do business with Europe and Japan right now.

In the near term, higher rates could hurt the housing market, which has not hit its stride in this upcycle. The stocks have benefitted from the expectation of lower rates, and the boost it would provide to mortgage activity. Higher rates would certainly put a dent in this demand. Toll Brothers (TOL-$38) reports on May 22. I expect investors will be disappointed with the results. Short the stock, and LEN. (LEN-$52).

In light of the near-term uncertainty for the US economy, like Energy right here. The Sector has pulled into a support area, and oil prices could get a lift from a weaker dollar, supply problems from Iran and Venezuela, and less production from Saudi Arabia. In addition, the US just sent an aircraft carrier to the Middle East. The world is nervous. EOG ($94) is my favorite Permian play. Maybe Chevron will target a different company. Oil service is as washed out a group as there is. Any funny business out of Iran, and the Energy sector could have a run. I like SLB ($40) and National Oil Well Varco ($40). Both sold off big on their recent quarterly results, which were lousy. Any whiff of tightening supplies, and they could see a short covering rally. And now I’m off for the Driving Range.

© Saut Strategy

More ETF Topics >