Growth Prospects and Challenges Ahead for the U.S., U.K., Eurozone, China, and Japan

The economic slowdown that began in late 2018 has started to stabilize. Trade tensions and policy uncertainty took a toll on confidence and financial markets late last year, but both seem less threatening today. Financial conditions have eased as major central banks (including the U.S. Federal Reserve) maintain a fairly accommodative stance amid a subdued inflation outlook.

A U.S.-China trade agreement is likely in the coming months, but wider tensions remain in other U.S. trade relationships. Amid other threats, the U.S. has moved toward imposing $11 billion in tariffs on Europe, putting the global automotive market at risk. And the roads to United States-Mexico-Canada Agreement and Brexit ratification won’t be easy.

We continue to see risks to our outlook as weighted to the downside.

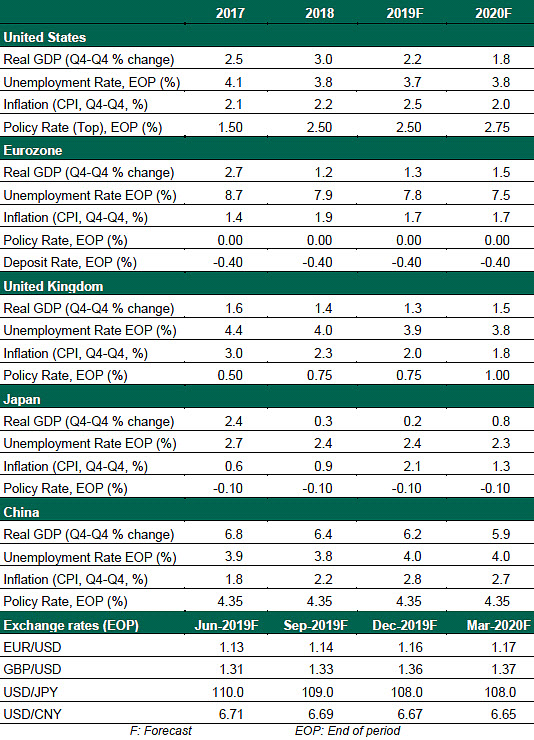

United States

- The U.S. economy has delayed this year’s expected slowdown, with real first-quarter gross domestic product (GDP) estimated to have grown by 3.2% on an annualized basis. However, much of the strength was explained by transient increases to inventories and net trade. We expect the momentum to fade in the coming quarters but not to an extent that warrants a rate cut by the Fed. As long as economic performance persists, we expect one hike in 2020.

- The labor market remains strong, as reflected in the March employment report. Weekly jobless claims touched 50-year record lows, providing assurance of continued economic momentum.

Eurozone

- According to the flash estimate, the eurozone’s quarter-over-quarter real GDP growth improved in the first quarter, driven by strong domestic demand. But external headwinds continue to weigh on industrial performance. Increasing evidence of a stabilizing Chinese economy and global manufacturing should bode well for Europe’s exporters in the second half of the year. That said, risks remain tilted to the downside as Brexit and U.S. car tariff threats loom large.

- Higher oil prices should boost the headline inflation but won’t be enough for the European Central Bank to move interest rates higher. A subdued economic outlook (including core inflation) suggests rate increases are a long way off.

- May elections for the European Parliament will remain in focus as they might challenge confidence and create policy uncertainty for the years ahead.