Projections of Fed rate changes appear misaligned with inflation expectations and GDP growth.

From its 2018 peak on October 4 to its low on Christmas Eve, the price of a barrel of Brent crude oil fell 38%. Since then, it has climbed steadily higher and now sits 42% above its trough.

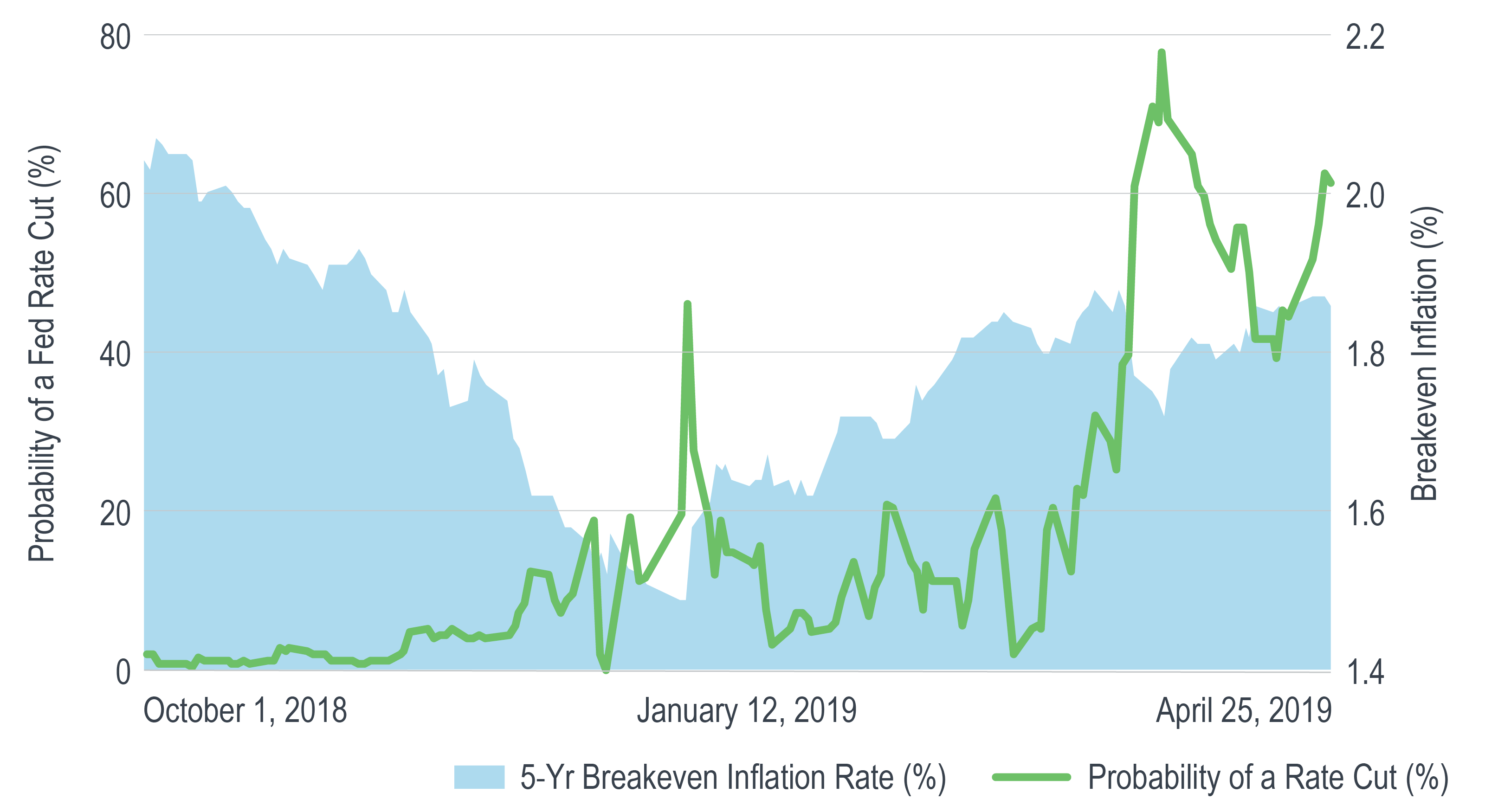

As the price of oil has moved, so too have inflation expectations. The 5-year breakeven inflation rate is a gauge of inflation expectations – measured by the difference between the yield of the 5-year Treasury bond and the yield of the 5-year Treasury Inflation Protected Security (TIPS).

Similar to the performance of the stock market over this period, the reversal in the price of oil coincides with the Fed’s reversal in its policy stance.

Counter-intuitively, during the second half of April, the futures-implied probability of a Fed rate cut before the end of 2019 has climbed from 39% to 67%.

How can it be that the market expects higher inflation on the one hand, while expecting a Fed rate cut on the other? It seems that one of these projections must eventually be proven wrong.

Rising oil prices and inflation expectations, along with the much-higher-than-expected Q1 GDP growth, may not increase the likelihood of a rate hike any time soon.

If those trends persist, however, it’s difficult to see how they won’t eventually put downward pressure on the likelihood of a rate cut.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.