Summary: NDX is now at a new all-time high (ATH). Leadership by NDX is a positive for SPX: historically, the risk/reward over the coming weeks and months for SPX has been excellent.

On an equal-weigh basis, both SPX and NDX are also at new ATHs. Any weakness in breadth is almost exclusively explained by the healthcare sector. The other sectors, aside from utilities, have all reached new YTD highs in the past week.

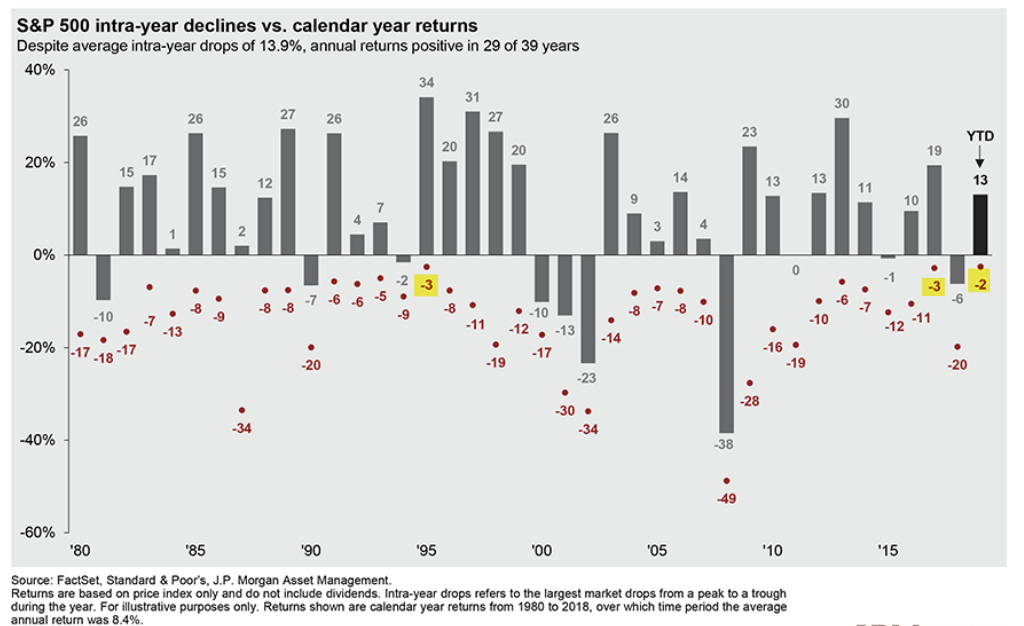

Volatility has been unusually low so far this year. By one measure, this is one of the least volatile starts to a year in the past 90 years. That's unlikely to last. The largest reaction so far this year has barely been more than 2%. Going back 40 years, no year has seen a lower drawdown and all but two (95%) have seen a drawdown of at least 5%. With SPX now within 1% of its prior ATH, a meatier reaction is odds on in the weeks and months ahead.

US equities continues to grind higher. With about a week to go in April, SPX, NDX and DJIA are on pace to rise in each of the first 4 months of the year. The leader is NDX, which has risen 6 weeks in a row and 16 of the last 17 weeks since Christmas Eve (table from alphatrends.net). Enlarge any chart by clicking on it.

In January, we noted that SPX was likely to grind its way higher as the volatility index, VIX (lower panel), sunk under 16, just as it had in 2018. That remains the case, and SPX is now less than 1% from its all-time high (ATH) of 2930 set in September.

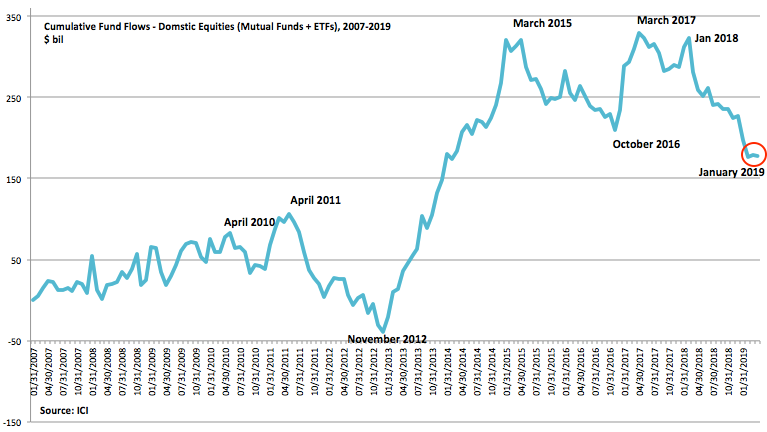

Investors have reluctantly embraced the rise in equities. Through mid-April, US equity ETF and mutual fund flows have been net negative. While anything is possible, it's hard to imagine this being the context of an important top (from ICI).

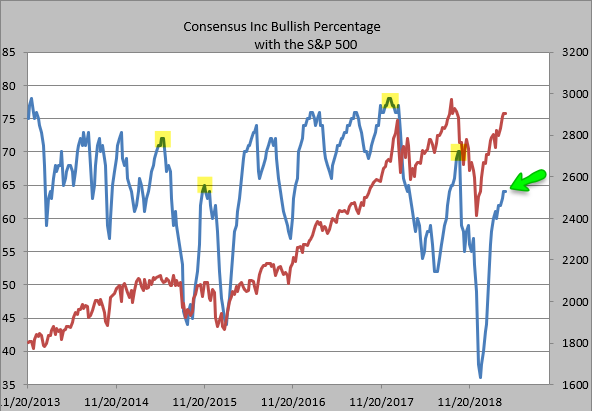

Likewise, despite a strong 4 month rally, sentiment amongst analysts has not rebounded that strongly (blue line). Bulls climbed back to just 64% this week; rallies in the past 8 years have not fizzled out until bulls were at least 65% (like late-2015) and more often when bulls were at least 70% (like July 2015 and both January and September 2018). Could SPX peak here? Yes, but it could just as well grind higher until sentiment is more clearly at an extreme (from Helene Meisler).

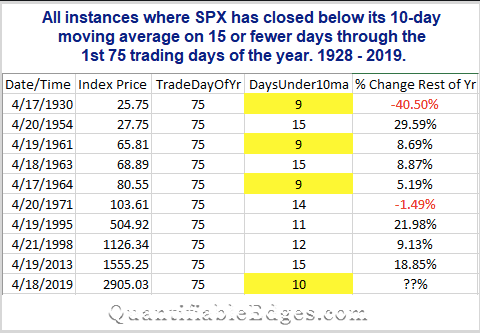

One of the more remarkable aspects of the current market is the persistence of the rally. Through the first 75 days of the year, SPX has closed below its 10-dma on only 10 days. In the past 90 years, this has only happened 9 other times. The last three times - 1995, 1998 and 2013 - all added 9% or more through year-end. That has been the general pattern for these types of years and you'd have to go back to the start of the Great Depression to find an instance where the equity markets fell into a bear market in the months ahead (from Quantifiable Edges).

VIX remains subdued. These periods can last for months, even years (yellow shading). Two of the years mentioned above - 1995 and 2013 - were similar. There is nothing inherently unstable or unsustainable about these low volatility periods

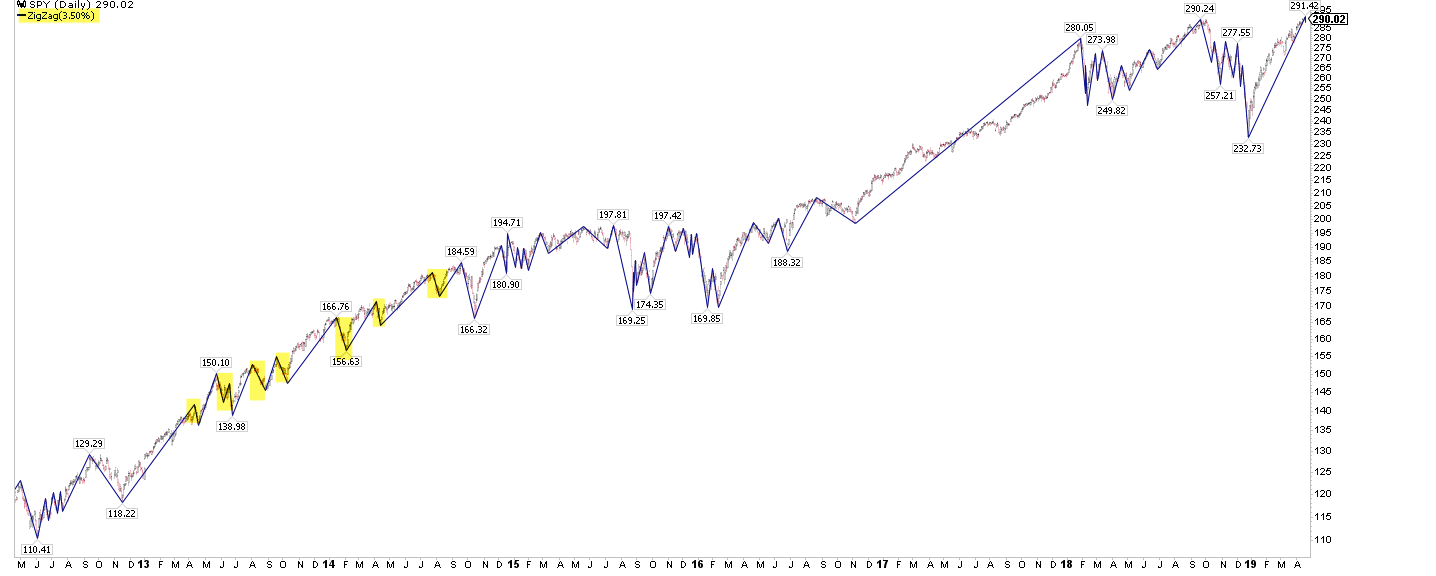

That obviously doesn't preclude periodic jumps in volatility. In 2013-14, VIX jumped from around 12 to 16-20 on 10 different occasions.

In fact, that is an odds-on event. There have been just three notable drops in SPX since January, each spaced about a month apart and the last one was a month ago (yellow shading). Each occurred near an area of resistance, which is notable now as SPX is within 1% of prior resistance at 2930. A reaction seems likely.

The largest reaction so far this year has barely been more than 2%. Going back 40 years, no year has seen a lower drawdown and all but two (95%) have seen a drawdown of at least 5%. A meatier reaction is odds-on in the weeks and months ahead (from JPM).

Between April 2013 and September 2014, VIX mostly stayed under 18 yet SPX dropped at least 3% on 7 different occasions. It was a persistently low volatility period but temporary setbacks were normal about every other month. This should be expected in 2019 as well.

May and June are just ahead. Historically, these are not great months for SPX. Anything can happen, but this wouldn't be an unusual time period for the uptrend to weaken a bit, as it did in both 2013 and 2014 (from (from Ryan Detrick).

On the calendar this week: new home sales on Tuesday, durable goods on Thursday and GDP for 1Q on Friday. Of more consequence, the following week includes an FOMC meeting on Wednesday and the employment report on Friday (from IBD Investors; for a trial subscription, please use this link).

© The Fat Pitch

Read more commentaries by The Fat Pitch