U.S. stocks continue to trend higher, indicating investor optimism about economic growth, while a flat/inverted yield curve has tended to herald a weakening economy—the truth may be somewhere in between.

Mixed economic data continues into the second quarter, and earnings season has just begun. A negative quarter for S&P 500 earnings is expected, but it’s not only whether the bar has been set too low that will be important—but what the tone of the forward looking commentary suggests about the broader economic outlook.

An international economic barometer is approaching a historically critical level, while Brexit drama is extended.

“Creativity comes from a conflict of ideas.” ― Donatella Versace

Investor conflict

Conflicting opinions are what makes markets work—you believe the price of a stock is going higher, while we think it’s not, we sell to you—but there appears to be a fairly large difference in opinion this year between stock and bond investors. Stocks have had a remarkable run since the Christmas Eve 2018 low, and have easily overcome a few bumps in the road, suggesting that stocks are telling a story of a near-term economic soft landing and a recovery shortly thereafter.

Stocks indicate confidence…

The bond market appears to be telling a much different story. The yield curve has flattened substantially, even inverting recently (with the 10-year Treasury yield moving below the 3-month T-bill yield). Theoretically, this could at least partially indicate a lack of confidence in future growth prospects. If investors are willing to have their money tied up for ten years at ever lower rates, the confidence in future economic growth is likely not particularly strong.

…but bonds appear to be telling a different story.

So which story is right?

As is often the case, there may be some truth to both stories. So far this year, the stock market has behaved mirror image fashion relative to 2018. Last year was a story of multiple contraction (lower P/Es), even though earnings (the E) were stellar. The contraction was a function of tightening financial conditions; but also the weak outlook for 2019 earnings. Remember, stocks tend to discount the future. This year has been a story of multiple expansion (higher P/Es), even though earnings estimates (the E) have been lowered according to Refinitiv estimates. The expansion has been a function of loosening financial conditions in our view; but we’re probably at a stage now where earnings are going to have to do some more of the market’s “heavy lifting.” Stocks may be increasingly vulnerable to a pullback as investor sentiment has recently moved well back into the extreme optimism zone (a contrarian indicator). The bond market is also being influenced by negative interest rates in several international regions, which appears to be pushing investors into higher-yielding U.S. securities; while also expressing confidence that inflation will remain contained.

What does the scoreboard say?

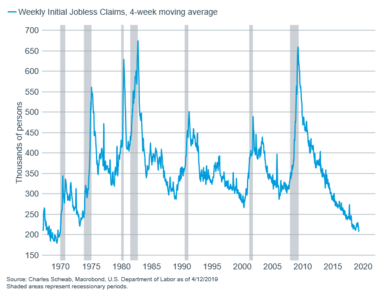

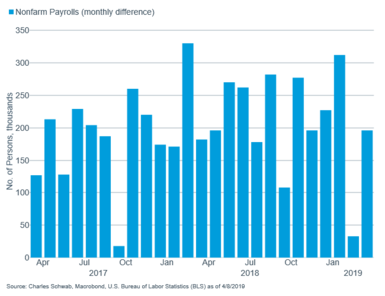

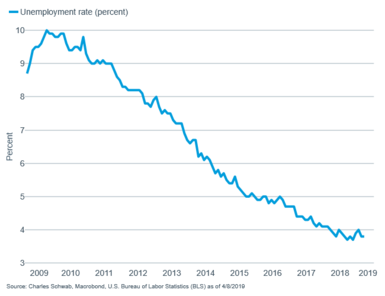

Both sides can point to different economic data points to bolster their arguments. For those more optimistic side, the labor market remains strong, with jobless claims recently hitting a 50-year low, while the March jobs report showed a robust 196,000 in payroll gains, making the weak February report look more like an outlier. The unemployment rate remains at a historically-low 3.8%, although average hourly earnings surprisingly dipped a bit from a gain of 3.4% to 3.2% on a year-over-year basis.

Claims indicate strong labor market

While job growth has rebounded

And unemployment remains historically low

Additionally, the Institute for Supply Management’s (ISM) Manufacturing Index bounced in March to 55.3 from 54.2, while the new orders component also rose nicely from 54.2 to 57.4. This improvement likely reflects some optimism that a trade deal between the United States and China will be coming in the near term. Although there’s ample reason to keep enthusiasm curbed for a near-term comprehensive deal, it would likely remove a major source of corporate uncertainty.

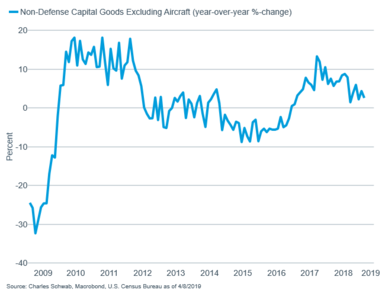

Not all is rosy though. A more pessimistic view can be shaped from other recent releases. Retail sales in February fell 0.2% from the previous month, durable goods orders fell by 1.6%, and orders for non-defense capital goods ex-aircraft—considered a proxy for business spending fell 0.1%—continue their declining trend.

Durable goods orders trending lower

On the services side, the March ISM Non-Manufacturing Index fell from 59.7 to 56.1, while the new orders component was also weaker, dropping to 59.0 from 65.2. On the trade front, pessimists could easily point to the fact that there is still no firm China-U.S. deal, the threat of European auto and airline subsidies tariffs has escalated (with retaliation likely coming from the European Union), and the growing likelihood that the USMCA (former NAFTA) will have trouble getting through Congress. We would be remiss if we didn’t also mention the possibility of a border shutdown between the United States and Mexico, recently threatened by President Trump; Caveat: he recently said there would be a “one-year warning” on such an action, but that tariffs on autos from Mexico are also possible. We try to avoid the partisan scrum and focus on actual policy implications for the economy and markets, but shutting down the border with Mexico would likely bring swift economic damage; with even Trump admitting that, “Sure it’s going to have a negative impact on the economy” (The Wall Street Journal).

In the midst of this mixed economic picture, first quarter earnings season could have a large impact on stock market action over the next few weeks. With estimates currently at -2.5% year-over-year growth (Refinitiv), expectations are muted; but what’s equally important will be comments about the future outlook by corporate executives.

And the winner is?

For now, we a will call the battle between stock and bond investors a draw. The mixed picture painted above gives fuel to both sides, which is why we continue to suggest investors not chase the recent stock rally and maintain a mostly neutral–to-slightly-defensive stance both at the macro and micro level. The history lessons of late-cycle eras suggests investors need to focus on the tried-and-true disciplines of patience, diversification and periodic rebalancing, while keeping an eye on long-term goals.

Brexit: Endgame

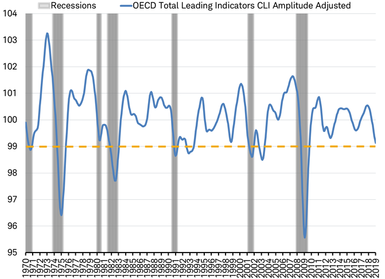

The composite leading indicator for the world economy from the OECD (Organization for Economic Co-operation and Development) is approaching a potentially significant threshold, as can be seen in the chart below. Over the past 50 years, a drop to 99 seems to happen right around the start of global recessions: in early 2008, early 2001, late 1990, late 1981, mid 1974, and mid 1970. The indicator has never crossed 99 and not been accompanied a recession. It's now at 99.1.

Leading indicator for the world economy

Source: Charles Schwab, Bloomberg data as of 4/10/2019.

A rebound in this indicator from the current level, as we last saw in 1998, would be welcome news. Despite this week’s downward revision to 2019 global economic growth estimates by the IMF (International Monetary Fund), there have been some signs of stabilization in global economic data. However, there are developments in the near future that could prompt further weakness, like revived trade tensions between the U.S. and Europe, mentioned above, or an abrupt and disorderly Brexit.

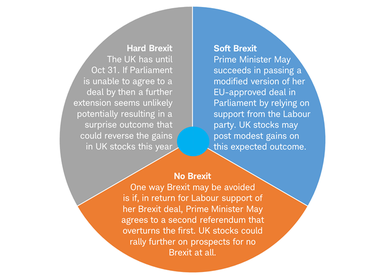

Avengers: Endgame is predicted to smash box office records upon its release later this month, but just as widely-watched is the drama over the Brexit endgame. This week, the U.K. was granted a widely-expected second exit date extension to October 31, with the option to leave earlier. We see three main scenarios the path of Brexit may take over the coming months, each with differing market outcomes.

Brexit: three main scenarios

The policy analysis provided does not constitute and should not be interpreted as an endorsement of any political party.

Hard Brexit: One way an abrupt and disorderly U.K. exit from the European Union could still happen is if Parliament is unable to agree to a deal by October 31. A further extension seems unlikely given likely opposition by French President Macron, it only takes one of the other 27 EU member nations to veto an extension. This unanticipated outcome could reverse the gains in U.K. stocks and the British pound seen this year.

Soft Brexit: Prime Minister May could succeed in passing a modified version of her EU-approved withdrawal agreement through Parliament by relying on support from the Labour party. A deal could still be ratified by the U.K. Parliament by May 22, in time for the U.K. to leave the EU at the end of June and avoid participating in European Parliament elections, but seems unlikely given divisions within the U.K. Parliament. While a version of this scenario seems to be anticipated by markets this year, U.K. stocks and the pound may post modest additional gains with further confirmation toward an eventual “soft” Brexit.

No Brexit: In exchange for the Labour party’s support for a modified version of her Brexit deal, Prime Minister May might have to agree to a second referendum where British voters would be given a final chance to choose between May’s version of Brexit or no Brexit at all. Alternatively, a power struggle among conservatives to replace May could delay progress on an agreement by October 31, prompting the U.K. to revoke Article 50 to stop the clock on Brexit. U.K. stocks and the pound could rally further on a heightened probability of no Brexit at all.

It is difficult to place probabilities on these three political outcomes, but the stock market seems to be expecting that a hard Brexit will be avoided since U.K. stocks are up a little over 10% (according to the FTSE 100) so far this year. If this worst-case scenario can be avoided, along with the negative economic consequences it is expected to bring, it may also be good news for the global economy as the global leading indicator nears an important threshold.

So what?

Stocks and bonds appear to be at loggerheads with regard to the economic outlook, and we believe both sides have merit. Unless earnings comfortably surprise on the upside, with healthy corporate guidance, there is a risk that stocks will give back some of their recent gains. Investor optimism remains elevated, economic data has been mixed, earnings expectations are in the red for the first quarter, and persistent trade concerns all remain potential headwinds. Stay patient and diversified and stay focused on longer-term goals.