Last Friday’s payroll report was generally cheered as having Goldilocks characteristics, but a closer look is warranted.

Wage growth was weaker-than-expected, with low wage industries in the spotlight; while manufacturing employment data is also troubling.

Layoffs are picking up, while consumers are worried about future job opportunities.

The monthly payroll report is always closely scrutinized by economists and market watchers; perhaps even more so these days given the Federal Reserve’s decision to shift into neutral/pause mode earlier this year. After a dismal February, payroll growth rebounded in March; with nonfarm payrolls rising a higher-than-expected 196k, and slight upward revisions to the prior two months. The unemployment rate remained at 3.8%, which is slightly above a 49-year low; while the labor force participation rate dipped. Average hourly earnings (AHE) represents the proxy for wages, and they were up a less-than-expected 3.2% relative to a year ago—down from 3.4% in February. (AHE for production and nonsupervisory workers was up a little more at 3.3% year-over-year; and is the wage proxy in the charts below.)

Goldilocks?

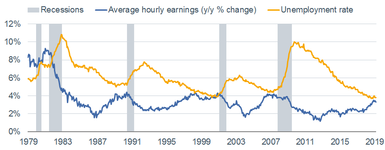

Friday’s report was generally cheered as Goldilocks—not too hot, not too cold. But digging into the details yields some concerns worth noting. The number of jobs gained or lost each month comes from the payroll survey; while the unemployment rate comes from the household survey. Payroll gains averaged 180k per month in the first quarter, which is lower than last year’s average of 223k. Household employment actually fell by 197k in the first quarter, 48k of which was in the prime working age (25-54) category. That category has seen employment losses in four of the past five months. In addition, temporary employment, which is a leading indicator of job growth, fell by 5k. It’s too soon to judge whether the weaker month-over-month and year-over-year AHE gain is a sign of a top in wage growth, but the convergence between the unemployment rate and AHE is worth watching as a recession indicator. As you can see in the chart below, historically once wage growth rolled over and the unemployment rate began to elevate, a recession was either underway or imminent.

Wages & Unemployment Converging

Source: Charles Schwab, Department of Labor, FactSet, as of March 31, 2019. Average hourly earnings for production and nonsupervisory workers.

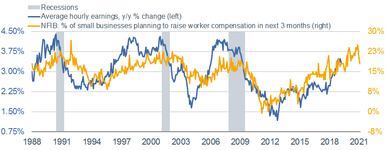

There had been high hopes for higher wage growth. The widely-watched monthly small business survey from the National Federation of Independent Business (NFIB) has as one of its survey questions whether member companies are planning to raise worker compensation. This percentage has historically led AHE changes by about two years, as you can see in the chart below (the NFIB line is advanced two years). Until the latest release, the surge in the percentage of small businesses planning to raise worker compensation in the next three months—from a recession low of 0% to the recent high of 25%—pointed to higher wage gains to come. The latest down move down to 18% will be troublesome if it persists; but a rebound would provide hope for higher wage gains to come.

Small Business Compensation Plans Faltering

Source: Charles Schwab, Department of Labor, FactSet, National Federation of Independent Business (NFIB). Average hourly earnings for production and nonsupervisory workers as of March 31, 2019. NFIB advanced 24 months and as of February 28, 2019.

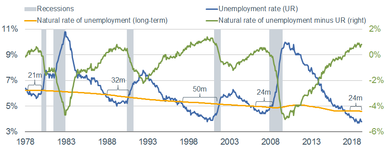

There may still be a decent length of runway between now and the next recession, but there’s little doubt we are late in the cycle. It’s been 24 months since the unemployment rate crossed (fell below) the “natural rate” of unemployment. It’s a concept pioneered by Milton Friedman and refers to the hypothetical unemployment rate consistent with aggregate production being at the long-run level; or when the economy is in a steady state of “full” employment. As you can see in the chart below, it was 24 months between the time of the cross and the start of the 2007-2009 recession; although it was a longer 50 months between the cross and the 2001 recession. We should certainly hope for a longer runway this time, but any sustainable uptick in the unemployment rate would be a troubling sign based on history.

Unemployment Rate Well Below Natural Rate

Source: Charles Schwab, Department of Labor, FactSet, U.S. Congressional Budget Office, as of March 31, 2019.

Lower-wage industries in spotlight

The largest payroll gain among private sector categories was the generally lower-wage education and health services, which represented more than 38% of private sector job gains. Related, hiring trends excluding the lower-wage industries of retail, health and restaurants has faltered, as you can see in the chart below. From a peak last April of nearly 180k on a three-month moving average, it has fallen to under 100k today.

Weaker Payrolls Ex Low Wage Industries

Source: Charles Schwab, FactSet, as of March 31, 2019. *Low wage industries: retail trade, education and health services, leisure and hospitality.

With weaker growth in higher-wage industries, it’s a simple math equation that gets us to slower overall wage growth than what was expected. With all the chatter about (and survey results showing) the quality of labor/skills shortages, it was expected that wage growth would continue to gain traction.

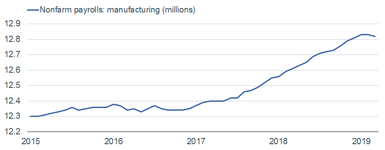

Manufacturing faltering

Employment-related weakness is particularly notable within manufacturing. Although perhaps it’s too soon to declare a peak, there has been a flattening out and slight dip in manufacturing payrolls, as you can see in the chart below. There was a loss of 6k manufacturing jobs in March, with an additional 2k job losses in wholesale trade.

Manufacturing Employment Rolling Over?

Source: Charles Schwab, Department of Labor, FactSet, as of March 31, 2019.

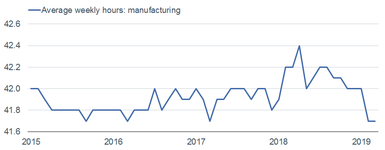

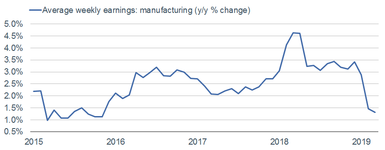

Also weakening has been average weekly hours within manufacturing—from a 2018 high of 42.4 to 41.7 as of March, as you can see in the first chart below. Given the cut to hours, average weekly earnings for manufacturing workers has also dropped sharply, from a high of 4.6% year-over-year growth in last year’s first half, to only 1.3% as of March, as you can see in the second chart below.

Weaker Manufacturing Hours/Earnings

Source: Charles Schwab, Federal Reserve Bank of St. Louis, as of March 31, 2019.

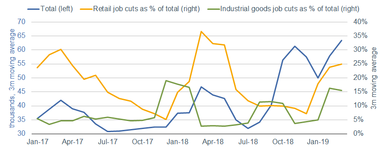

Claims data still healthy, but layoffs picking up

Unemployment claims—an important leading indicator for the economy—continue to plumb lows not seen since the late-1960s. However, layoffs tabulated by Challenger, Gray & Christmas have been moving up. From the recent low of 32k last July, the three-month moving average of layoffs has doubled; with retail representing the largest share (no surprise there given retailers have announced plans to shutter more than 4k stores so far this year). On a cumulative basis, employers cut a total of more than 190k jobs in the first quarter, which is more than 10% higher than last year’s fourth quarter, and more than 35% higher than the same quarter last year. The recent increase in job cuts by industrial goods firms is worth watching; and it’s in keeping with the aforementioned weaker manufacturing employment trends.

Challenger Layoff Announcements

Source: Charles Schwab, Challenger Gray and Christmas Inc., FactSet, TS Lombard, as of March 31, 2019.

Confidence faltering

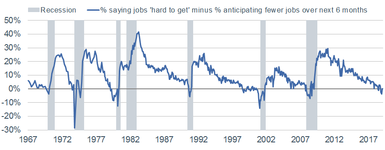

A final “worth watching” statistic comes from The Conference Board’s monthly Consumer Confidence survey. Two of the questions asked in the survey are whether respondents are finding that jobs are “hard to get” and whether they anticipate fewer jobs over the next six months. The difference between the two is charted below. As you can see, this measure recently breached the zero line and moved into negative territory. This has historically been an indication of imminent recession risk; so again, it’s worth watching.

Consumer Confidence Jobs Survey

Source: Charles Schwab, FactSet, The Conference Board, as of March 31, 2019.

I try not to be a Debbie Downer, but with all the cheering of a “Goldilocks” jobs report at this stage in the economic cycle, it’s crucial to test the temperature of her porridge. Ideally it stays warm for some time to come; but the risk is it goes from hot to cold sooner than anticipated, so we need to be on guard.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Thumbs up / down votes are submitted voluntarily by readers and are not meant to suggest the future performance or suitability of any account type, product or service for any particular reader and may not be representative of the experience of other readers. When displayed, thumbs up / down vote counts represent whether people found the content helpful or not helpful and are not intended as a testimonial. Any written feedback or comments collected on this page will not be published. Charles Schwab & Co., Inc. may in its sole discretion re-set the vote count to zero, remove votes appearing to be generated by robots or scripts, or remove the modules used to collect feedback and votes.