Closing the Gulf: How the GCC Countries Fit into our Emerging Debt Investment Process

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEXECUTIVE SUMMARY

The inclusion of five Gulf Cooperation Council (GCC) countries as of January 2019 into the benchmark EMBIG index represents one of the largest onetime index adjustments in recent memory. By the time the GCC countries are fully phased into the benchmark later this year, they will collectively account for about a 12% weighting, from virtually zero. Inclusion of these countries will increase the overall credit quality of the benchmark, lower its yield, and increase its exposure to oil price fluctuations. We use this as an opportunity to remind readers of our country risk process, highlighting some of the unique characteristics of these countries, how they fit into our relative valuation framework, and what this important market development means for our external debt portfolios.

Introduction

On January 31, 2019, J.P. Morgan, which manages the EMBI suite of emerging market bond indices, added five new countries of the Gulf Cooperation Council (GCC)1 to the external debt benchmarks. This addition represents the largest ever one-time adjustment to the index that our foreign currency sovereign debt funds have historically used as a benchmark. Therefore, we take this opportunity to make clients aware of the change, including how these countries fit into our country risk framework, and how they might fit into our portfolios.

Why and how?

According to data compiled by Bank of America, total sovereign and corporate bond issuance from the GCC has accelerated in recent years. Prior to 2014, when oil prices collapsed from their lofty levels well above $100 per barrel, gross bond issuance from the region averaged about $27 billion per annum. Beginning in 2016, after the realization that the oil price shock was going to be persistent rather than transitory, annual issuance has more than doubled to $66 billion. It is likely that the index provider was being pressured by a number of stakeholders to recognize this heightened level of issuance, which amounted to roughly 4-5% of the region’s combined GDP. To be sure, GCC countries drew down assets and tapped domestic pools of savings to offset the lower revenues from oil, but they also chose to borrow from foreigners in larger amounts, a rather unfamiliar feeling for a region normally accustomed to being a creditor.

GCC countries (aside from Oman) have heretofore not met the inclusion criteria for the EMBIG because gross national income per capita was above the threshold deemed to be applicable to emerging countries (currently around $19,000 per annum). In other words, they were too rich, even though they displayed other attributes of emerging countries, such as acute income inequality and weak democratic institutions, among others. The workaround adopted by J.P. Morgan came in the form of an additional inclusion criterion, which it calls the “PPP ratio” – essentially a measure of development because it measures a country’s level of purchasing power per dollar. Less developed countries will have more purchasing power per U.S. dollar than developed countries, due to the overall level of prices and other factors. When this ratio is set at 0.6 (crudely, $60 would buy a similar “basket of GDP” in country “X” than $100 would buy in the U.S.), it conveniently covers the GCC countries, allowing them – but no other previously excluded country – to be included.

What does it mean for the index?

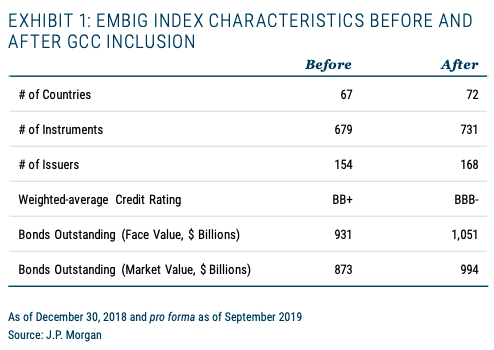

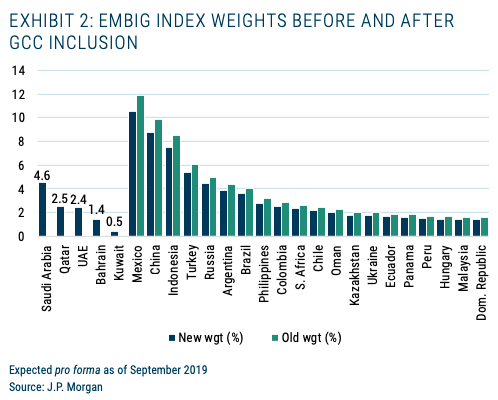

In order to prevent market dislocation, the five GCC countries will be phased into the index over nine months, through September 2019. Exhibits 1 and 2 show some pro forma estimates, subject to change depending on the issuance patterns in the market during the transition, of how the EMBIG benchmark will change, assuming full inclusion. About $120 billion of bonds are being added to a benchmark that finished last year with a market capitalization of $873 billion. The number of countries rises to 72, the highest it has ever been, with commensurate increases in the number of issuers and instruments (remember, this benchmark also includes quasi-sovereign issuers from included countries). Importantly, the weighted-average credit rating of the index will rise back to investment grade (BBB-), from BB+, assuming current ratings. Three of the five countries – Kuwait, Qatar, and UAE – are in the double-A rating range. The past few years have seen the EMBIG’s weighted-average rating fall, with important downgrades of some of the larger countries, such as Brazil, Russia, and Turkey. Upon full inclusion, the five new GCC countries will represent 11.4% of the index, which is a huge change in one year. To put it into perspective, we have observed China’s weight rise from around 2% to near 10%, but this happened over a 6-year time frame. Sub-Saharan Africa has gone from virtually zero weight to about 4%, but this increase evolved over 10 years.

Country Risk and Relative Value

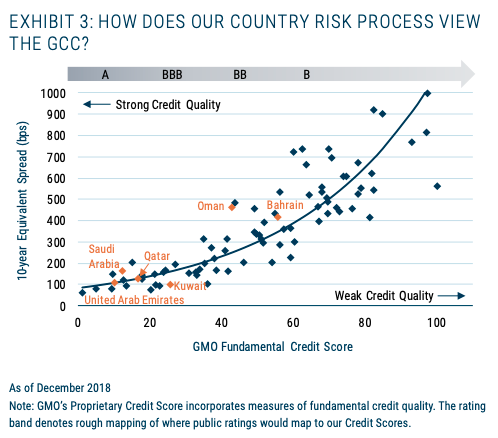

Over the past several months, in anticipation of the inclusion event, we have added the GCC countries not previously covered to our country risk coverage universe. Our primary approach is to insert the countries into our existing country risk model, which measures country risk across the three quantitative factors of each country’s economic structure, fiscal sustainability, and external liquidity conditions. Through a series of regressions we estimate coefficients that measure the relative importance of the three factors, and calculate an overall risk score, which we normalize on a scale of 1 to 100 (low risk to high risk). Once we have a risk score, we can plot it alongside bond spreads to obtain an estimate of fair value, and relative value to other countries. Exhibit 3 shows this plot for our most recent model run, with the countries of the GCC labeled for emphasis. Each dot represents a country in our model, and the non-linear regression line through the scatter plot provides an estimate of fair value. Countries whose dot lies above the line are cheap, by our assessment, and countries below the line are rich.

There is a clear bifurcation among these six countries (the five additions, plus Oman) in terms of their country risk and spreads. Our model places Kuwait, Qatar, Saudi Arabia, and UAE squarely within the high credit quality (and low-yielding) camp, while Bahrain and Oman are clearly of lower quality. This result is consistent with the views of the public rating agencies. All six countries score well in our definition of economic structure, one component of which is GDP per capita. We take the view that rich populations are more able to absorb shocks than poor populations, and are therefore more likely to adopt policies in order to avoid debt default. These Gulf countries are all relatively rich on this basis. The average GDP per capita of the countries in the benchmark is about $10,000 per year, while the GCC countries range from $19,000 (Oman) to near $70,000 (Qatar). With this per capita wealth comes higher average health and education levels, better infrastructure, and other attributes.

In terms of our model’s assessment of fiscal sustainability and external liquidity conditions, this is where the bifurcation is more pronounced. The four stronger credits have much more solid metrics on both of these factors. Our model considers “flow” variables like fiscal and balance of payments deficits, as well as “stock” variables, such as public debt and foreign exchange reserves. This region scores much more strongly on the stock variables, via the accumulation of surpluses generated in the years before 2014. The flow variables have deteriorated in recent years due to the fall in oil prices, but they all had strong buffers to begin with. Oman and Bahrain had weaker buffers at the onset of the oil price collapse, and worse deficits (more delayed policy adjustment) since the oil price collapse, which is why they are in a different (weaker) risk category.

We will continue to monitor the country risk profile of this region. We take some comfort in the fact that, over the past 10-12 years, the region has been hit with three major shocks, all of which were navigated reasonably successfully. The first was the global financial crisis in 2008-09, which the region came through, not without recessions, but without major financial upheaval.2 The second was the Arab Spring of 2011-12, during which populations rose up against authoritarian regimes in the Middle East and North Africa. Again, the GCC region was not unscathed by these events, but the monarchies have survived through a combination of repression, regional cooperation (it is in no one regime’s interest to see another fall in such a closely-knit space), and, importantly, some concessions to civil society. This leads us to the most recent shock – the oil price collapse that began in 2014. These concessions to society cost money, and most GCC countries, apparently, thought $100-plus oil was here to stay. By 2014, the breakeven oil price – the price at which the state budget would be balanced – had risen to $100 per barrel in Bahrain, Oman, and Saudi Arabia, leaving them highly vulnerable. The policy response of the region since the oil price collapse, once it became clear it was a longer-term regime shift, has been a combination of: a) asset drawdown (savings from previous surpluses); b) market borrowing to fund the deficits (hence, the reason we find ourselves writing this piece); and c) fiscal consolidation (to reduce that breakeven oil price figure). The first two are shorter-term in nature, while the third is the one that will determine each country’s longer-term trends in creditworthiness.

To conclude, these countries have demonstrated remarkable resiliency over the past 12 years or so, and while the authoritarian nature of the governments might be a cause for concern on a number of levels,3 from a pure sovereign credit perspective, there are some advantages. The governments comprising various forms of parliamentary democracies, which make up the vast majority of our investment universe, are often hamstrung by politicians who cannot (or will not) see beyond the next election (we’ve recently seen the effects of this in countries as diverse as Costa Rica, Ukraine, Brazil, and Kenya, among many others). Monarchies, by their nature, tend to think “multi-generational.” This is not to argue in favor of monarchies, but rather to state that their existence in our investment portfolio need not reduce its credit quality.

Implications for the Emerging Debt Portfolios

We highlight three implications for our external debt portfolios.

First, we note that our portfolios have already been invested in Saudi Arabia, Qatar, Bahrain, and Oman for some time, the first three having been off-benchmark (now in-benchmark) positions we’ve held due to valuation considerations and as a potential source of alpha. Referring back to Exhibit 3, we have viewed Saudi Arabia as attractive at the strong high-grade end of the credit spectrum, especially relative to other inbenchmark countries such as Chile, the Philippines, Peru, and Poland, among others. Oman and Bahrain occupy the mid-range of our credit spectrum, but the market prices them as single-B credits. It is difficult to find mid-range credit quality at very high spreads. These are often countries that are relatively strong credits but on a declining credit trajectory (other countries currently in this space are Turkey and Costa Rica). The assessment here depends in part on a view that policymakers want to avoid a self-inflicted debt crisis and will pivot economic policy in a way that stabilizes creditworthiness. It doesn’t always happen this way, but it often does, perhaps with the assistance of an International Monetary Fund program. Moreover, in the case of Oman and Bahrain, we find opportunities for security selection. For example, their bond curves tend to be very steeply sloping, offering an outsized term premium in spreads.

Second, there should be alpha opportunities from the plethora of quasi-sovereign corporates in the GCC region. In terms of pure benchmark inclusion, there will be an additional nine quasi-sovereigns entering the benchmark from the five new countries. However, our quasi-sovereign research team has identified and modelled about 40 others that we consider “fair game” – companies that might have less than 100% state ownership (and therefore not index-eligible) but have strong state sponsorship nevertheless. We will be focusing on this sector of the market in 2019, especially for those countries for which we see relatively less value in the sovereign debt, such as Kuwait, UAE, and Qatar.

Finally, the correlation with oil prices is likely to increase with the addition of these countries. We calculated one-year trailing correlations of weekly oil price moves and the spread return of the EMBIG index. We found that in the 10 years before the Lehman collapse, that correlation averaged around 0.09, while in the 10 years following the crisis, the average correlation quadrupled to 0.38, with major spikes in correlation occurring around the times of the sudden declines in oil prices. We calculate, using data from UNCTAD, that the percentage of the benchmark that we would consider oil dependent (countries in which oil and its derivatives account for at least 25% of exports) was around 18% before the GCC inclusion, and will be at least 28% after the full GCC inclusion. This might understate the benchmark’s true oil dependency, because there are some countries, like Mexico, where oil exports are low, but fiscal revenues from oil production are high. However, it should be a decent proxy that between one-quarter and one-third of the benchmark will be heavily dependent upon oil. Given our bottom-up approach and heightened focus on “alpha” rather than “beta” considerations, this trend will not preoccupy us, but it is something we will be aware of in the overall risk management of the portfolios.

1 GCC countries are Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates. Oman, the poorest of the six, is the only country that had been included in the index previously. The other five are being added over time.

2 It is sometimes forgotten that there was a massive oil price collapse (from $140 per barrel on Brent to about $50) during the global financial crisis, but unlike the 2014 oil price drop, it was more temporary.

3 We note that all of these countries have ESG scores that place them well within the eligibility criteria for the J.P. Morgan ESG version of the emerging debt benchmark.

Carl Ross Dr. Ross is engaged in research for GMO’s Emerging Country Debt team. Prior to joining GMO in 2014, he was a managing director at Oppenheimer & Co. Inc. where he covered emerging debt markets. Previously, he was the Senior Managing Director and Head of Emerging Markets Fixed Income Research at Bear Stearns & Co. Dr. Ross earned his BA in Economics from Mount Allison University as well as his M.A. and PhD in Economics from Georgetown University.

Disclaimer

The views expressed are the views of Carl Ross through the period ending March 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2019 by GMO LLC. All rights reserved.

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All