Bending, Not Breaking

The global slowdown that began last year has continued to spread. The U.S. economy has shifted into a lower gear, growth has been falling in the Eurozone, Brexit is festering and China is feeling the heat from internal imbalances and an elevated trade spat with the U.S. Economic activity in all regions will continue to be hindered by the uncertainties surrounding global commerce.

We remain optimistic that these uncertainties will not extend beyond 2019. A de-escalation of US-China trade tensions is in the offing; there are reports a deal could be reached before the end of the month. Brexit remains messy, but the paths to resolution have become somewhat clearer in recent weeks. Should these two situations reach resolution, confidence among consumers, producers and investors will improve.

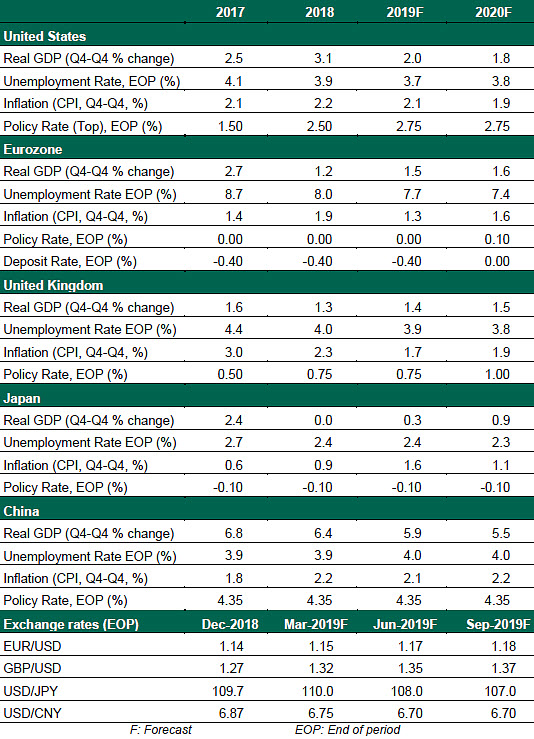

Overall, we continue to call for the global economy to reach a soft landing. Downside risks remain, and must be carefully managed. Following are our views on how the main world markets will likely fare in 2019 and 2020.

United States

- Economic growth in the U.S. is entering a period of transition, with fourth-quarter 2018 real gross domestic product (GDP) growing at a 2.6% annualized pace. The economy grew 3.1% for the full year, in line with the administration’s projections included in its proposal for the Tax Cuts and Jobs Act. The recent tapering marks the start of a trend that, in the best case, will be a soft landing for the U.S. As stimulus measures fade and global growth cools, we expect economic growth to continue at a more measured rate during the balance of 2019.

- Inflation remains calm, with the January Consumer Price Index (CPI) increasing only 1.6% year over year. Core CPI, excluding food and energy, grew at a more firm rate of 2.2%. Steady inflation and slower growth are just two of the reasons the Federal Reserve has struck a theme of patience in the year ahead, waiting for data to make a strong case for rate increases. We anticipate one rate hike later in 2019 to end the cycle of rate increases. Focus is turning to the Fed’s balance sheet reduction, which is likely to end later this year.