Is the Past Prologue or Is It Different This Time?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn this Octavia’s Outlook I quickly look back at 2018 stock market performance. I then look forward at the forces which I believe will drive global stock markets. Finally, I share how these forces influence my thinking in constructing investment portfolios. I know my letters can run long, so to shorten this letter I will not include much in the way of supporting data but instead just share my conclusions.

2018 in Review

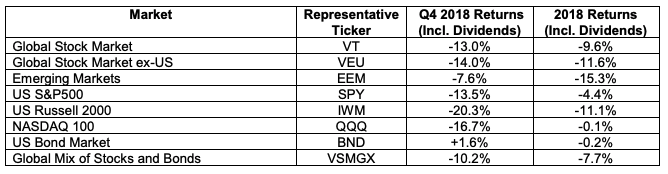

Global stock markets excluding the US had a poor year from start to finish, ending the year down 11.6%. US stock markets, on the other hand, started the year strongly but had a very weak Q4. And, US stock market performance was mixed across size, where the S&P 500 (large companies) declined 4.4% in 2018 while the Russell 2000 (small companies) declined 11.1%. Large growth companies, as represented by the Nasdaq 100, were basically unchanged in 2018.

Bonds did not help in 2018, with the US bond market basically unchanged in 2018. While bonds are typically less volatile than stocks, they will not necessarily go up when stocks go down. In fact, in some ways stocks and bonds are now positively correlated since rising interest rates can lead to declines in the prices of both stocks and bonds. This is an important concept to understand. The traditional view of holding a 60% stocks / 40% bonds portfolio where when stocks go up, bonds go down, and vice versa, may not hold going forward and should not be blindly trusted to act as a buffer against portfolio volatility.

Q4 was very challenging for US stock markets due to both fundamental factors and technical factors.

Fundamental Factors

All financial assets are worth the net present value of their future income stream. Thus, stock prices’ fundamental values are based on the growth rate of cash flows (“earnings”) and the discount rate at which you discount the cash flows to the present. During 2018, there were four fundamental factors negatively impacting global stock prices:

1. Global central bank policies. This, in my opinion, is the largest fundamental factor contributing to the weakness in global stock markets in 2018 and Q4 in particular. The US Federal Reserve (“Fed”) made statements that they were on auto-pilot to raise short-term interest rates to about 3.5% by the end of 2019. The Fed also said it was on autopilot to reverse its quantitative easing (“QE”) policy via shrinking its balance sheet. Other central banks have also been reducing liquidity. The following charts show the trend in central bank liquidity.

![]()

The market feared that the global economy could not handle such high rates and reductions in liquidity and that a global recession, if not outright depression, would follow. The world simply has too much debt and an increase in interest rates and corresponding decrease in liquidity in such a short time frame is too abrupt for the global economy to handle. In addition, higher interest rates imply lower financial asset values due to higher discount rates. The Fed chairman’s comments on October 3rd that interest rate increases still had a way to go was the trigger for the significant equity market decline in Q4.

2. Global economic slowdown. While the US economy showed strength throughout 2018, the global economy was in steady decline. The global slow-down was in part due to higher US interest rates and a higher US dollar. Emerging markets, which are the global growth engines, were particularly hard hit by the rising US dollar. By Q4, the markets were starting to question whether the US could remain immune to the global economic slowdown. Slower economic activity results in slower earnings growth which implies lower equity values. Global stock markets declined throughout 2018 in part due to the steady declines in economic activity.

3. Trade disputes. Global trade disputes, epitomized by the US-China dispute, risk slowing economic activity which would result in lower corporate sales and thus lower corporate earnings. The rancor between the US and China increased materially in Q4 and contributed to negative sentiment related to future global economic activity.

4. Duration of the current US economic expansion. The current US expansion is coming up on 10 years. Some fear that a recession is inevitable simply because economic cycles have always occurred and its about time for one. A recession reduces economic activity and thus corporate earnings and corresponding equity values.

Technical Factors

1. Algorithmic computer trading programs. Just as computer trading contributed to the large US sell-off in February 2018, computer trading also contributed to the US sell-off in Q4. Algorithmic trading makes up over 50% of all US stock trading. And, many of the programs follow the same rules and thus feed on each other, be it driving markets up or down. In Q4, the trend following programs drove markets down as they fed on the fundamental factors stated above and the technical factors listed below. Also, the computer trading programs have ushered in a new paradigm where trends that in the past took three to nine months to play out now tend to play out over three to nine weeks. This results in greater daily volatility and more violent moves. This makes the market decline in Q4 feel that much worse since it happened so quickly.

2. Hedge fund redemptions and liquidations. Hedge funds continue to fail to generate returns to justify their fee structures. Thus, investors were giving redemption notices in Q4, requiring hedge funds to liquidate positions to satisfy the redemptions. Also, hedge funds continue to shut down, again requiring liquidations. These liquidations are time driven, not price driven. By this I mean, the hedge funds are forced sellers even at any price because they must deliver cash by a certain date. This forced selling contributed to declining stock prices.

3. Tax loss selling. Q4 is the time of year when taxable investors sell their “losers” to offset gains on their “winners”. This tax loss selling added further fuel to the fire of a declining market. If investors take the proceeds from the sales and buy other stocks, the overall market should find support. During Q4 many investors were not re-investing the sale proceeds into new stock positions but instead holding cash or buying bonds.

4. Fear from the financial crisis. Most investors still remember the great financial crisis (“GFC”) and therefore were simply “getting out of the market” for fear of a GFC like 50% plus decline in the market. The wounds of the GFC are still too fresh for many. And if there were a 50% market decline, baby-boomers can’t afford to wait for their portfolios to recover; they need the current value of their portfolios to pay for their retirement.

The good news in 2018 was (i) a strong US economy that appeared immune to the global economic slow-down plus (ii) the benefit of lower US corporate tax rates. But, by Q4, there simply were too many negative factors at play, both fundamental and technical, and US markets succumbed to them.

Looking forward, I think everything described above is noise. In the short-term, they have behavioral influences on markets. But all the technical factors are short-term in nature, lasting weeks or months. And the fundamental factors will ultimately resolve themselves because they are dictated by human decisions. Since humans are wired to better their financial condition, central bankers and politicians will ultimately set policies that contribute to economic growth. It may take a year or two or more, but as we have seen historically, eventually the correct policies for economic growth are set. And, thus, what we experienced in Q4 was just noise if you are a long-term investor (meaning, you care what your investments are worth in 20 to 30 years, not 20 to 30 days, weeks or months).

Finally, stock markets have always experienced pull-backs. Its what they do. Its part of the process. But, buying and holding has proven to be the correct strategy over time. The following chart highlights this concept over the past 10 years.

![]()

Is Past Prologue?

There are two philosophies for investing. In the first, you believe that the factors that have driven the global economy and stock markets for the past 100 years will continue for the next 100 years. You believe that capitalism continues and thus individuals around the world will strive to better their lives. In such, more and more people will work, for which they will derive income, with which they will buy things, which companies will provide, which will lead to growing sales and growing profits. And, if the global economy is growing, then corporate sales and profits, in the aggregate, will grow. This will lead to an increase in global stock markets over time.

This formula has worked for the past nearly 100 years. Yes, from time to time stock markets can have large sell-offs. But, on average, the US stock market increased about 10% annually from 1926 to 2017. That means if you invested $1 in 1926, it would be worth about $7,347 now. That same $1 invested in long-term US government bonds would be worth $143 and invested in one-month US treasury bills would be worth only $21.

Based on the above, you don’t spend your time worrying about whether a recession is coming, about central bank policies, etc. You simply believe in capitalism and believe that in the long-term (say 20 to 30 years), your investment in the stock market will grow at a far greater rate than most any other investment option. And, you have a 92-year track record to support this view. Thus, there is no point in trying to time the market, where you not only have to know when to sell but then also when to buy again. Plus, historically, all the market return in a particular year typically occurs on about 20 trading days. To get the timing right on both when to buy and when to sell is near impossible. Therefore, you are better off just buying and holding, knowing that you will have large declines at times but in the end can expect roughly 10% annual returns if the past is prologue for the future.

Is It Different this Time?

The other philosophy for investing is that you can beat the market by timing when to buy and when to sell. With this lens, there are two legitimate arguments for why it may be different this time: (i) debt and (ii) the rise of populism.

Debt

In a world without debt, the size of the global economy is the size of the population multiplied by the productivity of such people. For the economy to grow, you need some combination of more people and/or higher labor productivity (producing more in a fixed amount of time). Per the following chart, the past 30+ years have benefitted from increasing productivity, but the increases have subsided the past 12 years.

Another way to increase economic growth is via debt. A simple example illustrates this. Without debt, you can only purchase up to your earnings and savings. And, your earnings are a function of your productivity. But your productivity has limits. So, there is a point where you can’t purchase more because you can’t earn more. But if you can borrow money, then you can purchase things with the debt. And, as long as you have enough earnings to pay the interest on the debt, you can grow your purchases each year even if your earnings stay flat. Or at least you can do this until the point where the interest on your debt becomes too large and lenders will no longer provide you more credit. At this point, you can’t borrow more and can’t purchase more. Unless, of course, lenders lower interest rates on your loans. At lower interest rates, your interest payments are the same even at higher debt amounts. And now you can go on growing your purchasing. But even this has limits because interest rates can only go so low.

And, this in a nutshell is the argument being made by some such as Ray Dalio of Bridgewater Associates. They argue that the global economy has benefitted from 70+ years of increasing access to debt enabled by lower and lower interest rates and decreased lending standards. They argue we are now reaching the point where global income (earnings using the example above) can no longer support increased debt because we are close to reaching the limit in how low interest rates can go. And, if debt cannot increase and productivity increases have flattened, then economic growth will slow from historical levels. This then means that investors need to assume a new, lower level of corporate earnings growth and the associated reset in financial asset values that comes with this lower earnings growth rate. The past will not be prologue.

As I wrote in last year’s Octavia’s Outlook, if past is prologue, the US stock market is very inexpensive. If the S&P500 earns $161 per share in 2019 (assumes no earnings growth in 2019 vs 2018), the long-term annual earnings growth rate is 7% (the average the past 100 years), the risk-free treasury rate is 3.5% and the risk premium is 6.5%, then today the S&P 500 should be about 5400 (2x versus about 2700 today). But what if the long-term earnings growth rate is 2% as the global economy resets to a world with less leverage? In that situation, the S&P 500 should be about 2000 (25% lower than today). In this de-leveraging scenario, one could argue the risk premium on equities should be higher. If the risk premium is 9%, the S&P 500 should be 1500 (about half of the current level).

How likely is this scenario? Intellectually I understand it. And, I believe it has been partly at play as it relates to Fed policy over the past year. I think the Fed has a real conundrum. On the one hand, exceptionally low interest rates, as we have experienced the past 10 years, leads to mal-investment. What I mean by this is that projects get approved only because the cost of financing is so low, not because they are genuinely good projects. The result is excess capacity of low-quality products, manufacturers, service providers, etc. which (i) leads to lower long-term productivity and (ii) hurts the well-run companies that must compete with companies or capacity that should not exist. In Darwinian terms, exceptionally low interest rates neuter the benefits of creative destruction. The Fed has been aggressively increasing interest rates the past two years plus shrinking their balance sheet simultaneously in order to slow down this mal-investment and its associated negative impact on long-term economic growth potential.

The problem, though, is that the Fed has gone too fast and the global economy can’t handle the pace of rate increases and simultaneous reduction in liquidity via the shrinking of the Fed’s balance sheet. Its like a drug addict having their heroin taken away. Take it away too fast and the addict convulses violently. That is what happened in Q4. Between what the Fed had already done the past two years and commentary that they would keep going into 2019 and 2020, the global economy went into massive withdrawal. This is the reason during the past month the Fed has completely changed its tune and stated it may not raise interest rates any further. And, the markets have reacted as expected with the S&P 500 increasing about 12.5% from the lows set on Christmas Eve (although the end of tax loss selling and hedge fund redemptions helped also).

Getting back to the specific question of the long-term, secular un-wind of a 70+ year build up in debt, at this time I am not constructing portfolios assuming this will happen. I say this for two reasons. First, a believe that central bankers are ultimately politicians and want to prevent global economic hardship even if that means following the wrong long-term policy. They will keep interest rates low or increase liquidity by growing their balance sheets if that is what is required to maintain the status quo. Low interest rates may create zombie companies who can only survive because they can service the interest on their debt but not actually pay down the debt. But if this is the price to pay for avoiding economic decline, I believe this is what central bankers will do. Basically, I believe central banks will pursue policies that prevent short-term pain at the cost of long-term growth. Better to grow at a lower rate in the long-term but avoid the short-term pain necessary to achieve it.

The second reason I am not constructing portfolios assuming debt will bring down the global economy is that the same argument has been made regarding Japan for the past 20 years. Japan has had near zero interest rates for over 20 years. And while Japan is not growing much, it also is not declining. People have been forecasting the collapse of Japan for over 20 years, but it has not happened. Yes, Japan owes its debt to its own people which is a unique situation. But China is in the same situation. While the US has material external debt, as long as the US dollar is the global reserve currency the US dollar will continue to be strong. So, when I look at historical precedence, the history of Japan calls into question the theory that excessive debt ultimately brings down an economy.

I have the utmost respect for Ray Dalio and am very mindful of what he is saying about debt levels. I’m just not ready at this time to reconstruct portfolios on the assumption that the historical experience of economic growth will fundamentally re-rate as we now enter a period of debt stasis or worse global de-leveraging. I do not believe that central banks and governments will let it happen…for now. Maybe in five or ten years global de-leveraging occurs, but I believe that central banks and governments still have tools to push out its occurrence. This may be bad long-term policy, but I invest based on the way the world is and not the way I wish it was.

The Rise of Populism

Earlier I wrote that an investment in the stock market is a bet on capitalism. But what if capitalism itself is threatened by the rise in populism? Capitalism is the best system to grow the total economic pie. The problem is that everyone’s slice of that pie does not grow equally. Capitalism’s enablement of personal wealth creation married with technologies’ purpose to increase productivity along with free trade’s objective of delivering the best product at the lowest cost creates great wealth for millions of people but simultaneously threatens the livelihood of tens or hundreds of millions of people. And, in a democracy the tens or hundreds of millions whose lives are displaced do not care about the merits of capitalism. They are focused on their personal survival. The result is they may vote for populist politicians who campaign on social justice and fairness, which means higher taxes, more regulation and less free trade. This is a toxic combination for global economic activity and resulting stock market values.

The populist movement is still small, but it is loud and gaining strength globally. As a result, it should not be ignored. And, fact is, it is not being ignored. There are numerous people, including the investor Paul Tudor Jones, who are ringing the alarm bells on this topic. As a result, I believe that the “system” will make the changes necessary such that capitalists can continue to flourish but not at such a rate that too many are negatively impacted. I’m betting on human ingenuity to address the problem. While this may mean the economy grows at rates below potential, it also means that capitalism will survive. And if capitalism survives, that’s good for global stock markets.

Octavia’s Portfolio Allocations

I fully respect the secular risks of debt and a movement away from capitalism. Of the two, I believe debt is the bigger risk and has a higher probability of occurring. But, I’m not ready to fully assume that we are entering the big debt unwind. For clients who are 20 to 30 years away from retirement, I am still fully invested in equities. For clients currently in retirement, portfolios are allocated across equities and bonds depending on their age and personal situation.

As stated earlier, everything that occurred in Q4 is noise and does not impact my long-term thinking on portfolio construction. I am not so arrogant as to think I know when to sell as well as know when to buy back in. I also do not like having to crystalize capital gains taxes on taxable accounts in order to pursue this market timing strategy.

From a fundamental standpoint, the US stock market is inexpensive. Let’s use the following conservative assumptions:

1. 2019 S&P 500 earnings of $160, which assumes no growth versus 2018. Currently, the market is forecasting 2019 earnings to grow 6.5% compared to 2018.

2. Long-term annual earnings growth of 5%. The average over the past 30 years has been 10% and last 100 years has been 7%.

3. Risk-free rate of 4%. The current 10-year treasury yield is 2.75%.

4. Risk premium of 6.5%

Using these assumptions, fair value today for the S&P 500 is 2900, about 10% higher than current levels. Based on this, its just hard not to invest in US stocks if I can tune out the noise and believe in capitalism and human ingenuity.

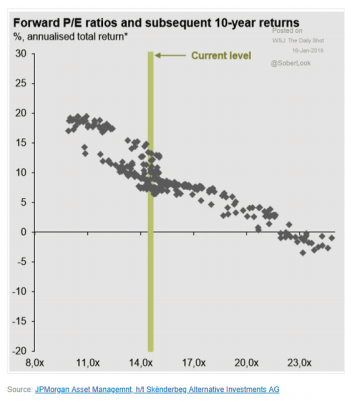

Assuming past is prologue, the following chart shows expected returns ranging from about 7% to about 15% over the next 10 years.

I hope you found this letter of value. My goal is to make good investment decisions, and I welcome any input.

Warmest Regards,

Andre Kovensky

Octavia Investments LLC

Legal Information and Disclosures

This memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Octavia Investments LLC (“Octavia”) has no duty or obligation to update the information contained herein. Further, Octavia makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This memorandum is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Octavia believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Octavia.

This article contains the opinions and ideas of its author and is designed to provide useful general information to the reader on the subject matter covered. No representation or warranty, express or implied, is made or can be given with respect to the accuracy or completeness of the information contained in this article. For a complete disclaimer, please see the last page of this article.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All