Chart of the week: 02/04/2019 – 02/08/2019

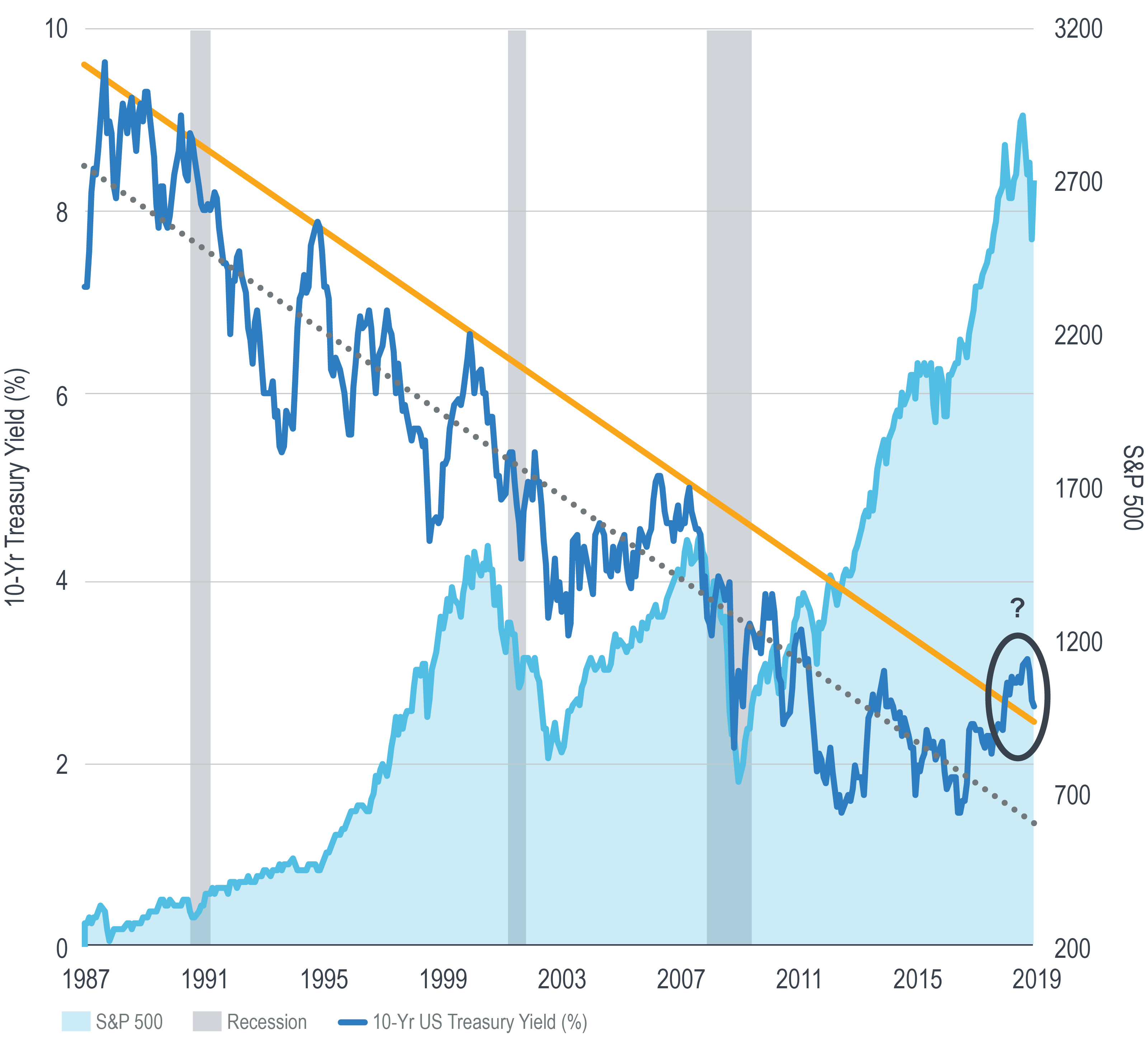

U.S. 10 Year-Treasury Yield Trendline

10-Yr Treasury Yield: Ordained to move upward or destined to move downward?

For the last several decades, the yield on the 10-yr U.S. Treasury bond has been on a downward trend. In spite of the many instances along the way when it appeared that the trend was reversing, the yield eventually changed course and proceeded to reach a new low.

Since touching its all-time low of 1.36% in July 2016, the 10-yr yield has trended higher, rising to 3.24% in November 2018 and breaking through the upper bound (orange line) of its longer-term down trend.

In the past, as depicted in the chart, these inflections have in some instances preceded market declines and recessions.

This most recent breach of the upper bound and the subsequent hint of a reversal raises some interesting questions.

Does the 2.5 year uptrend from its low in 2016 mark the end of the long-term downtrend, or is it merely a blip up on the way to even lower rates?

Is this recent breach of the upper bound signaling a stock market downturn or even a recession?

How might this affect Fed policy?

As the answers to these questions unfold, they will carry significant implications for investor portfolios.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.