Weighing the Week Ahead: Should Investors Worry about the 200-day Moving Average?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe have a normal economic calendar, and 1/3 of S&P 500 companies have not yet reported Q418 earnings. Corporate earnings are not confirming those who thought the market was signaling a recession. Both the economy and earnings remain in the background. Daily market moves, even small ones, and the often-erroneous explanations dominate the financial news. The market story has become the battle of the 200-day moving average.

I consulted Mrs. OldProf about today’s theme. I asked which was most interesting: The Super Bowl offensive show, the State of the Union and commentary, or whether we broke the 200-day moving average? Her response was not helpful.

Since I have a lot of good material this week, I wish I could attract more readers with a great title. I wish I could include Virginia resignations, Jeff Bezos, or scandalous pictures. Instead, I find myself asking:

Should long-term investors trade the 200-day moving average?

This dull-sounding question is actually quite important for the individual investor.

Last Week Recap

In my last edition of WTWA noted the light economic calendar and big earnings week. It was a good opportunity for investors to consider the evidence more deeply, looking beyond the most obvious headline stories. The concept was good enough, but the competing political and sex stories were too attractive. Real financial news took second seat. This may continue in the week ahead, but focused investors can use that as an opportunity.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski. She includes a lot of relevant information in a single picture – worth more than a thousand words. Read the full post for more great charts and background analysis.

Stocks were unchanged on the week and the trading range was only 2.1%. You can see the volatility results and comparisons in our indicator snapshot (below).

Noteworthy

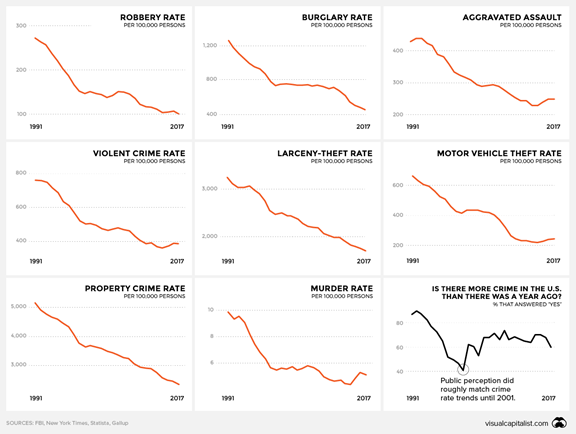

The Visual Capitalist illustrates the same problem we have in the investment world by considering crime statistics. There is a persistent belief that crime is more prevalent, despite FBI data.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

When relevant, I include expectations (E) and the prior reading (P).

New Deal Democrat’s high frequency indicators are an important part of our regular research. This week’s update shows all three time frames in neutral territory. The short indicators are still affected by the government shutdown.

The Good

- Q418 Earnings show continued strength. John Butters (FactSet) reports that the beat rate, revenue beat rate, and size of revenue beat rate are all above those of recent years. The size of the earnings beat rate is in line with the past five years.

- Negotiations to avoid another government shutdown show progress. (NYT) This is moving toward a compromise despite the insistence of extreme and vocal factions in both parties.

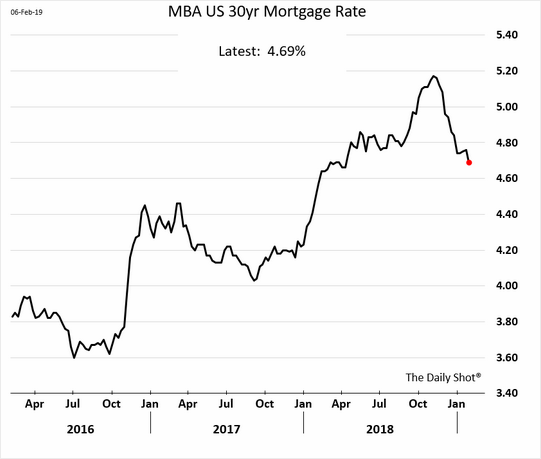

- Mortgage rates move lower. These rates move with the ten-year Treasury note, where yield has also backed off. This is good news for potential home buyers and the housing market.

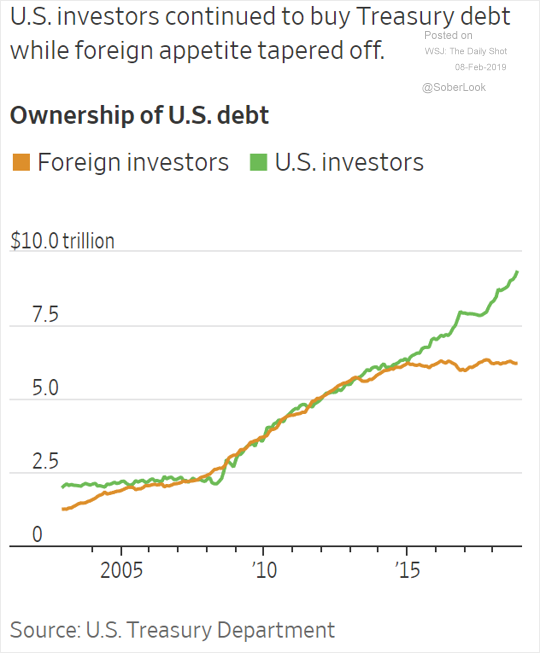

- The market for U.S. debt remains strong, despite smaller foreign purchases. Remember all of the stories about “who will buy our bonds?”

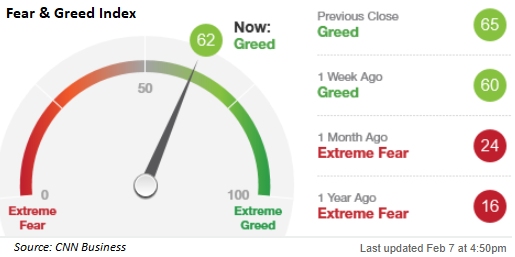

- Investor sentiment, while more bullish, remains at reasonable levels. David Templeton (HORAN) looks at the AAII data, newsletter writers, and the CNN business Fear & Greed index, which he notes hit maximum fear levels in December. Here is a current look.

The Bad

- Factory orders for November declined 0.6%. While this was better than the October decline of 2.1%, it missed forecasts of a 0.3% gain.

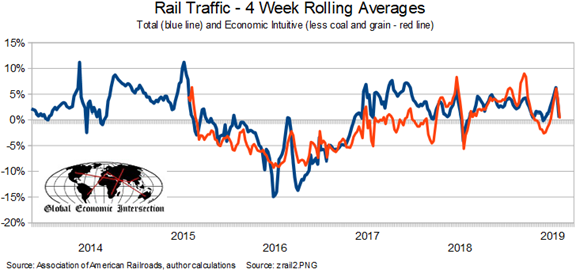

- Rail traffic has weakened. Steven Hansen (GEI) removes some cargo types to get the “economically intuitive” sectors. He also uses rolling averages to reduce noise and a year-over-year approach to avoid seasonal adjustments. His analysis often provides a better view than the “headline” data.

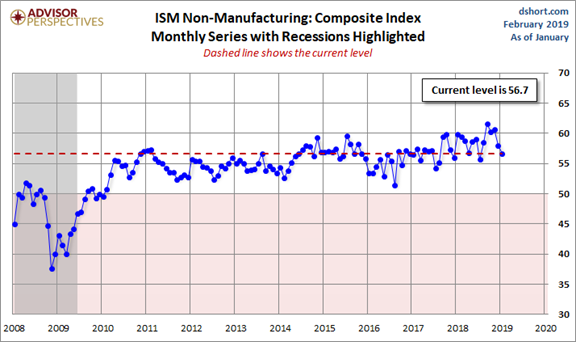

- ISM Non-Manufacturing registered 56.7 for January, lower than the upwardly revised 58.0 as well as expectations of 57.0. The ISM reports that this level corresponds (if annualized) to real GDP growth of 2.8%. Jill Mislinski’s report includes this chart:

- Initial jobless claims decreased to 234K from the prior week’s 253K but missed expectations of 220K. The government shutdown is still showing up in this series, which is based on data (only) one week old.

The Ugly

Farm belt bankruptcies. “Soaring” reports the WSJ. Trade disputes, falling prices, and competition from Russia and Brazil are all cited as factors.

Runner up in this week’s ugly contest goes to investors in a crypto exchange where the CEO died without a record of the sole password. There goes $190 million. (MarketWatch)

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

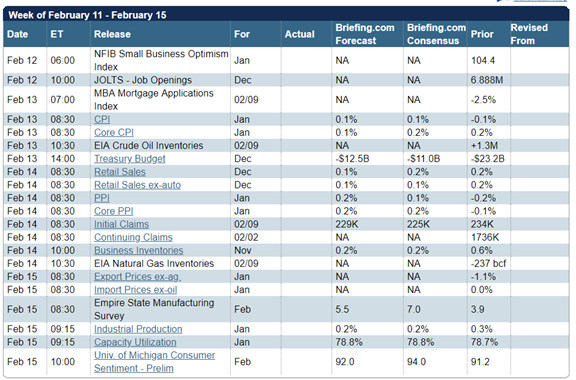

The Calendar

The calendar is normal including some catching up from the shutdown. The feature will be inflation data, both wholesale and retail, although little change is expected. Small business optimism has been important during the Trump Administration, and I’ll be curious about possible effects from the shutdown and the economic weakness meme. The JOLTS report has information about the labor market structure that you do not find elsewhere. It may give some early signals on incipient wage inflation.

And of course, we can also expect plenty of political news with a focus on new hearings and investigations in the Democratically controlled House.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

The stock market has repeatedly faltered at the 200-day moving average in one or more of the major indexes. This has overshadowed all news except salacious gossip. Forget economic data. Who cares? I expect the battle of the technical resistance to remain a major theme in whatever time the pundits have left. It is reasonable to ask:

Should long-term investors change allocations based upon the 200-day moving average?

This indicator is important for traders. Should investors also pay attention? Let’s start with advantages and disadvantages.

Advantages

- When a technical factor becomes important support or resistance, knowing this helps to interpret market action.

- Should investors care about weekly market action?

- Even if the answer is usually “no” a failing (or bouncing) market may provide evidence for the investor’s allocation.

- Limits losses to a pre-defined level. Even savvy investors, tolerant of normal fluctuations, are rightly concerned about the possibility of massive 40-50% declines. Mikhail Samonov (Two Centuries Investments) has a useful analysis of what they see as the two key investment risks: low return and drawdowns. These risks often cause investors and managers to make unwise decisions to switch strategies.

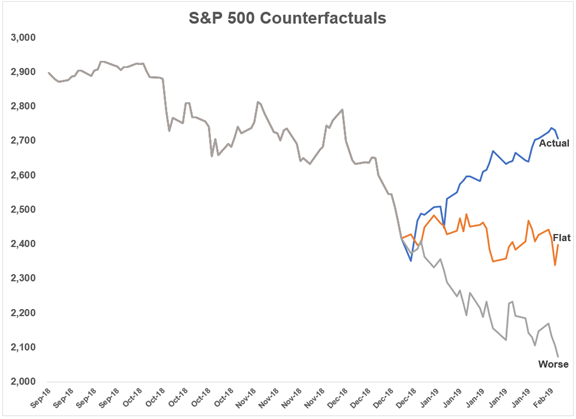

- Takes the emotion out of deciding when to adjust positions. Most investors (and many investment managers) lack the experience to act with discipline during tough times. This effect is often under-estimated. Plenty of people bailed out of their planned investment program in December. Others held on when January restored some confidence. What if the story had been a little different? Ben Carlson explores this topic with two “counterfactuals.” What would have happened in these alternative cases? This is an excellent way to approach the question.

Joe Wiggins (Behavioural Investment) draws upon a great Farnam Street post identifying stupid decisions, those “overlooking or dismissing conspicuously crucial information.” There is a helpful list of concerns, but my favorites are about experts. One point notes how many confident experts there are. Another emphasizes how many are commenting outside their “circle of competence.” Exactly right! Borrowing from Ted Williams, I call this outside of their happy zone.

- Allows the investor to stay in the market during the unavoidable short-term downdrafts. This is the hidden advantage, and perhaps the most important. Investors can usually ignore scary stories and headline news, maintaining or adding to holdings when Mr. Market makes an attractive offer.

Disadvantages

- Does the strategy even work? Josh Brown thinks not. “There’s no signal there, for if there was, everyone would know exactly what to do upon each cross to the upside or downside.” His conclusion?

There is no worthwhile system that will produce satisfactory results from buying above the 200-day and then selling on a cross below, but there is one simple truth about market behavior above and below this imaginary line: Bad things tend to happen more often when the stock market is below. This seems obvious, and it is. When stocks are selling below the levels at which they’ve spent most of a year, people are more nervous and prone to reacting negatively. Volatility, on average, will be elevated when the S&P 500 is spending time below the 200-day, and the major corrections and crashes throughout history have almost all begun from underneath.

- There is potential for whipsaw trading. Markets can move above or below the MA many times before establishing a real trend.

- This generates many trades, all at losses.

- It doesn’t help to set your trade above or below the MA, although it mitigates the “crowded trade” of many who execute the strategy mechanically. You are basically shifting the “whipsaw” point by a small amount.

- It does not help overall performance. Michael Batnick has an interesting analysis of what happens when you can miss the worst days, a frequent topic of bloggers. The problem is that you also miss the best days! Michael has a balanced analysis of possible strategies, although showing a net gain by missing the worst days. Check out the many helpful charts. Here is a key quote about a simple switching model:

This model would have given around 160 signals since 1997- would you have taken all of them? Would you have been able to trust the model and ignore your intuition? Would you have been able to trust the model when it provides 10 signals in 30 sessions? Would you have been able to stick with it when it is dramatically underperforming the index?

- Extra costs

- Increased trading expense.

- Undesired tax consequences.

Allocation importance

Knowing the difference between normal (but large) market fluctuations and the start of a major decline is not easy. Most investors emphasize past performance, trail the major moves, and seriously underperform as a result.

David Templeton (HORAN) shows the most recent “chasing” effect.

These are the basic arguments, strongly held by many participants. Those who embrace buy-and-hold are on one side. Traders and system types, edging into investing, take the other.

As always, I’ll have my own conclusions in today’s Final Thought.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

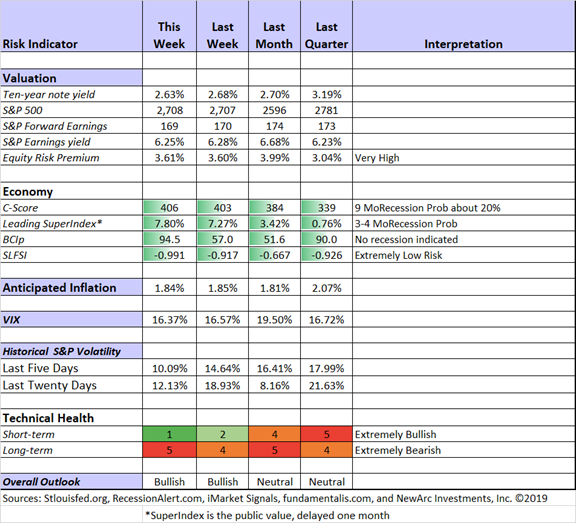

The Indicator Snapshot

Short-term trading conditions have improved to strongly bullish for technically-based methods. This is a good indication for short-term traders. The improvement is enough for our trading models to edge back into the market, but it is not a complete “all clear” signal.

The technical background for long-term trading remains at “slightly bearish.” The reasons behind this are a major theme in today’s post.

Fundamental analysis remains strongly bullish. Earnings are excellent and the risk indicators are low. The overall investment climate has improved to “bullish.”

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Georg Vrba: Business cycle indicator and market timing tools. The BCI does not signal a recession.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Guest Commentary

New Deal Democrat’s valuable high-frequency indicators are featured regularly in WTWA. His long-leading indicators lead him to institute a “recession watch” beginning in Q419. He explains that this puts him on notice to watch for “persistence and confirmation.”

Calculated Risk reviews his own past record on recession forecasting, noting the many big errors by others. He is still not on recession watch.

[Jeff – I confidently forecast…….a bull market in recession forecasting!]

Insight for Traders

Check out our weekly “Stock Exchange”. We combine links to important posts about trading, themes of current interest, and ideas from our trading models. This week our trading models have edged back into the market. Conditions have improved but are not yet at an “all clear” point. Please note that this is not a short-term bullish or bearish call. It reflects what environment provides the best potential for our systems.

With Athena choosing a pot stock, we whimsically wondered Are the Momentum Bulls High?

In addition to our discussion of model choices, we provided background both on momentum and also trends in cannabis. We also provided sector ratings from Oscar and Felix, featuring the DJIA.

Insight for Investors

Investors should embrace volatility. They should join my delight in a well-documented list of worries. As the worries (shutdown, Fed policy, trade) are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

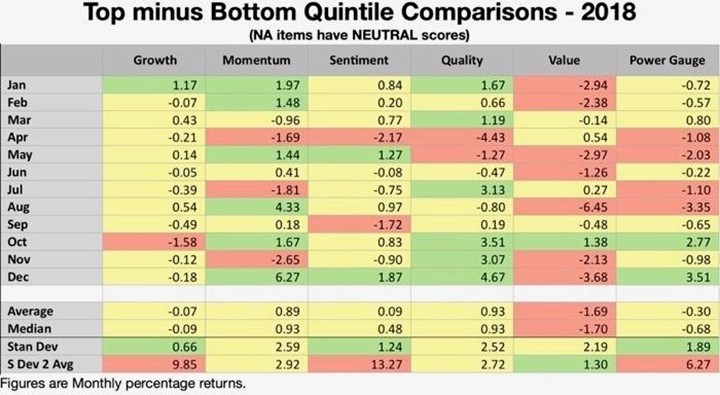

If I had to recommend a single, must-read article for this week, it would be Marc Gerstein’s discussion, Value Pushes Back Against The Bear. He shows the “power gauge” for each of five important factors and provides tables with the monthly results over the last four years. The tables show an unusually long weak period for the value factor, with a sharp switch in January. I’ll show just 2018 as an example, but 2017 is similar.

He writes as interpretation:

Bear in mind, here, that this presentation is about Value as a factor. “Value Investing,” the process of identifying and choosing stocks whose valuation ratios, however high or low they may be, are lower than where they should be in light of company characteristics, was never out of fashion and never will be.

Value as a factor in and of itself is most productive when consensus investor expectations fail to materialize, when highly priced companies don’t fare as expected causing stocks to suffer, and/or when meagerly valued companies prove less bad than previously supposed, causing stocks to correct in a favorable way. The often-empirically-demonstrated long-term efficacy of the value factor tells us that for the most part, investors are not especially good at analyzing companies.

This analysis is important for any investor choosing stocks, ETFs, or managers. In particular, look at Marc’s description of the growth factor and what happens when favorable assumptions return to reality.

Stock Ideas

Chuck Carnevale continues his sector-by-sector bargain hunting with two new installments — Consumer Durables and Consumer Non-Durables. Both posts include detailed analyses and a helpful lesson on valuation. They also mention quite a few of my holdings!

Health care dividend stocks? (Barron’s). The yields are currently lower than utilities and consumer staples, but valuations are better. Seeking Alpha Editor Michael Taylor collects some viewpoints on the risk to pharmaceutical companies.

Will the Celgene (CELG)/Bristol-Myers (BMY) deal be blocked? Stone Fox Capital sees the risk as minor and the possible decline small. Celgene is worth plenty on its own.

Pharmacy benefit manager stocks have been under pressure due to the debate over drug pricing. How much effect will there be under the Trump plan?

However, analysts don’t think the new proposal will impact PBMs too much. “The industry has already been shifting towards a more pass-through, fee-driven model,” UBS analyst Kevin Caliendo said in a note to investors Friday, citing CVS’s disclosure that it only kept 2% of the total rebates it negotiated in 2018. In December, CVS Caremark announced it would be rolling out a new model of pricing where it would pass through 100% of drug rebates to its health plan clients. (MarketWatch).

Eric Compton (Morningstar) opines Wide-Moat Wells Fargo Worth a Look. He discusses the low cost of capital, high revenue per dollar of assets, and low involvement in capital markets. And yes, he also discusses the recent “overheated sales culture.”

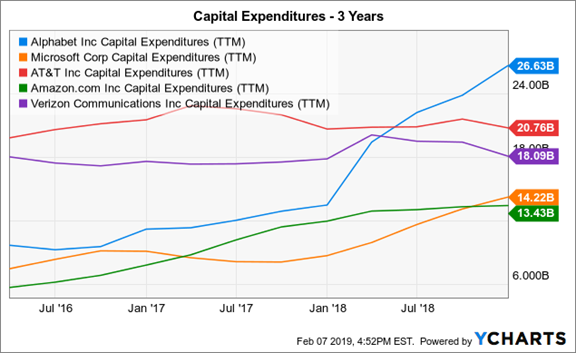

Alphabet’s earnings reports are “confused” by the use of only GAAP numbers, reports Stone Fox Capital. Read the full post for comparisons using more meaningful metrics like revenue growth and increased operating income. Also important is the large increase in capital spending for cloud computing. The authors conclude that the stock remains cheap.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich’s Asset Allocation Daily is consistently both interesting and informative. Each week he highlights stories of interest for both advisors and investors. This week I especially enjoyed his discussion of the “berserk” Mr. Market. He slightly alters the famous Benjamin Graham allegory.

Graham invites readers to view themselves as Mr. Market’s business partner. I would like to alter the analogy and invite you to consider yourself an out-of-town businessperson, preferably an overseas visitor, looking for investment opportunities. My reason is that, in my observation, so many people fail to avail themselves of Mr. Market’s largesse, but rather conduct themselves in sync with him.

Read the full post to see his argument, leading to this great conclusion: By surrounding yourself with good influences, you can begin to build an immunity to the bad cultural influences in the investment world.

Abnormal Returns is an important daily source for all of us following investment news. I read it daily, finding many good ideas. His Wednesday personal finance theme is of special interest for investors. Among the usual collection of excellent choices, I especially liked Emmet Pierce’s Six Reasons to Think Twice Before Taking Out a Reverse Mortgage. Like many financial products, this approach might work for some homeowners. The questions raised in this article are not mentioned by Mr. Selleck and Mr. Winkler.

Watch out for…

Tax refunds. Beware of spending your expected refund before doing your return. Most people expect a lower bill from the tax cut legislation but did not adjust withholding levels (Bloomberg). The result? Smaller refunds for many. [Why do so many people think of taxes in terms of refunds rather than their total tax bill?]

Free dinners – and the annuity pitches that frequently come with them. Eileen Ambrose (Kiplinger) writes as follows about the recent surge in annuity sales:

Part of the reason for the resurgence is that rising interest rates are increasing payouts, making these insurance products more attractive to investors. But much of the credit for the rebound goes to the demise last year of the fiduciary rule—the U.S. Department of Labor rule that would have required brokers and others to put clients’ financial interests ahead of their own when giving retirement-account advice.

She provides excellent advice on how to determine whether this product is right for you.

Final Thought

Investors need some sort of protection against excessive drawdowns. Few are willing to ride through recession-level declines. Trading the 200-day moving average accomplishes many of the risk-control needs of the individual investor. That is a plus.

It is also fraught with costs and problems. I hate “light-switch” decisions, especially those in crowded trades.

I’m more worried about:

- Lack of Brexit progress. The British decision to cancel a shipping contract with a company that has no ships illustrates the many problems that were not considered at the time of the referendum.

- The bull market in researching old yearbooks. What is the dividing line? My high school put on a production of Showboat and I lost out on the chance to sing “Old Man River.” I could not remember the makeup worn by the person chosen for the role, but a yearbook check looks like just a little darkening. How long ago is too long? How dark is too dark? How old must one be before the choices are mature judgments?

I’m less worried about

- Trade issues and the March 1st “deadline.” This was always a flexible target, even though a big worry for many.

- The shutdown negotiations. I expect an agreement. No one will be a clear “winner,” but we’ll move on to more important issues.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits