In early January, a well-known, large US-based asset management firm decided to close its convertible securities fund, citing the fund’s inability to “gain broad acceptance” among some investors and, as part of a review of its products and offerings, “eliminating funds that lack a distinct role.” Following this announcement, the Invesco Convertible Securities Team has fielded several questions about our view of convertible securities. We continue to believe that convertible market remains healthy and that converts may offer investors a way to participate in the upside of the issuer’s stock while providing the potential downside risk mitigation of a fixed income instrument through regular coupons, a stated par value and maturity date.

A convertible security is a corporate bond that has the ability to be converted into a fixed number of shares of common stock. We see the convertible market as healthy when viewed by several measures:

-

US convertibles outperformed a variety of asset classes in 2018, with the ICE BofA Merrill Lynch All US Convertibles Index up 0.2%, compared to a -4.4% return for the S&P 500 Index, -11.0% for the Russell 2000 Index, -2.0% for the Bloomberg Barclays US Corporate High Yield Index and -3.7% for investment grade debt (measured by the Bloomberg Barclays USD Liquid Investment Grade Corporate Total Return Index).1

-

Issuance in the US was strong last year, topping $50 billion in proceeds for the first time in a decade.2That total far exceeded the proceeds raised in 2017 ($37 billion) or 2016 ($36 billion) as rising equity prices and the prospect of higher interest rates pushed companies to raise capital through convertibles, which typically have lower coupons than non-convertible debt from the same issuer.2

-

Flows into the asset class were positive. According to fund flow data from EPFR, cumulative funds into US convertibles outright accounts topped $1 billion in 2018, despite significant volatility in the capital markets during the fourth quarter.

-

Buy/sell activity picked up. Liquidity, as measured by turnover, or the amount of securities traded as a percentage of the amount outstanding, improved in 2018 to 265%, from 232% in 2017.3 Particularly when compared to liquidity in the high yield market (157% in 2018), convert market trading activity has been healthy according to the data from Barclays.

Looking ahead though 2019, the convert market seems well-positioned, in our view.

-

Valuations are more attractive, in our view, as the recent stock market sell-off has resulted in a more balanced profile for converts. Indeed, the average price of a US convertible bond within the Bloomberg Barclays US Convertibles Composite Index declined from the high $110s to approximately $106 in the fourth quarter, while the Russell 2000 Index fell over 20% in the period.4 Additionally, from Sept. 30, 2018, to Dec. 20, 2018, the average current yield of a convertible in this index had risen almost 30 basis points to 2.83%, and the average delta (the amount of sensitivity to stock price moves) had fallen from a relatively high 64% to 54%, which is more in line with the 10-year average of 52%. 4 This means that convert investors can now pick up more yield while still capturing a percentage of equity participation that’s in line with the 10-year historical average.

-

New issuance is expected to remain robust. Bank of America Merrill Lynch is anticipating convertible issuance in the US to come in slightly ahead of 2018’s $52 billion total, based in part on a high volatility equity environment.5

-

Returns are expected to be attractive based on anticipated corporate earnings growth moving stocks higher and higher convertible coupons. Barclays is predicting gains for convertibles and equities in 2019.

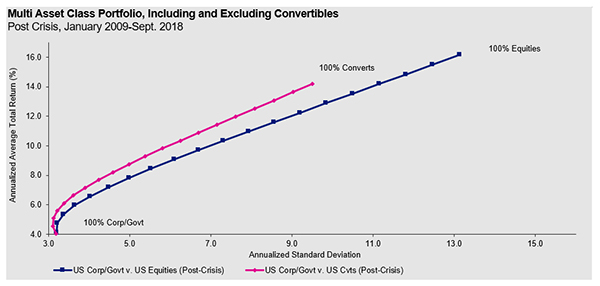

Moreover, as shown below, the addition of convertibles to a portfolio of all stocks or all bonds can enhance returns for a given amount of risk or lessen risk for a given return.

Improved risk-return profile

Including convertibles in a bond portfolio can potentially provide more return for the same amount of risk, when compared to a stock and bond portfolio. In the hypothetical chart below, the points along the pink line represent a bond/convert portfolio allocated in 5% increments (from left to right, 100%bond/0% convert, 95% bond/5% convert, 90% bond/10% convert – with 0% bond/100% convert on the far right) The points along the blue line represent the same allocations for a bond/equity portfolio. As shown below, the bond/convert portfolios trend higher on the return axis and lower on the standard deviation (risk) line than the bond/equity portfolios.

Source: BofA Merrill Lynch, as of Sept. 30, 2018. Past performance cannot guarantee future results. Risk is measured by standard deviation. Standard deviation measures a fund’s range of total returns and identifies the spread of a fund’s short-term fluctuations. Stocks are represented by the S&P 500 Index. Bonds are represented by the BofA Merrill Lynch U.S. Corporate/Government Master Index. Convertibles are represented by the ICE BofA Merrill Lynch All US Convertible Index. An investment cannot be made directly in an index. This hypothetical example is for illustration purposes only. This does not constitute a recommendation of the suitability of any investment strategy for a particular investor.

Conclusion: Convertible securities may help with diversification

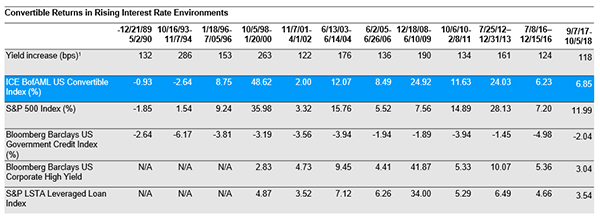

To sum up, the Invesco Convertible Securities team continues to view convertible securities as a worthwhile diversification tool, offering investors the potential for equity upside participation as well as downside support from the fixed income component. Converts’ less than perfect correlation with both stocks and bonds6 means that adding them to an equity or bond portfolio can potentially reduce the portfolio’s risk per unit of return. And converts’ historical outperformance in a rising rate environment7 may be beneficial if rates do rise this year. A robust new issuance calendar may provide managers the opportunity to invest in compelling growth situations and hopefully generate attractive risk-adjusted returns.

Learn more about Invesco Convertible Securities Fund.

1 Sources: Lipper and Bloomberg, L.P., as of Dec. 31, 2018

2 Source: Bank of America Merrill Lynch, as of Dec. 31, 2018

3 Source: Barclays, “US Convertibles Outlook 2019: In the Wheelhouse,” Dec. 13, 2018

4 Source: Barclays, as of December 2018

5 Source: Bank of America Merrill Lynch, “2019 – the year ahead: Convertibles positioned to perform as risks rise,” Nov. 20, 2018

6 Source: Bank of America Merrill Lynch. As of Dec. 31, 2018, the 10-year correlation between the ICE BofA Merrill Lynch US convertibles Index and the S&P 500 Index was 0.91. Between the ICE BofAML US Convertible Index and the ICE BofA Merrill Lynch US Corporate Index was -0.03.

7 See chart below

Sources: Invesco, Bloomberg L.P. Basis point is the smallest measure used for quoting yields on bonds and notes. One basis point is one one-hundredth of a percentage point, or 0.01%. If the US Federal Reserve increases its short-term interest rate target by 50 basis points, or a bond’s yield rises by 50 basis points, the change would be 0.50% or one-half of one percent. The S&P 500® Index is generally representative of the US stock market. The Barclays US Government Credit Index includes Treasuries and agencies that represent the government portion of the index, and it includes publicly issued US corporate and foreign debentures and secured notes that meet specified maturity, liquidity and quality requirements to represent the credit interests. The ICE BofAML US Convertible Index is an unmanaged index that measures performance of US dollar-denominated convertible securities not currently in bankruptcy with a total market value greater than $50 million at issuance. The S&P LSTA Leveraged Loan Index is designed to reflect the performance of the largest facilities in the leveraged loan market.Yield increases represented by the 10-year Treasury yield. Past performance cannot guarantee future results. Returns less than one year are cumulative; all other performance figures are annualized. Does not reflect or imply the performance of any Invesco Fund. An investment cannot be made directly in an index.

Important information

Blog header image: FreelySky/Shutterstock.com

The ICE BofA Merrill Lynch All US Convertibles Index is an unmanaged index that measures performance of US dollar-denominated convertible securities not currently in bankruptcy with a total market value greater than $50 million at issuance.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The Russell 2000® Index, a trademark/service mark of the Frank Russell Co.®, is an unmanaged index considered representative of small-cap stocks.

The Bloomberg Barclays US Corporate High Yield Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or bel

The Bloomberg Barclays USD Liquid Investment Grade Corporate Total Return Index is designed to track a more liquid subset of the US Corporate Index, which measures the market for investment grade, fixed-rate, taxable corporate bonds.

BofA Merrill Lynch U.S. Corporate/Government Master Index tracks the performance of US dollar-denominated, investment grade-rated corporate debt publicly issued in the US domestic market.

The Bloomberg Barclays US Convertibles Composite Index tracks the performance of the USD-denominated convertibles market and includes all four major classes of convertible securities (i.e., cash pay bonds, zeros/OIDs, preferreds, and mandatories).

The ICE BofA Merrill Lynch US Corporate Index tracks the performance of US dollar-denominated, investment-grade-rated corporate debt publicly issued in the US domestic market.

Invesco Convertible Securities Fund Risks:

Convertible securities may be affected by market interest rates, the risk of issuer default, the value of the underlying stock or the issuer’s right to buy back the convertible securities.

An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Derivatives may be more volatile and less liquid than traditional investments and are subject to market, interest rate, credit, leverage, counterparty and management risks. An investment in a derivative could lose more than the cash amount invested.

The risks of investing in securities of foreign issuers, including emerging markets, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Junk bonds involve a greater risk of default or price changes due to changes in the issuer’s credit quality. The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.

Preferred securities may include provisions that permit the issuer to defer or omit distributions for a certain period of time, and reporting the distribution for tax purposes may be required, even though the income may not have been received. Further, preferred securities may lose substantial value due to the omission or deferment of dividend payments.

The Fund is subject to certain other risks. Please see the current prospectus for more information regarding the risks associated with an investment in the Fund.

Stuart Novick, CFA

Senior Analyst

Stuart Novick is a Senior Analyst working with the Invesco Convertible Securities team.

Mr. Novick joined Invesco in 2014 and entered the industry in 1989. He was previously a senior credit analyst at Bloomberg, covering special situations in the Bloomberg Industries research group. Prior to that, he was a credit analyst at the Financial Times Group. Mr. Novick started in the industry in 1989 and spent 17 years at Citigroup, where he was a director in the convertible securities group.

Mr. Novick earned a BS degree from the University of Albany and an MBA from Columbia Business School. He holds the CFA designation.

Read more commentaries by Invesco

Sources: Invesco, Bloomberg L.P. Basis point is the smallest measure used for quoting yields on bonds and notes. One basis point is one one-hundredth of a percentage point, or 0.01%. If the US Federal Reserve increases its short-term interest rate target by 50 basis points, or a bond’s yield rises by 50 basis points, the change would be 0.50% or one-half of one percent. The S&P 500® Index is generally representative of the US stock market. The Barclays US Government Credit Index includes Treasuries and agencies that represent the government portion of the index, and it includes publicly issued US corporate and foreign debentures and secured notes that meet specified maturity, liquidity and quality requirements to represent the credit interests. The ICE BofAML US Convertible Index is an unmanaged index that measures performance of US dollar-denominated convertible securities not currently in bankruptcy with a total market value greater than $50 million at issuance. The S&P LSTA Leveraged Loan Index is designed to reflect the performance of the largest facilities in the leveraged loan market.Yield increases represented by the 10-year Treasury yield. Past performance cannot guarantee future results. Returns less than one year are cumulative; all other performance figures are annualized. Does not reflect or imply the performance of any Invesco Fund. An investment cannot be made directly in an index.

Sources: Invesco, Bloomberg L.P. Basis point is the smallest measure used for quoting yields on bonds and notes. One basis point is one one-hundredth of a percentage point, or 0.01%. If the US Federal Reserve increases its short-term interest rate target by 50 basis points, or a bond’s yield rises by 50 basis points, the change would be 0.50% or one-half of one percent. The S&P 500® Index is generally representative of the US stock market. The Barclays US Government Credit Index includes Treasuries and agencies that represent the government portion of the index, and it includes publicly issued US corporate and foreign debentures and secured notes that meet specified maturity, liquidity and quality requirements to represent the credit interests. The ICE BofAML US Convertible Index is an unmanaged index that measures performance of US dollar-denominated convertible securities not currently in bankruptcy with a total market value greater than $50 million at issuance. The S&P LSTA Leveraged Loan Index is designed to reflect the performance of the largest facilities in the leveraged loan market.Yield increases represented by the 10-year Treasury yield. Past performance cannot guarantee future results. Returns less than one year are cumulative; all other performance figures are annualized. Does not reflect or imply the performance of any Invesco Fund. An investment cannot be made directly in an index.