What the Size of Your Coffee Cup Can Teach Us About Investment Returns

Many US companies have enjoyed an earnings boost from premium products in recent years. But a strong sales mix may leave a company’s profitability vulnerable in the late stages of an economic cycle, when spending trends begin to weaken.

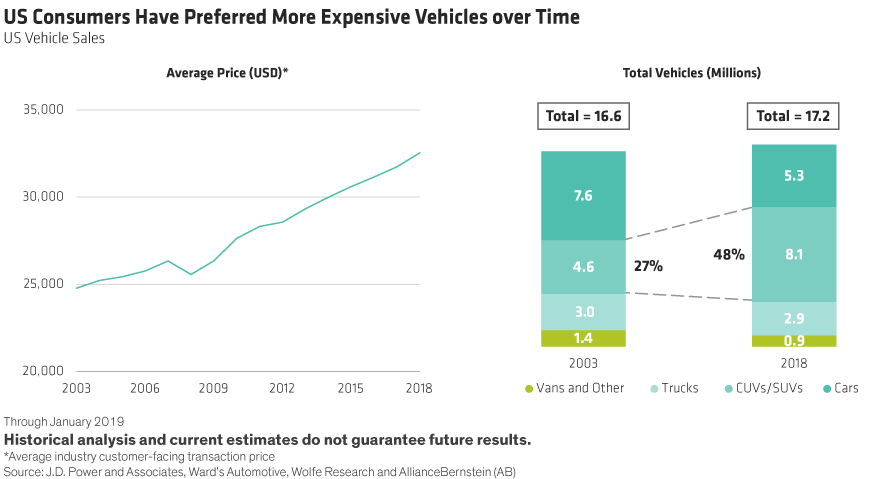

Buoyant consumer demand has fueled the US economy over the past decade. During good economic times, consumers are more capable of embracing premiumization and tend to trade up from good products to better or best products. Investors often don’t pay much attention to this process, but it can make a big difference to a company’s sales mix, profitability and financial performance.

A stronger sales mix—or a greater share of higher-end and higher-priced products—feels great for companies. It typically boosts sales and profits, with limited incremental investment. So profit margins and return on invested capital (ROIC), a key profitability measure, tend to be higher when the mix is rich.

Mix It Up: Large Coffees Unlock Profitability

Coffee sales are a great example of how premiumization can dramatically affect a company’s bottom line. Go to any coffee chain, and you’ll find that a medium-sized coffee costs a bit more than a small cup. But for the company, there’s little added expense, and probably no incremental capital investment, to deliver it. Selling more medium coffees is a winning strategy.

Adding large coffees to the mix is even better. As the analysis in the illustrative example below shows (Display), a large coffee is more than twice as profitable as a small cup. And shifting just 10% of sales to large cups would push the ROIC to 18.2%. That’s a 20% improvement in profitability from selling only small cups. So when coffee consumers regularly upgrade to larger cups, they trigger a change in the sales mix that’s arguably as powerful to the company’s financial results as pure price increases. These financial dynamics occur across industries.

Investors can’t usually see the sales mix effect. Few companies provide enough detail on how sales are generated to evaluate the mix. For instance, even when Apple reported smartphone unit volumes in the past, it did not disclose sales volumes by phone model. With good (or bad) mix trends potentially lasting for years, both investors and companies may lose perspective on what a normal sales mix is. It’s also difficult to disaggregate productivity gains (which theoretically are structural) from mix improvements (which can have limited life-spans).

Since the Great Recession, the sales mix of many companies has benefited from monetary policy, in our view. Central banks’ low interest rates have driven a consumer-lending boom. This has enabled consumers to buy products and services that they might not be able to afford without financing. As a result, we think excessive monetary liquidity has likely inflated demand volumes across many industries. This possibility implies that if conditions normalize the risk to many companies’ financial performance is greater than many realize.