GMO Quarterly Letter

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAnd the Winner Was…T-Bills?

A down year makes for much-improved opportunities

Ben Inker

Executive Summary

2018 was a lousy year for almost all assets, with no major asset class around the world able to keep pace with U.S. Treasury Bills. The poor returns were not driven by any economic calamity, but by markets coming into the year with unrealistic and incompatible expectations, which wound up being generally disappointed. The poor returns have a silver lining, however, in that today a number of asset classes are priced at levels that embody much more achievable expectations and decent longterm returns. In general, it looks to be the best opportunity set we have seen since 2009. This means it is reasonably straightforward to put together a diversified portfolio priced to achieve something close to +5% real return. But as U.S. equities and nominal government bonds are not among the appealing assets, we believe the portfolio you should own today looks more or less nothing like a traditional 60% stock/40% bond portfolio.

Your portfolio likely lost money last year. It wasn’t in a catastrophic, 2008 kind of way, but I am reasonably confident in saying that for U.S. dollar based investors reading this, 2018 ended up with a negative sign before your total return. The strong U.S. dollar meant that non-U.S. investors owning unhedged foreign assets did a little better than their U.S. counterparts, but only in places like Australia and Canada, where local currencies were very weak, would many investors have had a shot at achieving positive total returns. Of the asset classes that traditionally have meaningful allocations in institutional portfolios, only the Bloomberg Barclays U.S. Aggregate Bond Index (Agg), a proxy for investment grade bonds, gave a positive return in U.S. dollars – and it earned a princely +0.01%. Otherwise, pretty much everything was down. The S&P 500 fell 4.4%, soundly trouncing both MSCI EAFE (down 13.8%) and MSCI Emerging (down 14.6%). Real estate proved no hedge, with REITs falling 4.6%, and small caps were even worse than large caps, with the Russell 2000 down 11% and MSCI EAFE Small Cap down 17.9%. Credit was no haven either, with the Bloomberg Barclays U.S. Corporate High Yield down 2.1% and the J.P. Morgan EMBI Global emerging debt index down 4.6%. The best performing major asset worldwide was stodgy old U.S. Treasury Bills, up 1.9%. It was the first time since 1994 that T-Bills beat both the S&P 500 and the Agg, and the first time since 1981 that they outperformed those assets along with non-U.S. equities, small caps, and REITs. It is worth pointing out that in 1981, T-Bills returned over 15%, so an index could trail it and still deliver a double-digit return. As a result, 2018 arguably set a new standard for universal dismalness.

For all that, a 60% stock/40% bond portfolio1 lost only 5.5% for the year, a far cry from the 26% loss such a portfolio suffered in 2008. In reality, it was merely the fifth worst year in the past 30, hardly an outlier in a total return sense. What feels so odd about 2018 was the sheer unavoidability of the losses. In 2008 you could at least daydream about having had the foresight to move your portfolio to government bonds and reap a +12.4% return. There was no such haven asset in 2018.2 Had you had perfect foresight about asset class returns for the year, the best your long-only portfolio could have achieved was +1.86%, earned by investing your entire portfolio in 3 month Treasury Bills.

The other interesting feature of the year was the fact that the broad swath of losses across asset classes was not driven by any particularly horrible economic events. According to the IMF World Economic Outlook report, real GDP growth for the 12 months ended June 2018 (the most recent data I could find) was +3.2% U.S. dollar weighted and +3.7% purchasing power parity weighted. These were the best growth rates since 2010 and 2011, respectively. World inflation, while up 0.6% from 2017 at +3.8%, was below the average level since 2000. And yet, more or less every asset capable of delivering a capital loss did so.

So, what gives? It comes down to expectations. The simple answer is that markets came into 2018 with an unrealistic set of expectations, and more or less all of them were disappointed. Bond markets assumed inflation and growth would be so muted as to dissuade the Federal Reserve from raising rates four times, as it had suggested was its plan. Stock markets assumed growth would be strong, and appear durable, driving earnings and the expectations for future earnings high enough to keep stocks competitive with the higher yields available on cash. Credit markets assumed that growth and inflation would be muted enough to keep rates low, but corporate cash flow high enough to keep default rates at cycle lows. Real estate assumed that growth would be strong enough to stimulate demand, but rates low enough to keep financing costs from rising. As it turned out, growth was too strong for the bond market’s liking, and too weak for the other asset classes. It is a clear reminder of the truth that it doesn’t take a disaster to lead markets to losses, only a disappointment. Disasters certainly aren’t very good for portfolios, but investing is far more complicated than simply avoiding risk coming into a recession.

Exhibit 1 shows the annualized performance of the S&P 500 in real terms in recessions and expansions since 1900.

Returns were certainly a bit better on average during expansions than recessions – +8.6% real versus +6.7% real. But it is abundantly clear that any narrative that says “stocks do well in expansions and poorly in recessions” is silly. Markets tend to do badly when disappointed and well when positively surprised. The onset of a recession usually comes as a disappointment. If you can predict that disappointment, you will indeed avoid some pain. But predicting a recession, as hard as it is, is not enough. You need to predict that things will be worse than the market expects. If you believe there will be a recession and the market agrees with you, there is no sense in selling your equities. Similarly, once the recession starts, its end will probably come as a positive surprise. If you wait until it is easy to see the recession is over, you may well miss out on a significant market recovery.

How Do You Predict a Surprise?

But if markets respond to surprises and surprises are difficult to predict, does that mean we have to just give up on being able to forecast anything? I’d suggest not. Rather than giving up, I think it makes sense to focus on situations where the odds of a positive surprise are better than average. When are the odds of a positive surprise better than average? When expectations are really low. Low expectations do not guarantee a good outcome, but they do allow for decent outcomes in the absence of what most investors would consider to be “good news.” To illustrate, let me ask you which country in the world actually had a positive stock market return in U.S. dollars last year?3 Let’s think a little about what type of country it might be. The best performing sectors in 2018 were utilities and health care and the worst were materials, financials, industrials, and energy. So perhaps we’d want to think of countries heavy in more defensive sectors and lighter in cyclicals and financials. From a regional perspective, emerging markets underperformed developed markets, so we’d probably want to look at the developed world. The obvious candidates would be countries like the U.S. and possibly Switzerland. Both did outperform the average country in the year, with returns of -4.4% and -8.2%, respectively. But the winner for the year was Russia, with a return of +0.2%, despite a stock market consisting almost entirely of energy, materials, and financials; an ongoing war with one of its neighbors; significant economic sanctions; and real GDP growth of a paltry +1.4%. The best thing one could say about Russia in 2018 was that things could have been worse, and with some of the cheapest valuations in the MSCI All Country World Index (ACWI) coming into 2018, it was priced for some pretty nasty events. The second best performer was Brazil, with a loss of only 0.2%. Again, we can’t exactly claim this was a banner year for the country, with economic growth of +1.3% real, a marked absence of needed economic and political reforms, and the election of a right-wing populist lacking any particularly obvious qualifications for governing and espousing more killings by the police. But things could certainly have been worse, and slow GDP growth is certainly better than falling back into the depression that had seen the biggest fall in Brazil real GDP going back at least as far as the 1950s.

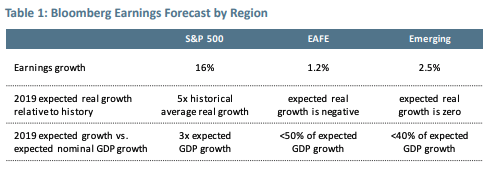

So, what are investors expecting in 2019? The good news is that expectations are not as ebullient as last year, but things differ materially across regions. Forecast earnings growth for the S&P 500 is 16%,4 which is admittedly down from over 25% a year ago. This is a little misleading, however, as much of last year’s forecast and actual earnings growth came directly from the corporate tax cut, and there is no similar windfall in the cards for next year. Growth of 16% is extremely strong by the standards of anything other than 2018, implying real growth of over 5 times the long-term history for the S&P 500. So analysts are certainly still quite optimistic about the prospects for U.S. corporations. Analysts in the rest of the world are positively gloomy, however, with growth estimates for MSCI Emerging and EAFE at 2.5% and 1.2% – approximately 0% and -1% growth after expected inflation!

Now it is certainly possible that the U.S. continues to strongly outpace the rest of the world from a profitability perspective, but it is worth remembering that U.S. corporate profits are already just about at all-time highs relative to GDP (see Exhibit 2), and GDP growth is unlikely to be particularly strong.

Achieving forecast growth for the S&P 500 implies corporate profits moving decisively above any previous peak relative to GDP. This is possible, but why stick your neck out investing in the one region of the world where meeting expectations requires something never seen before?

EAFE and emerging could come in with even worse growth than that forecast, but those forecasts assume earnings growth significantly below expected GDP growth,5 whereas U.S. forecasts assume growth of over three times GDP growth.6 An additional potential concern in the U.S. is the fact that while the equity market is expecting continued strong growth, the bond market is now expecting the Federal Reserve to cut rates in 2019, against the “Fed dots,” which suggest 0.5% of tightening over the year. It seems highly likely that either stock investors or bond investors are going to wind up disappointed. Growth strong enough to make the stock market happy is very likely to push the Fed to disappoint bond investors and raise rates. An economy weak enough to cause the Fed to lower rates in the face of currently very low unemployment seems extremely unlikely to show earnings growth of anything close to 16%. It actually seems quite possible that we could see a repeat of 2018 for the U.S. at least, with both stock investors and bond investors disappointed with the outcome.

None of this is close to a guarantee, of course. Maybe the U.S. will have a burst of disinflationary growth that allows profits to flourish while falling inflation pushes the Fed to ease. Maybe the rest of the world will do even worse than the tepid growth that analysts expect. But as a rule, investing where success requires something never seen before seems a lot harder than investing where business as usual would count as a significant positive surprise.

Putting Together a Portfolio

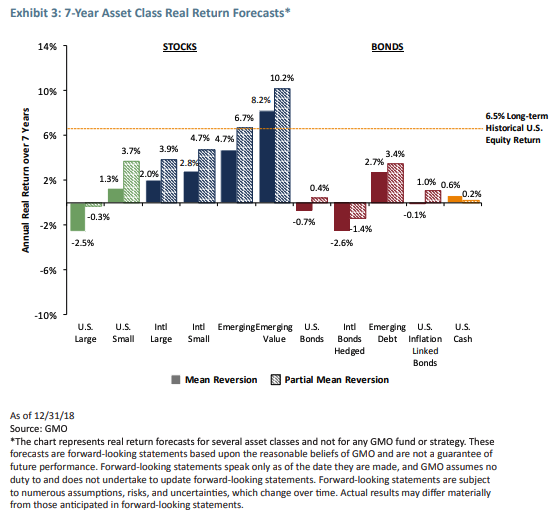

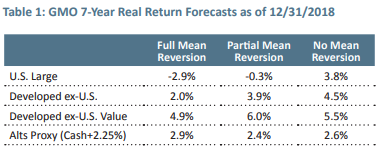

Our asset allocation process doesn’t directly focus on analysts’ expectations. As analysts have historically done a lousy job of forecasting, we generally ignore their forecasts and instead assume that things will gradually wend their way to normalcy. It should not come as a surprise, however, that our forecasts line up quite similarly to the “inverse of expectations” ordering. Our December forecasts (Exhibit 3) show both the partial mean reversion and full mean reversion scenarios.

While the U.S. looks better on our data than it has in a while, it still has a forecast meaningfully below cash in either scenario. But non-U.S. developed equities are a good deal better than cash, and emerging equities even better, at about fair value versus history. We believe combining those reasonable valuations with value spreads much wider than average means there is suddenly a fairly wide array of cheap stocks to buy. The attractiveness of credit is also on the rise, with emerging debt looking a bit cheap on our data and U.S. corporate high yield at approximately fair value as of yearend.7 Even cash itself has a higher yield than any time since January 2008. It is the first time since 2009 that we have seen such a wide swath of assets this attractively priced.

Not only do several traditional assets look appealing, we also have a number of liquid alternatives (see John Thorndike’s accompanying piece) joining the ranks of pretty attractive assets. Based on our current forecasts for the asset classes represented in our Benchmark-Free Allocation Strategy, we have a forecasted real return of +4.2% before alpha.8 For the classic 60% stock/40% bond9 portfolio, unfortunately, things do not look as rosy, as neither U.S. equities – now well above 50% of a global equity index – nor government bonds look priced to deliver returns meaningfully in excess of inflation. The classic 60/40 portfolio is therefore priced to deliver a paltry +0.7% real due to its large weight in those two areas. To me this is a bit reminiscent of the world at the end of 2000, where despite meaningful losses for the year, the S&P 500 was still substantially overvalued, but other asset classes, having fallen along with the S&P, were rapidly getting cheap. 2001 and 2002 were negative years for traditional portfolios, but there was money to be made for investors who focused on areas where prices were attractive.10 Will 2019 be the year that the 60% stock/40% bond portfolio finally shows its weaknesses? It’s hard to say, but it is certainly pretty easy today to come up with a portfolio where good returns require a much less impressive economic balancing act.

Ben Inker. Mr. Inker is head of GMO’s Asset Allocation team and a member of the GMO Board of Directors. He joined GMO in 1992 following the completion of his B.A. in Economics from Yale University. In his years at GMO, Mr. Inker has served as an analyst for the Quantitative Equity and Asset Allocation teams, as a portfolio manager of several equity and asset allocation portfolios, as co-head of International Quantitative Equities, and as CIO of Quantitative Developed Equities. He is a CFA charterholder.

Performance data quoted represents past performance and is not predictive of future performance. Returns are presented after the deduction of a model advisory fee and a model incentive fee if applicable. Net returns include transaction costs, commissions and withholding taxes on foreign income and capital gains and include the reinvestment of dividends and other income, as applicable. A GIPS compliant presentation of composite performance has preceded this presentation in the past 12 months or accompanies this presentation, and is also available at www.gmo.com. Actual fees are disclosed in Part 2 of GMO’s Form ADV and are also available in each strategy’s compliant presentation. Fees paid by accounts within the composite may be higher or lower than the model fees used. The performance information is supplemental to the GIPS compliant presentation that was made available on GMO’s website in September of 2018.

Disclaimer: The views expressed are the views of Ben Inker through the period ending January 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2019 by GMO LLC. All rights reserved.

1 60% MSCI All Country World Index/40% Bloomberg Barclays U.S. Aggregate Bond Index.

2 I don’t have good data on the returns to private credit for the year, and it is possible that when such indices come out they will show a meaningfully positive return. If so, it will be due to the fact that the loans will not have been marked to market, as they somehow seldom are in that asset class. While that apparent stability may help explain the appeal of the asset class in recent years, equities delivered positive returns in 2018 as well, if you’ll allow me not to update prices from the levels at which they were purchased.

3 Actually there were three countries in the MSCI All Country World Index universe that had gains last year, but two of them, Peru and Qatar, are such a small weight in the global equity universe as to be irrelevant.

4 All growth estimates are from Bloomberg positive estimated EPS relative to positive trailing EPS, for S&P 500, MSCI EAFE, and MSCI Emerging indices.

5 The IMF World Economic Outlook estimates 2019 real GDP growth at 2.1% for advanced economies and 4.7% for emerging economies.

6 The Survey of Professional Forecasters forecast 5% nominal U.S. GDP growth in 2019 in their Q4 2018 release. https:// www.philadelphiafed.org/research-and-data/real-time-center/survey-of-professional-forecasters.

7 This is true on year-end data. The rally in the first part of January has pushed high yield back above fair value, although emerging debt still looks fair.

8 These forecasts use a blend of our full and partial mean reversion scenarios along with adjustments for the expected return to currencies based on their respective valuations. For alternative strategies, we are assuming there is a return to the basic activities involved as discussed in John Thorndike’s accompanying piece.

9 60% MSCI ACWI/40% Bloomberg Barclays U.S. Aggregate.

10 A 60% MSCI ACWI/40% Bloomberg Barclays U.S. Aggregate portfolio lost 6.6% in 2001 and 8% in 2002, whereas GMO’s Global Asset Allocation Composite made +3.9% and +0.9%. Our Benchmark-Free Allocation Composite launched during 2001 (with a +2.6% return from 7/31/2001 to 12/31/2001) and returned +6.5% in 2002. Past performance is no guarantee of future results. Please visit www.gmo.com for a complete performance history of each composite.

Liquid Alts: Rising to the Occasion

How liquid alternatives, aided by higher cash rates, can help position portfolios to achieve 5% real returns

John Thorndike

Executive Summary

■ In the years following the Global Financial Crisis, liquid alternative investment strategies1 have failed to match their pre-crisis performance.

■ Post-crisis returns have been dragged down by negative real (i.e., after inflation) cash yields, but this drag has likely been eliminated thanks to recent interest rate hikes by the Federal Reserve.

■ Buoyed by short-term rates above expected rates of inflation, liquid alts now look poised to deliver attractive real returns and outperform developed equity markets in the coming years.

■ Investors who redeem from alts today are exhibiting the classic investor behavior of selling out as the opportunity set improves.

■ Considering the risks and perceived opportunities of GMO’s alternatives strategies, we believe the alts in our asset allocation portfolios have the potential to deliver 5% real returns.

■ The improved prospects for alts and the attractive prices of emerging market value stocks indicate that our portfolios may be well positioned to outperform traditional balanced portfolios.

■ While the 5% real return target sought by many institutional investors will likely remain a challenging bogey for diversified portfolios in the coming years, we are increasingly optimistic about our portfolios’ prospects for delivering 5% real.

Liquid Alts since the Global Financial Crisis

Liquid alts have disappointed many investors who bought into these strategies in the aftermath of the Global Financial Crisis (GFC). The term “liquid alts” covers a broad spectrum of investment programs2 that can colloquially be described as hedge fund strategies in mutual fund form. While no two liquid alts funds look exactly alike, the strategies generally exhibit low sensitivity to traditional asset class movements, take both long and short positions in securities, and turn over their portfolios relatively frequently. Unlike hedge funds that may employ lockups, restrict redemption activity, and provide only limited transparency into portfolio positions, liquid alts provide daily liquidity to investors and position-level transparency through public filings. In other words, liquid alts had much to offer in the post-GFC environment.

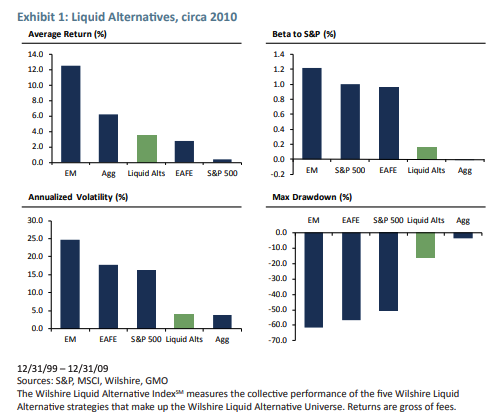

Not only did liquid alts have some attractive characteristics, they had also performed well through the GFC.3 In the 10 years ended 2009, liquid alts outperformed developed equity market indices, exhibited about as much volatility as bonds, and limited losses during equity market drawdowns. From 2000 to 2009:

■ Liquid alts delivered average annual returns of +3.5%, outpacing the +2.8% average return of the MSCI EAFE Index and the +0.4% average annual return of the S&P 500.

■ The 4.1% annualized standard deviation of monthly returns for liquid alts modestly exceeded the 3.8% volatility of the Bloomberg Barclays U.S. Aggregate Bond Index.

■ Liquid alts experienced a 16.4% drawdown compared to losses of greater than 50% for broad equity market indices.

Not surprisingly, capital gravitated toward liquid alts funds. According to the Financial Times, industry assets doubled from 2011 to 2014.4 Perhaps also not surprisingly, increased assets under management for liquid alts funds corresponded with lower returns. So far this decade, liquid alts funds have averaged returns of +1.5% annually, which is 2.0% lower than their average in the prior 10 years and 0.1% below the rate of inflation over this period.5 As returns from liquid alts have disappointed investors, sales have plunged, and investors have questioned the role of these strategies in their portfolios. At first glance, it appears that liquid alts have suffered from the all-too-common effect of increasing strategy assets leading to decreasing strategy returns.

The Fed’s Effect

Yet placing the blame for liquid alts’ reduced performance on rising assets under management doesn’t stand up to scrutiny. If increasing assets under management in liquid alts strategies were to blame for decreasing performance, we would expect the effect to show up in the strategies’ excess returns relative to a passive benchmark. Cash, a short duration risk-free asset, is the most relevant benchmark for liquid alts because many of the underlying activities use cash as collateral and, more fundamentally, the underlying activities tend to have low duration. For example, in event-driven strategies, the time horizon for an event such as a merger closure is typically measured in months or quarters, not years.

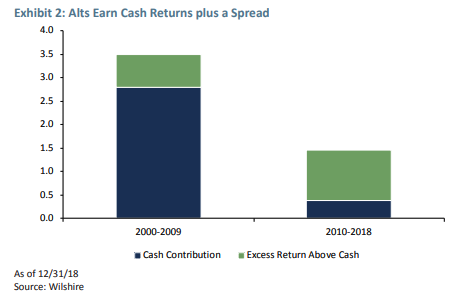

Rather than experiencing a degradation in excess returns since 2010, liquid alts have seen just the opposite. Exhibit 2 shows that from 2000 through 2009, alts returned an average +3.5% per year (net of fees). However, cash delivered an average return of +2.8%, so returns in excess of cash and fees during that period were only +0.7%. By contrast, while alts returns since 2010 have averaged just +1.5%, cash has only generated +0.4%, implying a +1.1% net-of-fee excess return over cash. Relative to cash, liquid alts have performed better since 2010 than over the prior decade.

If too much money flowing into liquid alts strategies doesn’t explain their decline in performance, what does? Lower returns on cash. Since 2010, cash yields have averaged 2.4% less than their 2000- 09 levels, more than accounting for the 2.0% drop in liquid alts performance. Unhappy liquid alts investors need look no further than the Eccles Building – home of the Federal Reserve – to find the source of their disappointment. Investors should recognize, however, that as the Fed has moved away from a zero interest rate policy to a target rate roughly equal to the rate of inflation, the real return prospects for cash, and by extension for liquid alts, look much improved relative to recent years.

Real Return Prospects for Alts

To build a real return forecast for liquid alts, we need to estimate the real return potential for cash and then estimate the potential for alts to deliver excess returns above that risk-free rate. Exhibit 3 shows that the Fed has hiked rates by 2.25% since December 2015, when it moved off its longstanding 0-0.25% target range. Exhibit 4 also shows that inflation expectations have been relatively stable over this period. As a result, current cash rates are modestly above the market’s expectation for inflation over the next seven years. That’s a significant improvement compared to the 1.8% spread between cash rates and the average rate of expected inflation that persisted from 2010-15. The Fed’s move away from zero nominal rates means that cash returns have transitioned from a headwind for alts to a tailwind. Our forecast methodology for cash is informed by market pricing over the next two years and an assumed terminal real cash rate seven years from now. Across the different mean reversion scenarios that we consider (see sidebar), we forecast real cash returns of 0.2% to 0.6%.

What does this mean for alts? If we look back on the full history, we can see in Exhibit 4 that the category has delivered 0.9% of incremental return above cash net of fees, which we estimate equates to about 2.25% before fees and other expenses. It’s worth noting that the excess returns plotted in Exhibit 3 have a correlation with equity markets of 0.8. Further, liquid alts lost to cash in 2001, 2008, 2011, 2015, and 2018 – all years in which the MSCI All Country World Index declined. To our minds, this correlation is a favorable feature of the liquid alts track record: it provides a hint that liquid alts are incurring some amount of equity-like risk – what we on GMO’s Asset Allocation team refer to as depression risk – and therefore deserve to earn a return premium above cash. For the purpose of looking at the prospects for alts broadly, we will assume that they continue to earn cash plus 2.25%, which when added to our forecasts for cash, equates to a targeted real return of about 2.5%-3%.

Alts vs. Equities

Alts look attractive relative to developed equity markets. Table 1 shows our forecasts for U.S. and non-U.S. developed equities under the assumptions of full, partial, and no mean reversion (see sidebar). Only the value half of non-U.S. developed markets look priced to outperform alts across this range of scenarios. Large cap U.S. stocks look priced to significantly underperform alts whether we get full (-2.5%) or partial (-0.3%) mean reversion. Only if U.S. equity valuations remain constant do their expected returns (+3.8%) exceed what alts ought to be able to deliver in that scenario (+2.6%).

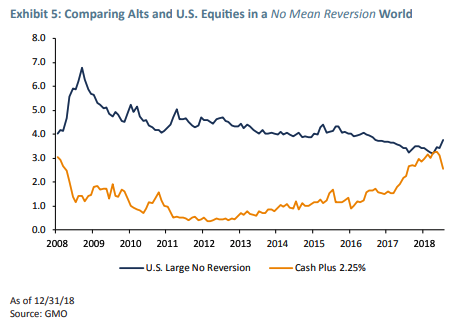

Investors who share our conviction in mean reversion have likely been underweight U.S. stocks for quite some time. In our Benchmark-Free Allocation Strategy, we eliminated the last of our long-only allocation to U.S. Quality stocks in February 2018 by converting the position into a relative value strategy and moving it to our alternatives allocation. Exhibit 5 shows why. It plots our no mean reversion forecast for U.S. stocks against our forecast for cash plus 2.25% from mid-2008 through the third quarter of 2018. The area between the two lines represents the return liquid alts need to generate above their historical track record in order to match the return from U.S. stocks (assuming valuations stay constant). The two lines crossed at the end of the third quarter, meaning alts didn’t need to generate any premium over their historical track record in order to match the returns from U.S. stocks in a world devoid of mean reversion. The fourth quarter’s equity sell-off and rally in short-term interest rates caused the spread to widen, but to a level that remains well below the spread seen for most of the past ten years. Prior to 2018, if you expected valuations to stay constant, then you would have clearly preferred U.S. stocks over alts. Today, however, even if you hold that view, Exhibit 5 shows that there’s likely an opportunity to diversify your portfolio without materially reducing your expected returns.

Determining just how much of your portfolio to steer away from equities and direct toward alts depends both on your expectations for mean reversion in equity markets and on the spread you expect alts to deliver above cash. While the 2.25% spread generated by liquid alts funds historically may be a plausible forecast for future returns, we believe GMO’s alts strategies have the potential to do better. To explain why, we now turn to our process for forecasting the return potential of alts.

Determining Our Target for GMO’s Alts

GMO’s Asset Allocation team uses a 7-year framework when forecasting returns for traditional asset classes. The basic building blocks of this framework are: 1) estimates of current valuations for each asset class; 2) estimates of the equilibrium return that investors will demand for owning each asset class; and 3) an assumption that prices will move one-seventh of the way from their current valuation to equilibrium valuations in a year. Unfortunately, a 7-year framework isn’t much help for calculating forecasted returns6 for many liquid alternatives due to the short duration of liquid alts strategies. Corporate takeovers will generally occur, or not, within a 6- to 18-month window; as a result, merger arbitrage doesn’t fit neatly into a 7-year framework. Actively managed strategies such as our Systematic Global Macro and Relative Value Rates & FX strategies, which react to both valuation and sentiment signals and as a result tend to turn over their portfolios in under a year, don’t fit either.

Developing return targets for alts requires that we step out of our 7-year forecasting framework. Our goal isn’t to come up with a precise methodology so that we can react to small changes in forecasts, nor do we aim to forecast any and all flavors of alts that an investor may consider. Rather, our goal is to build a mosaic of inputs that help us consider the prospects for the alts managed at GMO.7 We aim to take advantage of both the top-down, generalist views from our Asset Allocation team (what Daniel Kahneman would call the “outside view”) and the bottom-up, specialist views of the teams managing GMO’s alternative strategies (Kahneman’s “inside view”). For a given strategy, the outside view involves understanding the strategy’s exposure to the main systemic risks that we believe investors are paid to incur – depression, unanticipated inflation, and liquidity shock risk – and comparing those exposures to traditional asset classes. This helps us put a range on the projected long-term returns to a given strategy. The inside view builds upon the historical track record of a strategy and the team’s models for the current environment. Finally, we use our 7-year forecasts for cash as an estimate for the risk-free component of returns.

GMO’s alts fit into three broad categories: equity-oriented, event-driven, and relative value. To illustrate our approach to forecasting alts, let’s look at an example from each category:

■ Equity-oriented. GMO’s Risk Premium (put selling) Strategy systematically sells at the-money puts on equity market indices. The outside view of this strategy is rather straightforward: by selling puts we are exposed to the downside risk of equities; therefore, we ought to earn an equity-like return. As an approximation, we can think of the return to put selling as being one-half driven by equity markets and one-half driven by another risk premium, the volatility risk premium. In determining a target return for put selling, we place a one-half weight on our 7-year equity forecasts and a one-half weight on cash plus an estimate of the volatility risk premium, which our Global Equity team models as part of their investment process in managing the strategy.

■ Event-driven. GMO’s approach to event-driven investing centers on definitive agreement merger deals. These investments provide a return profile that is similar to investing in credit: most of the time, the majority of the positions make a relatively small amount of money and the gains from the investments that pay as planned (when the merger closes or, analogously, the bond coupons get paid) should compensate for the losses incurred by the few that don’t, despite the losses on most losing positions being much larger than the gains on the winners. Both merger arbitrage and credit investing have depression and liquidity shock risk, as merger deals are more likely to break and coupons are less likely to get paid when the economy and/or markets are doing poorly. While we think comparing merger deals to high yield bonds is helpful for thinking about the long-run returns to merger investing, we don’t expect the two activities to be so tightly related as to use changes in our high yield forecasts as a time-varying component of our forecasted returns for merger arbitrage.

■ Relative Value. Unlike put selling or merger arbitrage trading, we do not think investors should earn any premium above cash for systematically engaging in relative value trading of securities within the same asset class. Systematically buying a basket of stocks and shorting a different basket of stocks without any insight as to the composition of those two baskets should underperform cash due to transaction and financing costs. That means our relative value strategies rely on differentiated alpha views to earn a place in our portfolios. An example today is our view that a long position in developed non-U.S. value stocks, hedged with short positions in U.S. stocks and the relevant currencies, offers an attractive investment opportunity due to the valuation discount of non-U.S. stocks relative to U.S. equities. Although we use our 7-year forecasts when analyzing the relative value opportunity, the forecast return of a spread trade is not simply the forecast on the long asset less the forecast on the short asset. We must account for average returns over our rebalancing window, the transaction costs associated with rebalancing, and the optimal hedge ratio implied by the covariance of the asset classes in which we’re positioned.

As we look at our alternatives book strategy by strategy, we estimate that we can target a return of cash plus 3–4% from these strategies before any value added from specific security selection. Differentiating the return to an activity such as merger arbitrage from specific security selection is more of a theoretical distinction than a practical one. The distinction is clearer for the non-U.S. developed value stocks vs. S&P 500 relative value trade: our cash plus 3–4% target includes an assumption for the projected return of this trade if both legs of the trade were indexed. In practice, we actively manage the long book of this position because we believe that our Global Equity team can generate security selection alpha within the non-U.S developed value universe. Therefore, we hope to do better via security selection than the cash plus 3–4%.

While we arrive at our range of targeted returns for alts by considering the risks and opportunities embedded in GMO’s specific strategies, we are comforted by the fact that the historical 2.25% return premium delivered by liquid alts funds is close to what we hope to achieve from our own strategies. Whether our return target for GMO’s alts proves conservative, aggressive, or spot-on remains to be seen. But what we have already seen – that today’s cash yields are about the best they’ve been in the post-GFC period – in our view makes the future for liquid alts look brighter than the recent past.

Conclusion: Targeting 5%

Real With the rise in cash rates to the point where cash now may provide a positive real return, we think alternatives broadly have the potential to deliver 2.5–3% real returns for investors. We believe the alts in our portfolio may be poised to perform even better, with the potential to deliver up to 5% real returns in the coming years if our underlying investment teams can deliver the security selection alpha that we currently target. Alts join emerging market value stocks – our Asset Allocation team’s favorite asset class – in offering attractive return possibilities. Together, alternatives and emerging market value stocks comprise over 50% of GMO’s Benchmark-Free Allocation Strategy.8 As the name implies, we manage this strategy without concern for its tracking error relative to any particular benchmark. That said, we believe Benchmark-Free has the ability to outperform a traditional balanced portfolio over the medium-to-long-term. For context, a traditional portfolio that allocates 60% to the MSCI All Country World Index and 40% to fixed income will invest about 3.3% in emerging value stocks and will not hold any alts. With so little exposure to attractively priced equities and alternative investment strategies, we believe the traditional portfolio looks likely to disappoint. Our ability to invest a significant portion of the Benchmark-Free portfolio in alternatives is an important reason why we believe this portfolio is positioned to outperform traditional portfolios in the coming years.

While we still believe a 5% real return goal will prove a challenging bogey for a diversified portfolio over the next seven years, the improved return prospects for alts and emerging market value stocks may help us to position our portfolios to deliver against this objective. That said, in order to earn 5% real we need a few developments to break our way: we need the fundamentals of value stocks in emerging markets to be less bad than their valuations imply; we need our value-oriented security selection processes within asset classes to prove fruitful; and we need some volatility across asset classes to provide profitable rebalancing opportunities. We believe all these developments are reasonably likely, but whether or not they occur remains to be seen. In prior years, it also remained to be seen if, and when, cash rates would turn positive in real terms, thereby providing a needed boost to alternatives and other short duration strategies. Thanks to the recent rise in cash rates, we can check this development off our wish list.9 That is an important development for our portfolios, and a development that has us increasingly optimistic about their prospects.

John Thorndike. Mr. Thorndike is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2015, he was a managing director and Deputy CIO at The Investment Fund for Foundations. Previously, he was an analyst with TIFF. Mr. Thorndike earned his AB in Physics from Bowdoin College.

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security or adopt any investment strategy. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. GMO products and services may not be available in all jurisdictions or to all client types.

The views expressed herein are generally those of the named author [and the Asset Allocation team, which comprises professionals across multiple disciplines, including equity, alternative and fixed income], and are not intended to predict or depict performance of any investment. The views and recommendations of the author and the [Asset Allocation team] may not reflect the views of the firm as a whole and GMO advisors and portfolio managers may recommend or take contrary positions to the views and recommendation of the author [and the Asset Allocation team]. Indices are unmanaged and not available for direct investment. Past performance does not guarantee future results.

The projected/target returns in this paper are based on the author’s judgments about the risks incurred in certain investment strategies, the return investors would demand for incurring such risks in a hypothetical fairly valued market environment, and the current market environment. The author considered GMO’s proprietary 7-year forecast framework for certain return assumptions. For example, when considering the projected/target return for equity relative value strategies, the author considered a proprietary blend of GMO’s full, partial, and no-mean reversion forecasts for different segments of the global equity market along with assumptions about the covariance of those segments based on an analysis of historical returns.

Target returns are hypothetical in nature and are shown for illustrative, informational purposes only. This material is not intended to forecast or predict future events, but rather to demonstrate the investment process of GMO. Specifically, the projected/target returns are based upon a variety of estimates and assumptions by GMO of future returns including, among others, estimates of future operating results, the value of assets and market conditions at the time of disposition, related transaction costs and the timing and manner of disposition or other realization events. The returns and assumptions are inherently uncertain and are subject to numerous business, industry, market, regulatory, competitive and financial risks that are outside of GMO’s control. Certain of the assumptions have been made for modeling purposes and are unlikely to be realized. No representation or warranty is made as to the reasonableness of the assumptions made or that all assumptions used in achieving the returns have been stated or fully considered. Actual operating results, asset values, timing and manner of dispositions or other realization events and resolution of other factors taken into consideration may differ materially from the assumptions upon which estimates are based. Changes in the assumptions may have a material impact on the projected/target returns presented. The projected/target returns do not reflect the actual returns of any portfolio strategy and do not guarantee future results. All data is shown before fees, transactions costs and taxes and does not account for the effects of inflation. Management fees, transaction costs, and potential expenses are not considered and would reduce returns. Actual results experienced by clients may vary significantly from the hypothetical illustrations shown.

Target Returns May Not Materialize. The information in this presentation may contain projections or other forward-looking statements regarding future events, targets or expectations and is only current as of the date indicated. There is no assurance that such events or projections will occur, and may be significantly different than that shown here. The information in this presentation, including projections concerning financial market performance, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Target returns include the reinvestment of income, but do not include any advisory fees, trading costs or taxes an actual account may experience. Actual performance results will be reduced by advisory fees and any other expenses incurred in the management of the account. As fees are paid periodically, the compounding effect will increase the impact of fees. . For example, if the strategy were to achieve a 10% annual rate of return each year for ten years and an annual advisory fee of 0.75% were charged during that period, the resulting average annual net return (after the deduction of management fees) would be 9.25%. Actual fees are disclosed in Part 2 of GMO’s Form ADV and are also available in each strategy’s compliant presentation.

Disclaimer: The views expressed are the views of John Thorndike through the period ending January 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2019 by GMO LLC. All rights reserved.

1 Hereafter referred to as liquid alts or simply, alts.

2 As of September 30, 2018, Wilshire Associates defined the category to include 476 mutual funds across equity hedge, event-driven, global macro, multi-strategy, and relative value categories.

3 Throughout this white paper, we will use the Wilshire Liquid Alternative Index as a proxy for the category’s performance.

4 Liquid alternative mutual funds leave investors disappointed, Financial Times, May 22, 2016.

5 Performance as of 12/31/2018.

6 In this section, we’ll use returns as short-hand for the return premium above the cash rate.

7 GMO clients invest in alts through asset allocation mandates and through direct investments in alternatives strategies, either individually or through vehicles that offer exposure to multiple alts strategies.

8 As of December 31, 2018.

9 It’s now replaced with a desire to see cash rates remain positive in real terms.

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All