“Every man I meet wants to protect me. I can't figure out what from.” – Mae West

Stock market participants for most of the past few years have eschewed protection. It was all about making large amount of gains. Almost every advisor lost clients from “cocktail party” conversations about who had made the most money recently. We heard of retired clients that were not satisfied with only 10% to 20% gain a year. They would withdraw money from advisory account to speculate in technology stocks. And then, of course, there was the cryptocurrency craze.

Well, all of that has ended with a splat! We have entered a bear market (defined by a 20% drop from the high-level mark) according to most market indices. The technology sector declined 24% in less than two months. Energy stocks have been massive losers with losses of over 30% over the same period time. I don’t think I have to describe what has happened to bitcoin and its brethren.

What can we learn from 2018 and what do we see for 2019 (at least the first part of it)?

Slow and Steady Won the Sector Race in 2018

You couldn’t tell much about which business cycle phase we are in based on sector performance in 2018. Although some late cycle sectors such as health care and utilities had positive returns for the year (while the S&P 500 was down about 4%), typical early to mid-cycle sectors including consumer discretionary, real estate, and technology provided negative results but outperformed the broad market for the year. But both consumer discretionary and technology were more negative than the S&P 500 in the fourth quarter indicating that the economy is likely moving into a late-cycle phase where defensive and inflation-resistant sectors tend to outperform while cyclical sectors tend to underperform.

On the negative side, some sectors that historically have underperformed in the late cycle, did so, especially, financials and industrials. Other late cycle sectors, such as consumer staples, energy and materials, suffered greater than market losses. Consumer staples and materials rebounded in relations to the market in the fourth quarter indicating that we are moving to the end of this business cycle.

Real estate and energy performed unusually during the year. The chart below shows the 2018 performance of the S&P 500 in black, the real estate sector in red, and the energy sector in green. If we are going into the late cycle, we would expect the real estate sector to start underperforming. Not only did it give better than market results for the year, it was the second-best sector in the down fourth quarter. Given that utilities and real estate were the best sectors in Q4, the low and declining interest rates continue to help these sectors’ stock performances regardless of the business cycle.

On the other hand, energy tends to outperform in late cycle times when inflation heats up and demand is solid. But the combination of a lack of strong inflation globally and the turmoil amongst energy producing countries in trying to manage oil prices have hit these stocks hard.

Source: Barchart.Com

It’s Not Too Late (Cycle) to Diversify More Intensely

According to Fidelity, the late cycle phase tends to last about 18 months and stock returns tend to be below average but positive. If we are entering this cycle phase, we would expect that 2019 to be unusually volatile like 2018. For financial advisors and their clients with long-term goals, the number one concern this year should be the reduction of portfolio downside risk.

Diversification portfolio

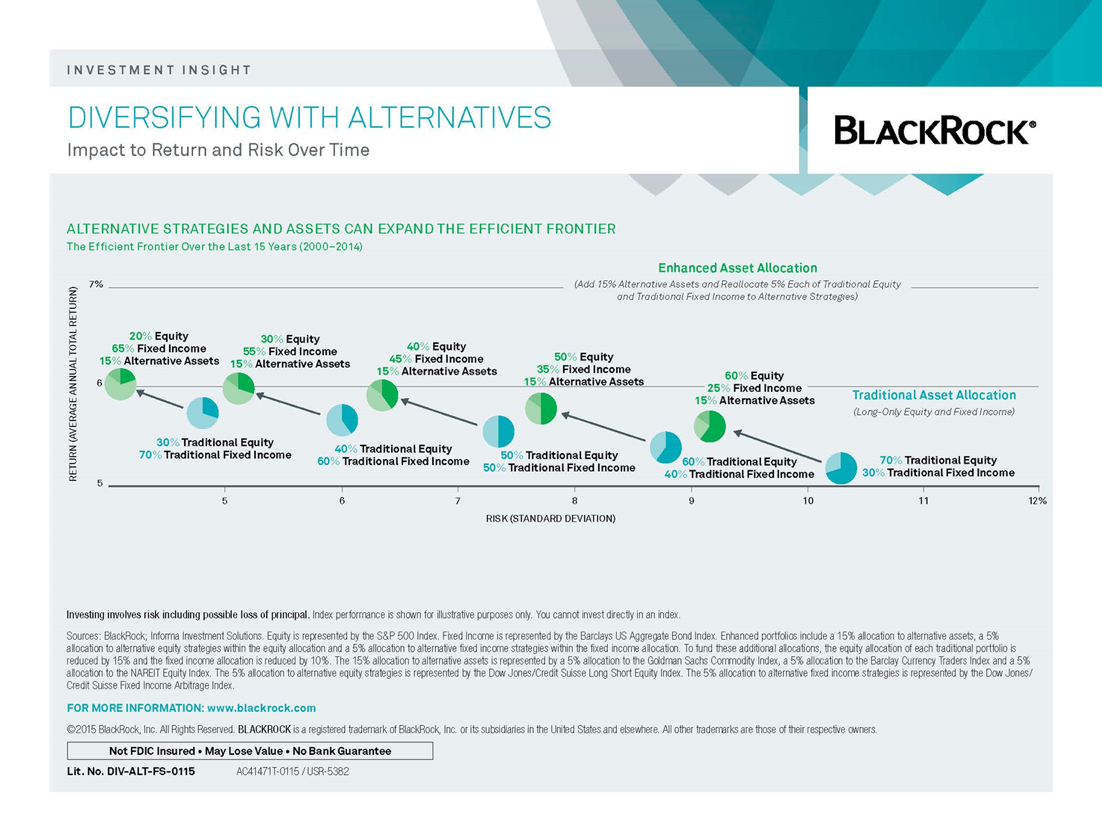

iSectors® believes that most portfolios are under-diversified. Given the availability of alternative exchange traded funds (ETFs) and mutual funds, advisors can now more thoroughly diversify their client portfolios. Bonds are not complete diversifiers, especially during this time of secularly rising interest rates. According to BlackRock, a 60% stock, 40% bond portfolio changed to a 50%, stock, 35% bond, 15% alternatives portfolio should earn higher returns with lower risk over time.

Source: BlackRock

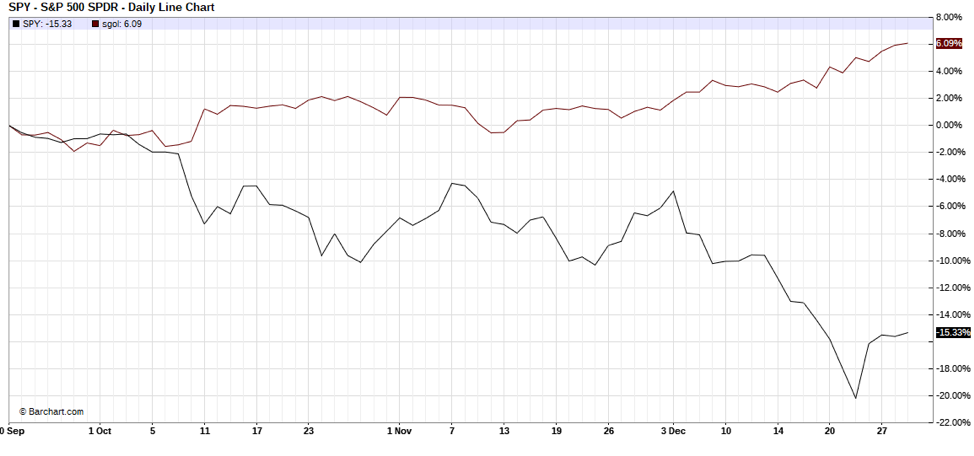

Doing the recent market decline, precious metals have been the star performers. Although stocks (in black) dropped as much as 20% from its September 20 highs, gold (as represented by the Aberdeen Standard Physical Swiss Gold Shares ETF – SGOL, in red) steadily climbed to new recent highs.

If your client’s portfolio is under $100,000, an investment in a gold bullion ETF or mutual fund can provide this diversification. If your client is taxable, please be aware of the different capital gains treatments among different types of funds. For larger clients, advisors may wish to consider diversified precious metals or inflation protection strategies available from third-party managers.

Source: Barchart.Com

Income portfolio

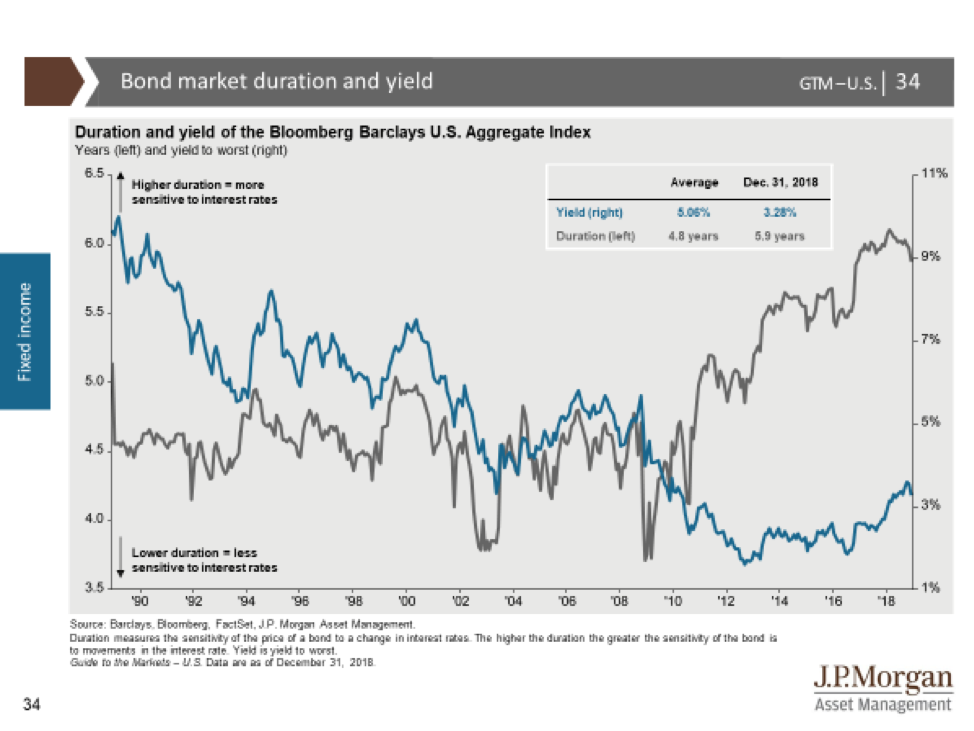

Bonds and other income strategies still have a place in client portfolios. Unfortunately, the Bloomberg Barclays Aggregate Index have become so long that strategies tied to the index are mainly exposed to interest movements and little else. As the chart below indicates, the duration (in black) or the interest risk of the index has risen almost 60% since 2009 while the yield (in blue) has declined. If we see interest rate increases in 2019, these strategies will be negatively impacted.

Source: J.P. Morgan Asset Management

iSectors recommends fixed income allocations be based on client needs. If the client needs income from the portfolio, there are high income strategies offered by third party managers. Be careful that the allocation utilized is truly diversified and not highly correlated to the equity market. If the strategy being researched is predominantly high dividend stocks and high yield corporate bonds, advisors should avoid it.

If the client’s primary need is diversification, a portfolio with balanced allocations to interest rate and credit risks should be considered. Be careful of utilizing “core plus” portfolios that can have concentrated risks that change at the manager’s discretion. Strategic fixed allocations with ongoing balanced allocations offered by third-party managers are worth the relatively low fees associated with them. These are available for taxable and tax-exempt clients.

Equity portfolio

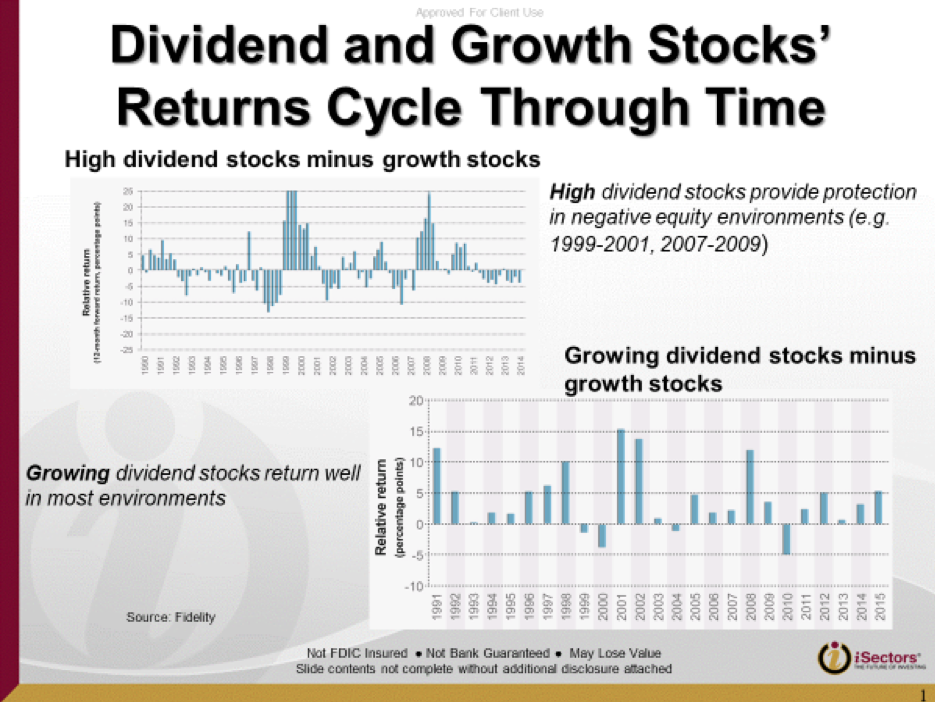

It is important for clients to keep invested during the downturns, so they can receive the long-run benefits of equity returns. As we enter the late cycle, income-oriented and sector allocation portfolios should be attractive. The addition of dividend funds will help protect the portfolio during market declines. Dividend growth funds comprise of companies that have historically or expected to increase their dividend rates consistently. These funds have historically performed well during market rallies. High dividend funds, which own companies that pay higher current yields to their shareholders, tend to provide protection in market declines.

Sources: Fidelity, iSectors

It is important to note that income-oriented portfolios should be complimented with growth-oriented portfolios to receive the benefit of market advances. A growth index fund allocation is one way to provide this boost to portfolio returns, although a sector allocation portfolio may be a more efficient tactic to take. These strategies utilize rules-based processes to attempt to outperform the market. The best sector allocation managers implement the following in their process:

- Focus on reducing downside risk as opposed to outperforming the market in every period

- Use forward looking indicators instead of backward price action such as trend following

- Invest in low to moderately correlated sectors to reduce risk concentration; and

- Utilization of ETFs and mutual funds to minimize single stock risk

Disclosure

© iSectors

Read more commentaries by iSectors