2018 ended with outsized volatility in equity markets. Even on days with no particular news for the market to digest, the normally quiet final week of the year featured dramatic price swings. Analysts blamed the market’s anxiety on falling economic momentum and rising concern about recession. However, U.S. economic indicators remain strong, and we expect continued growth even amid downside risks.

The deceleration reflected in our forecast has been widely expected. Tax reform had its maximum impact in the quarters immediately following its implementation, effects which will likely fade as we move through 2019. The return to regular rates of growth is not altogether disappointing, especially as the expansion approaches its tenth birthday.

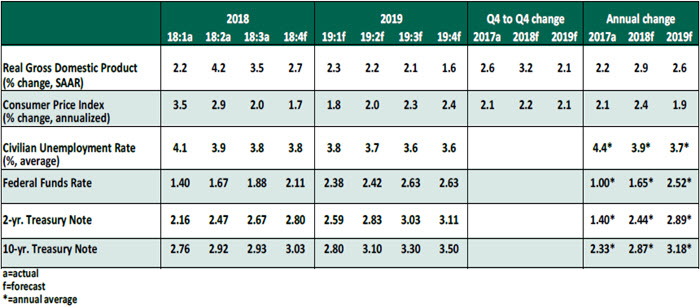

Key Economic Indicators

- The Federal Open Market Committee executed a widely expected rate increase following its December 19 meeting. In remarks following the meeting, Fed chair Jerome Powell emphasized that the new rate range of 2.25-2.50% is now within the estimated range of the “neutral” rate. Markets reacted negatively, specifically in response to Powell’s comments that the Fed will run off its balance sheet “on automatic pilot,” appearing to disregard market signals.

- In light of subsequently dovish Fed commentary and a range of global uncertainties, we have revised our forecast to include only one federal funds rate increase in 2019, likely in June.

- While employment continues to surprise on the upside, the carryover to wages and inflation remains muted. With inflation risk modest, delaying interest rate increases to await additional clarity on the outlook seems wise.

- December’s unemployment report continued a years-long streak of good news. 312,000 jobs were added last month, well beyond consensus expectations. Job gains in prior months were also revised upward, yielding a monthly average of 220,000 new jobs for 2018. The unemployment rate rose slightly to 3.9% for an encouraging reason: The labor force participation rate showed more marginal workers re-entering the workforce.

- Average hourly earnings grew by 3.2% year-over-year, the fastest pace seen in this economic cycle. The upward trend in wage growth suggests employers are approaching the limits of labor market slack and are increasing wages to attract and retain workers.

- Despite higher wages, inflation remains subdued, in large part due to lower energy and fuel costs. The Consumer Price Index grew 2.2% year-over-year in November, a slide following a year that peaked at 2.9% as recently as July. Core personal consumption expenditures, which exclude food and energy, grew 1.9%.

- In its final revision, third-quarter gross domestic product (GDP) growth was revised down slightly to 3.4% on an annualized basis, confirming a quarter of solid economic performance. Fourth-quarter GDP is expected to grow more slowly, but at a sufficient pace to maintain a full-year growth rate of over 3%. Upcoming readings of GDP may be delayed, as the U.S. Bureau of Economic Analysis is closed during the shutdown.

- Manufacturers appear braced for a slower year, with the Institute for Supply Managers’ composite U.S. Private Manufacturers’ Index (PMI) falling to 54.1 in December from 59.3 in November. The declines were mirrored in many other countries. Though not yet a cause for alarm, as a PMI value over 50 indicates expansion, slower growth is on the horizon.

- The U.S. and China have resumed trade negotiations in earnest. The temporary reprieve agreed at November’s G-20 meeting, in which the U.S. postponed a tariff increase from 10% to 25% on $200 billion of imported goods, will expire on March 1. Cracks are emerging in the Chinese economy, with its manufacturing PMI shifting to contraction. We believe the deteriorating condition of the Chinese market combined with U.S. leadership’s appetite for a trade win will motivate both sides to negotiate a new trade deal in the year ahead.

© Northern Trust

northerntrust.com/disclosures