Alternative investments have been used by some investors to diversify their holdings, and these may potentially help reduce overall portfolio risk when the appropriate strategies are implemented properly. Over the past year, the Invesco Global Solutions team examined hundreds of financial advisor portfolios, and we discovered that a common source of hidden risk is unintended equity exposure within alternative allocations, which can have an adverse effect on portfolio performance during equity market downturns. Fortunately, there are solutions that can potentially mitigate this risk and help investors achieve desired results.

Why alternatives?

Alternatives are any investment that falls outside of the boundaries of traditional, long-only positions in stocks and bonds. They include asset classes such as multi-asset strategies, absolute return strategies, equity strategies that can take short positions, real estate, infrastructure, master limited partnerships and more.

The main objective of including alternatives within a portfolio is to provide a differentiated source of return outside of the traditional equity and fixed income markets, as well as reduce overall portfolio volatility.1 As we approach the later innings of the equity bull market cycle, many investors and advisors are asking where to obtain the returns they are looking for and how to improve portfolio downside risk.

Figure 1 illustrates that a diversified alternatives portfolio has had similar returns as equities over the past 20 years, while delivering less downside risk in adverse market conditions during this period.

Alternatives have slightly outperformed equities when stock markets are stressed

Source: Invesco, August 1998 – March 2018. Past performance is not a guarantee of future results. Investments cannot be made directly into an index. Alternatives portfolio is represented by a portfolio consisting of: 20% Inflation-hedging assets; 20% Principal preservation strategies; 20% Portfolio diversification strategies; 20% Equity diversification strategies; 20% Fixed income diversification strategies. Traditional 60/40 Portfolio is represented by 60% S&P 500 Index and 40% Bloomberg Barclays US Aggregate Bond Index. Equities are represented by the S&P 500 Index. Fixed Income is represented by the Barclays U.S. Aggregate Bond Index. 20% Inflation-hedging assets are represented by 15% FTSE NAREIT US Real Estate Index Series, All Equity REITs and 5% Bloomberg Commodity Index. The 15%/5% split reflects Invesco’s belief that investors tend to invest in strategies with which they are more familiar. 20% Principal preservation strategies are represented by the BarclayHedge Equity Market Neutral Index. 20% Portfolio diversification strategies are represented by 12% BarclayHedge Global Macro Index and 8% BarclayHedge Multi-Strategy Index. Multi-strategy is underweighted in this example due to its potential overlap with global macro. 20 % Equity diversification strategies are represented by the BarclayHedge Long/Short Index. 20 % Fixed income diversification strategies are represented by the 20 % BarclayHedge Fixed Income Arbitrage Index.

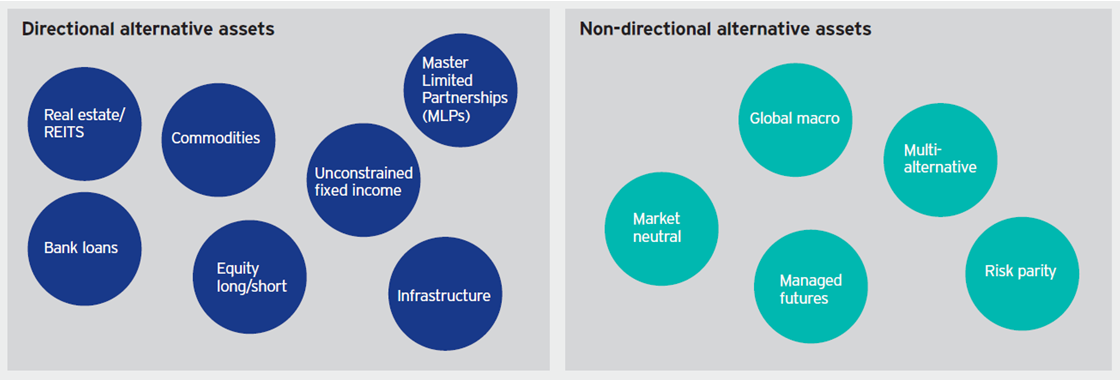

Yet, some types of alternative strategies tend to be more correlated to equities while others behave more independently. Figure 2 categorizes alternative strategies into two groups — directional alternative assets which tend to move with the overall equity market (have higher correlation2), and non-directional alternative assets which generally don’t move with the overall equity market (have lower correlation). Both types have potential benefits, but when diversification is the goal, it’s important to understand how to combine them in a holistic portfolio.

Alternative performance can be correlated to equities or behave independently

For illustrative purposes only

What did our analysis reveal?

One way the Invesco Global Solutions team helps advisors is through our Custom Portfolio Analysis (CPA) service. We compiled portfolio data from 121 CPAs performed in the second quarter of 2018 to assemble an up-to-date snapshot of portfolio construction insights.

Analysis of these CPAs uncovered a pervasive misapplication of alternatives, as some 68% of the alternatives sleeves we reviewed demonstrated unduly high correlation to their corresponding equities. Therefore, these portfolios are less likely to capture the full diversification potential of alternatives and may be more sensitive to downturns in the equity market.

How to fund alternatives in a portfolio?

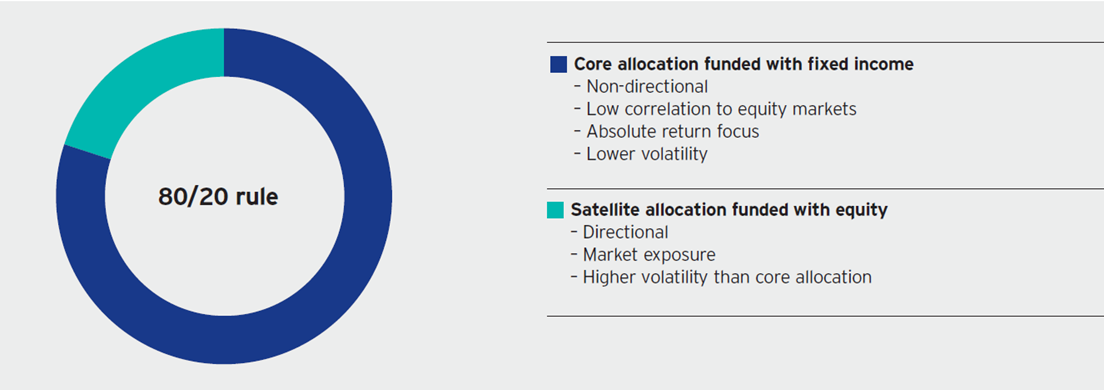

So, how can advisors avoid this hidden risk? By making intentional choices about which alternatives to use, and whether to take assets from equities or fixed income to fund that allocation. One simple method is to implement an 80/20 core-satellite approach for the alternatives sleeve.

Core:

- 80% of the alternatives sleeve is allocated to a core alternatives allocation.

- Assets are re-directed from fixed income as the funding source.

- The core allocation includes non-directional alternative strategies that historically have had low correlation to equities and lower volatility. (Past performance does not guarantee future results)

Satellite:

- The remaining 20% is funded from equities

- The satellite includes directional strategies that historically have had higher equity market exposure and higher volatility than the core allocation. (Past performance does not guarantee future results.)

An illustration of a core-satellite approach to alternatives

Source: Invesco, as of Sept. 30, 2018. For illustrative purposes only. Holdings are subject to change and are not buy/sell recommendations.

Key takeaway: Diversify alternatives exposure with non-directional investments

For portfolios that are underweight core alternative strategies, adding non-directional strategies can potentially mitigate overall portfolio risk while maintaining a similar return profile.

Important information

Blog header image: Africa Studio/Shutterstock.com

1 Volatility is defined by standard deviation.

2 Correlation is the degree to which two investments have historically moved in relation to each other. In this case, it is based on five-year returns.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The Bloomberg Barclays U.S. Aggregate Bond Index is an unmanaged index considered representative of the US investment-grade, fixed-rate bond market.

The FTSE NAREIT All Equity REIT Index is an unmanaged index considered representative of US REITs.

The Bloomberg Commodity Index is a broadly diversified commodity price index.

The BarclayHedge Equity Market Neutral Index includes funds that attempt to exploit equity market inefficiencies and usually involves being simultaneously long and short matched equity portfolios of the same size within a country.

The BarclayHedge Fixed Income Arbitrage Index includes funds that aim to profit from price anomalies between related interest rate securities.

The BarclayHedge Global Macro Index includes funds that carry long and short positions in any of the world’s major capital or derivative markets.

The BarclayHedge Long/Short Index includes funds that employ a directional strategy involving equity-oriented investing on both the long and short sides of the market.

The BarclayHedge Multi-Strategy Index includes funds that are characterized by their ability to dynamically allocate capital among strategies falling within several traditional hedge fund disciplines.

Alternative investments can be less liquid and more volatile than traditional investments such as stocks and bonds, and often lack longer-term track records.

Alternative products typically hold more non-traditional investments and employ more complex trading strategies, including hedging and leveraging through derivatives, short selling and opportunistic strategies that change with market conditions. Investors considering alternatives should be aware of their unique characteristics and additional risks from the strategies they use. Like all investments, performance will fluctuate. You can lose money.

Long positions are buying a security with the expectation that it will increase in value.

Short positions/short selling is the sale of a security not owned by the seller, then buying later. The belief is that security prices will decline and the price paid to buy it back at will be lower than the price it was sold.

Most master limited partnerships (MLPs) operate in the energy sector and are subject to the risks generally applicable to companies in that sector, including commodity pricing risk, supply and demand risk, depletion risk and exploration risk. MLPs are also subject to the risk that regulatory or legislative changes could eliminate the tax benefits enjoyed by MLPs, which could have a negative impact on the after-tax income available for distribution by the MLPs and/or the value of the portfolio’s investments.

Although the characteristics of MLPs closely resemble a traditional limited partnership, a major difference is that MLPs may trade on a public exchange or in the over-the-counter market. Although this provides a certain amount of liquidity, MLP interests may be less liquid and subject to more abrupt or erratic price movements than conventional publicly traded securities. The risks of investing in an MLP are similar to those of investing in a partnership and include more flexible governance structures, which could result in less protection for investors than investments in a corporation. MLPs are generally considered interest-rate-sensitive investments. During periods of interest rate volatility, these investments may not provide attractive returns.

Investments in real estate related instruments may be affected by economic, legal, or environmental factors that affect property values, rents or occupancies of real estate. Real estate companies, including REITs or similar structures, tend to be small and mid-cap companies and their shares may be more volatile and less liquid.

Investment in infrastructure-related companies may be subject to high interest costs in connection with capital construction programs, costs associated with environmental and other regulations, the effects of economic slowdown and surplus capacity, the effects of energy conservation policies, governmental regulation and other factors.

Christopher Hamilton, CFA®, CAIA

Head of Portfolio Advisory, Invesco Global Investment Solutions

Christopher Hamilton is Head of Portfolio Advisory for Invesco Global Investment Solutions. In this role, Mr. Hamilton leads Advisory Solutions efforts in the wealth management intermediary marketplace, with a focus on providing multi-asset portfolio construction research and guidance to financial advisors and wealth management platforms. As part of the Invesco Global Solutions franchise, he works to deliver in-depth portfolio research, analytics tools and investment solutions to investors across North America.

Prior to assuming his current position, he was part of the Wealth Management Intermediary strategy team, focused on developing multi-faceted distribution strategies for key clients across multiple channels. Prior to joining Invesco, Mr. Hamilton was a portfolio manager for U.S. Trust, focused on building out asset allocation and portfolio construction frameworks, and leading manager selection efforts for high-net worth individuals and institutions. He was also director of business analysis for Phillips 66, where he engaged in merger, acquisition and divestiture efforts, as well as capital market activities for the organization.

Mr. Hamilton earned a BA degree in economics from the University of Illinois at Urbana-Champaign, and an MBA from Rice University. He holds the Series 7, 63 and 66 registrations. He also holds the Chartered Financial Analyst® (CFA) designation, the Chartered Alternative Investment Analyst (CAIA) designation, and is a member of the CFA Society of Houston.

Neil Patel, CFA®, CAIA

Vice President of Portfolio Advisory, Invesco Global Advisory Solutions

Neil Patel is Vice President of Portfolio Advisory for Invesco Global Advisory Solutions. In this role, Mr. Patel is responsible for Advisory Solutions efforts in the US retail and institutional marketplace, with a focus on providing multi-asset portfolio construction research and guidance to financial advisors, wealth management platforms, institutions. As part of the Invesco Global Solutions, he delivers in-depth portfolio research, analytics tools to investors across the country.

Prior to joining Invesco, Neil worked for Graystone Consulting, the institutional consulting arm of Morgan Stanley. He focused on building out asset allocation and portfolio construction frameworks, and leading manager selection efforts for endowments, pensions, foundations, family offices, and High Net-Worth Individuals. Additionally, Neil has worked in other areas within the financial services industry including Equity Research, Private Equity, and Trading.

Mr. Patel earned a BS degree from the University of Texas at Austin and an MBA degree from Rice University. He also holds the Chartered Financial Analyst® (CFA) designation, the Chartered Alternative Investment Analyst (CAIA) designation, and is a member of the CFA Society of Austin.

Read more commentaries by Invesco Blog