Gold Miners Are Crushing the Market in the Face of Higher Rates

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSummary:

- Anticipating trouble ahead, fund managers make a historic rotation out of equities into bonds.

- Gold and gold mining stocks have been the one bright spot this quarter.

- Tax reform turns one year old. Has it achieved what was expected?

Disregarding strong opposition from the likes of DoubleLine Capital founder Jeffrey Gundlach, legendary hedge fund manager Stanley Druckenmiller, “Mad Money” host Jim Cramer, President Donald Trump and others, Federal Reserve Chairman Jerome Powell hiked rates on Wednesday for the fourth time in 2018.

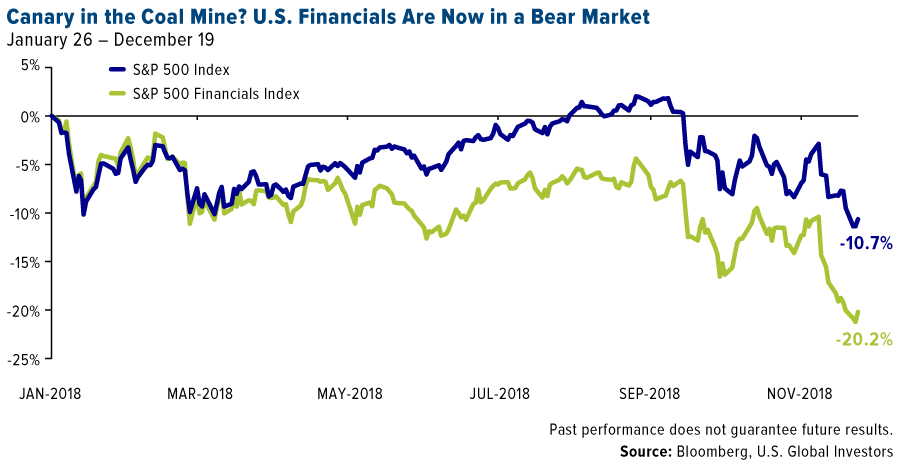

Markets responded negatively, with the Dow Jones Industrial Average jumping around in a nearly 890-point range before closing at its lowest level in more than a year. Meanwhile, the small-cap Russell 2000 Index has fallen into a bear market, down more than 22 percent since its peak at the end of August, and the S&P 500 Index is on track for not only its worst year since 2008, but also its worst month since 1931.

Among the sectors now in a bear market is financials, down around 20 percent since its peak in January. Regional banks, as measured by the KBW Regional Bank Index, have been banged up even worse, having fallen close to 30 percent since their all-time high in early June.

I bring up financials here because the sector is sometimes considered to be the “canary in the coal mine,” for the very good reason that financial institutions are highly exposed to the performance of the broader market.

What’s more, we learned this week that lenders are starting to pull back from riskier loans, a sign that they’re getting more cautious as recession fears loom. According to the New York Fed, the credit card rejection rate in October climbed to 21.2 percent, well above the year-ago rate of 15.7 percent. Banks also cut off credit from 7 percent of customers, the highest rate since 2013.

Fund Managers De-Risk in Favor of Bonds and Cash

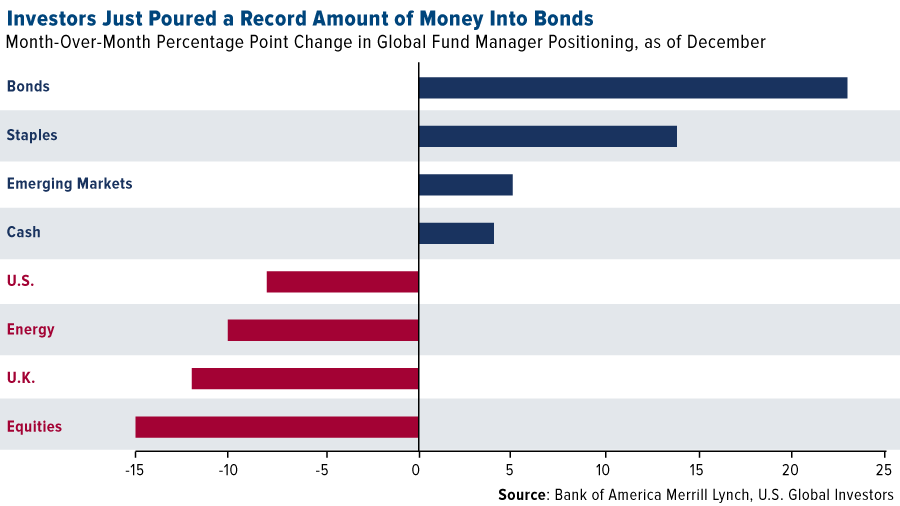

Against this backdrop, fund managers have turned incredibly bearish on risk assets and bullish on defensive positions such as bonds, staples and cash. According to Zero Hedge’s analysis of a Bank of America Merrill Lynch report, this December represents “the biggest ever one-month rotation into bonds class as investors dumped equities around the globe while bond allocations rose 23 percentage points to net 35 percent underweight.” Fund managers’ average cash levels stood at 4.7 percent in November, above the 10-year average, according to Morningstar data.

Equity outflows have been particularly pronounced. Lipper data shows that, in the week ended December 13, as much as $46 billion fled U.S. stock mutual funds and ETFs. That’s the most ever for a one-week period. It’s very possible that the selling is related to end-of-year tax-loss harvesting, but again, we’ve never seen outflows of this magnitude.

As such, I highly encourage investors to heed the recent advice from Goldman Sachs: Get defensive by positioning yourself in “high-quality” stocks. This probably isn’t the time to speculate.

Gold Has Been the One Bright Spot

I would also recommend gold and gold stocks. The yellow metal, as expected, is performing well at the moment, and commodity traders have taken a net bullish position for the first time since July. So far this quarter, gold has crushed the market, returning around 6 percent as of December 21, compared to negative 15 percent for the S&P 500 Index. Gold miners, though, as measured by the NYSE Arca Gold Miners Index, have been the top performer, climbing a phenomenal 12.3 percent.

On yesterday’s episode of “Mad Money,” Jim Cramer aired his frustration with the Fed’s decision to move ahead with another rate hike, predicting that the central bank will “have to reverse course, maybe in the next four months.” When and if that happens, “you’ll regret selling because the market will rebound so fast.”

But in the meantime, Cramer says, investors should consider buying into the “bull market” in gold. He added that he likes Randgold Resources.

You can read more of my thoughts on gold and gold mining stocks by clicking here.

Is It Time for the Fed to Take a Breather?

Although there’s more to the selloff than higher interest rates—a looming government shutdown tops the list—industry leaders have been quick to point fingers at the Fed’s long-term accommodative policy. Speaking to CNBC this week, Jeffrey Gundlach commented that the problem isn’t so much that the Fed is currently hiking rates. The problem, he says, “is that the Fed shouldn’t have kept them so low for so long.”

Stanley Druckenmiller made a similar argument, writing in a Wall Street Journal op-ed that, in a best-case scenario, “the Fed would have stopped [quantitative easing] in 2010” when the recession ended. Doing so, he says, would have helped mitigate a number of problems, including “asset-price inflation, a government-debt explosion, a boom in covenant-free corporate debt and unearned-wealth inequality.” Too late now.

Other analysts have highlighted the untimeliness of this month’s rate hike. According to Bloomberg’s Lu Wang, rate hikes are “exceedingly rare” when “stocks are behaving this badly.” Not since 1994, Lu says, has the Fed decided to tighten in such a volatile market. Nor has it ever tightened like this when the budget deficit was expanding, as it is right now. (I’ll have more to say on the deficit later.)

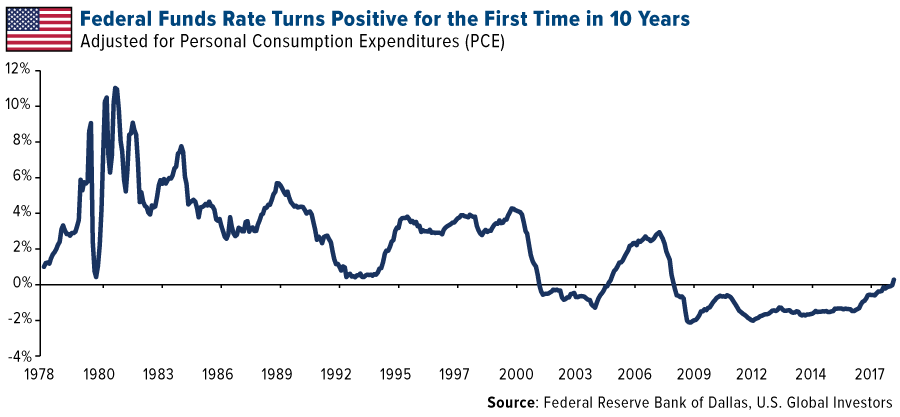

Then again, there’s a case to be made that, should another recession strike, the Fed needs the ammunition to stanch further losses. If it doesn’t hike now, it won’t have the option to lower rates later. That’s the argument made by Axios’ Felix Salmon, who believes “the only way to prevent another catastrophic asset bubble is to allow interest rates to revert to something much more normal.”

Salmon points out that, when adjusted for personal consumption expenditures (PCE)—the Fed’s preferred measure of inflation—the federal funds rate is now positive for the first time in over a decade. That’s “something to be welcomed,” he says.

Deficit Is “Unprecedented” in Such a Strong Economy

There are other worrisome economic signs, including the ballooning deficit. I was surprised to learn this week that, outside of a war or recession, the U.S. deficit has never been as high as it is now. That’s according to the Committee for a Responsible Federal Budget (CRFB), which reports that the budget deficit in 2018 is projected to total around $970 billion, up more than 45 percent from $666 billion last year.

“This borrowing,” says the CRFB, “is virtually unprecedented in current economic conditions.”

Normally, deficits expand during recessions and shrink during times of economic growth. But because of increased entitlement spending and other obligations, not to mention higher debt service on interest payments, the government’s outlays are far outpacing revenues.

The Tax Cuts and Jobs Act Turns One Year Old

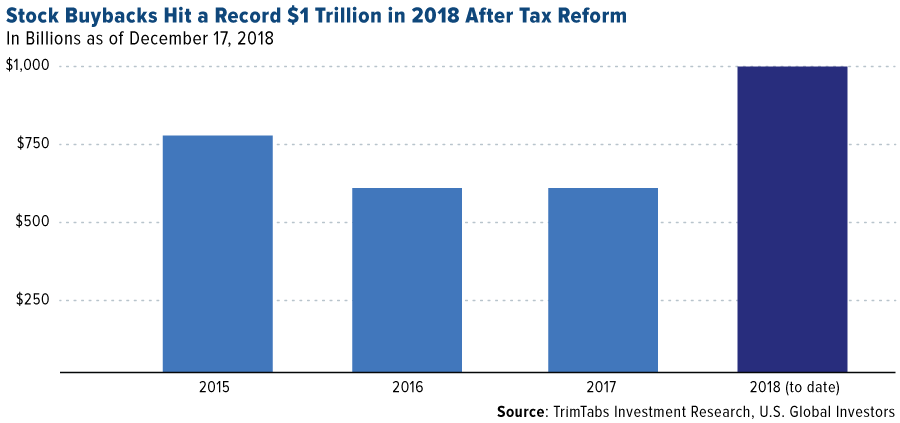

That brings me to the issue of corporate taxes. One year ago this weekend, President Donald Trump signed into law the Tax Cuts and Jobs Act (TCJA), which, among other things, cut the corporate income tax rate from 35 percent to 21 percent. It was initially estimated that as much as $4 trillion would be repatriated back to the U.S. by multinational corporations that have long held hordes of cash overseas in more tax-friendly jurisdictions. So, has this happened?

I’m pleased to see the tax law working. Companies are indeed bringing funds back, though admittedly at much lower rates than was anticipated. According to data released this week by the Commerce Department, only $92.7 billion in offshore cash was repatriated during the September quarter. That’s the lowest quarterly amount this year and 50 percent down from the second quarter. All combined, a little more than half a trillion dollars have returned to the U.S. It’s a good start, even if it falls short of expectations.

Another projection was that companies would plow their tax savings back into employees, new equipment and overall expansion. Here the outcome is more mixed. Wages jumped 3.1 percent in the third quarter, the fastest rate in over a decade, which I believe can be directly attributed to the tax law.

But the biggest consequence of the tax law by far has been corporations’ historic buybacks of their own stock. For the first time ever, $1 trillion was spent this year on stock repurchases. That beats the prior record of $781 billion set in 2015.

These buybacks helped stocks head higher this year—until they didn’t—but they’ve been strongly criticized for a number of reasons. One criticism is that aggressive buyback programs are often launched when stock prices are elevated, rather than when they’re on sale.

With most of the S&P 500 now in a bear market, many stocks certainly look like a bargain. I would proceed with caution, however, and make sure that I’m following the 10 percent Golden Rule: 5 percent in physical gold and the other 5 percent in well-managed gold mutual fund and ETFs. Now would be a great time to rebalance.

On a final note, I want to wish all readers and shareholders a very Merry Christmas! May this time bring you comfort and happiness as we head into a new year. Watch my special holiday message below.

Gold Market

This week spot gold closed at $1,255.66 up $17.21 per ounce, or 1.39 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.83 percent. The S&P/TSX Venture Index came in off 4.53 percent. The U.S. Trade-Weighted Dollar fell 0.44 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-17 | Eurozone CPI Core YoY | 1.0% | 1.0% | 1.0% |

| Dec-18 | Housing Starts | 1226k | 1256k | 1217k |

| Dec-19 | FOMC Rate Decision (Upper Bound) | 2.50% | 2.50% | 2.25% |

| Dec-20 | Initial Jobless Claims | 215k | 214k | 206k |

| Dec-21 | GDP Annualized QoQ | 3.5% | 3.4% | 3.5% |

| Dec-21 | Durable Goods Orders | 1.6% | 0.8% | -4.3% |

| Dec-27 | Hong Kong Exports YoY | 7.3% | -- | 14.6% |

| Dec-27 | Initial Jobless Claims | 219k | -- | 214k |

| Dec-27 | New Home Sales | 569k | -- | 544k |

| Dec-27 | Conf. Board Consumer Confidence | 133.0 | -- | 135.7 |

| Dec-28 | Germany CPI YoY | 1.9% | -- | 2.3% |

Strengths

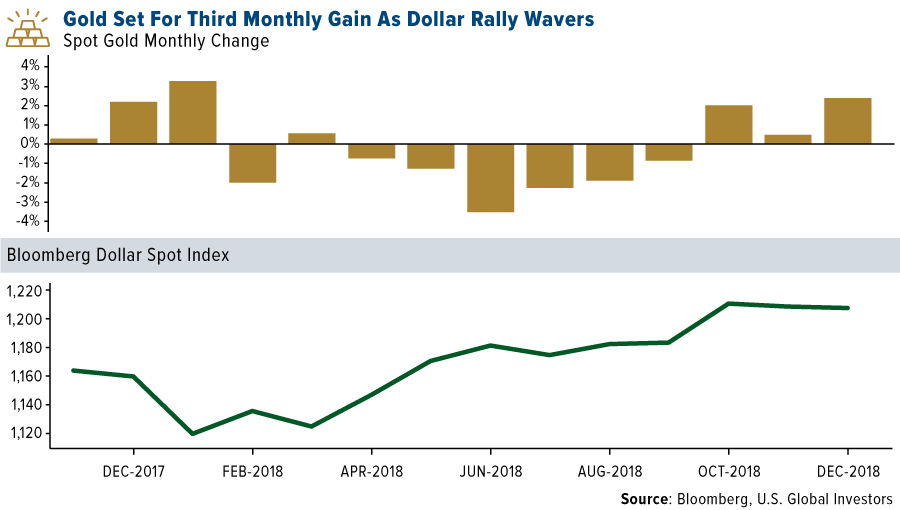

- The best performing metal this week was gold, up 1.39 percent. Gold traders continue to be bullish on the yellow metal amid concerns about economic growth, as measured by the weekly Bloomberg survey. ETFs backed by gold saw holdings increase for 10 days straight, bringing this year’s net purchases to 1.47 million ounces, according to data compiled by Bloomberg. Gold stocks did well this week as the spot price of gold broke above its 200-day moving average for the first time since this summer. Not only is bullion set for a third straight month of gains, it’s also set for the best quarter since 2017, as equities become shaky and the dollar heads for its worst week since March. Hedge funds raised their net long position in the gold futures market to a six-month high.

- Demand for gold in India has been falling, due in part to government measures and higher local prices, which has forced jewelers to adapt online purchases to be more appealing to young buyers. Retailers are offering gold for just one rupee, then buyers will receive physical delivery of their gold once they have paid enough for one gram of gold, which stands around 3,200 rupees, reports Bloomberg. This low barrier of entry, it is hoped, will spark greater demand, and since its launch last year, about 3 million people have already transacted on the online platform.

- Several central banks are buying up gold just in time for Christmas. Turkey has continued to increase its holdings week after week. They’ve risen by $257 million from last week, bringing total reserves to $19.6 worth of bullion. Russia’s reserves of the yellow metal climbed to 66.43 million ounces in October, up from 65.47 in September. Bloomberg data shows that India has also been steadily adding to its holdings this year and that Mongolia added ounces in October. Swiss gold exports rose 57 percent in November to 126.8 tones; however, imports fell 30 percent to 144.5 tons, according to data on the Swiss Federal Customs Administration website.

Weaknesses

- The worst performing metal this week was palladium, down 1.03 percent despite hedge funds raising their net long position over the week. Gold fell on Wednesday by 0.2 percent after the Federal Reserve announced another interest rate hike and signaled two additional hikes in 2019. Tai Wong from BMO Capital Markets told Bloomberg in a phone interview that the Fed is “not as dovish as the market expected – it’s a little bit of a disappointment.” Big name investors such as Stan Druckenmiller and Jeffrey Gundlach both said the Fed should pause its interest rate hiking due to the economy slowing and markets falling. President Donald Trump also urged the Fed, via Twitter, to cease the rate hikes to avoid making “yet another mistake.”

- Investors are becoming increasingly bearish on stocks and are pouring their cash into bonds. According to the Bank of America Merrill Lynch’s global fund manager survey published on Tuesday, money managers have increased their allocation to bonds by 23 percentage points, which is the biggest ever one-month rotation. The survey also showed that over half of respondents said they reckon global expansion will slow over the next two months, reports Bloomberg. Additionally, U.S. homebuilder sentiment fell this month to the lowest level since 2015, signaling that the industry’s struggles are growing amid higher prices and higher borrowing costs.

- Chinese President Xi Jinping said in a speech to party officials this week that China will stick to its policy agenda, despite pressure from other nations to allow more competition in its economic system, reports Bloomberg News. Xi said that “no one is in the position to dictate to the Chinese people what should and should not be done.”

Opportunities

- Credit Suisse analyst Fahad Tariq wrote in a note this week that gold mining equities are at an attractive entry point heading into 2019 and expects the yellow metal to gain more with an average price of $1,275 for the year. BMO Capital Markets also recommends increased exposure to gold due to concerns of the slowing global industrial economy. The group forecasts gold prices to average $1,260 per ounce in the first quarter of next year and that it will reach $1,300 in the second quarter.

- Saxo Bank says that silver could be set up for a move soon due to the bounce in gold, reports Bloomberg. Ole Hansen, head of commodity strategy at the bank, says the gold-to-silver ratio is currently in favor of higher silver prices, showing that silver is the cheapest relative to gold in 25 years. Hansen says “silver needs three things to run higher: higher gold, weaker dollar and stronger industrial metals” and that “so far only the gold box can be ticked.”

- A Bloomberg survey of 20 analysts and traders projected an increase in gold prices with a median estimate of $1,325 an ounce for the end of 2019. Almost all respondents said they were bullish on gold, even as the precious metal heads for its first yearly loss in three years. Mike McGlone, Bloomberg Intelligence commodity strategist, writes that it is unlikely that the U.S. dollar will remain atop the list of best-performing assets in 2019. The amount of offshore cash repatriated fell almost 50 percent in the third quarter of this year compared with the second quarter, to just $92.7 billion. The corporate tax cuts signed into law one year ago were expected to bring back more than $4 trillion to the U.S., according to President Trump.

Threats

- Goldman Sachs is warning clients to get defense amid the high uncertainty around the stock market for next year. The bank cited recent meetings with clients in saying that many investors believe the U.S. economy will fall into a recession in 2020 and are concerned because the S&P 500 has fallen by more than 10 percent a quarter of the time in the year before a recession in years going back to 1928, writes Bloomberg’s Joanna Ossinger.

- Fed policymakers’ new economic projections show that interest rate increases will start to hit the U.S. economy in 2020, which could lead to rising unemployment. This is bad news, especially as it comes during a presidential election year.

- Akira Takei, global fixed income manager in Tokyo at Asset Management One, told Bloomberg this week that he “expect[s] the global economy to be substantially worse in 2019 than this year,” citing recent drops in bond yields and equities. Globally, bonds with negative yields total $7.9 trillion, up from the 2017 low of $5.7 trillion reached in October, reports Bloomberg.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 6.87 percent. The S&P 500 Stock Index fell 7.05 percent, while the Nasdaq Composite also fell 8.36 percent. The Russell 2000 small capitalization index lost 8.42 percent this week.

- The Hang Seng Composite lost 2.21 percent this week; while Taiwan was down 1.00 percent and the KOSPI fell 0.38 percent.

- The 10-year Treasury bond yield fell 11 basis points to 2.78 percent.

Domestic Equity Market

Strengths

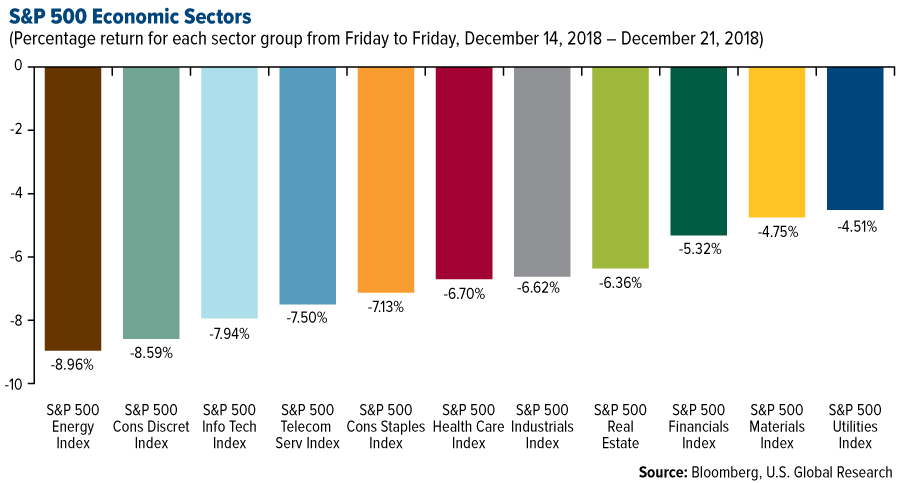

- Utilities was the best performing sector of the week, decreasing by 4.51 percent versus an overall decrease of 7.06 percent for the S&P 500.

- General Mills was the best performing stock for the year, increasing 3.83 percent.

- 2018 was a big year for initial public offerings (IPOs). A total of 191 companies went public in the U.S. this year, up 19.4 percent from the previous year.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 8.96 percent versus an overall decrease of 7.06 percent for the S&P 500.

- Perrigo was the worst performing stock for the week, falling 35.02 percent.

- Facebook continues to fall as the bad news keeps piling up. Shares of the social media giant fell more than 7 percent on Wednesday, wiping out $30 billion of market value, after it was sued by Washington, D.C. over its relationship with Cambridge Analytica. Facebook also acknowledged this week in a blog post that Netflix and Spotify had privileged access to user messages.

Opportunities

- Nike saw a big boost from digital sales. The sneaker giant beat on both the top and bottom lines, and said that its Nike brand saw sales jump 14 percent on a neutral-currency basis, driven largely by digital sales.

- AB InBev announced it is teaming up with Tilray to explore marijuana-infused drinks. The world's largest brewer and the Canadian cannabis producer agreed to form a partnership, investing up to $50 million each, to research nonalcoholic beverages containing THC and CBD.

- Oracle reported adjusted earnings of $0.80 a share on revenue of $9.56 billion, beating out expectations of $0.78 a share and $9.52 billion total revenue.

Threats

- The S&P 500 has fallen more than 7.8 percent this month and is on track for its worst December since 1931, when it lost about 15 percent during the chaos of the Great Depression.

- Globally rising interest rates combined with tensions over geopolitics and the trade war could mean the start of 2019 may look just as volatile and turbulent as this year – according to the Bank for International Settlements (BIS). The BIS quarterly review, released Sunday, is titled "Yet more bumps on the path to normal.”

- Malaysia filed criminal charges against Goldman Sachs over the 1MDB scandal. Malaysia has accused the bank and two of its former executives, Tim Leissner and Roger Ng Chong Hwa, as well as the former 1MDB employees Jasmine Loo Ai Swan and Low Taek Jho, of "grave violations of our securities laws" relating to its $6.5 billion sovereign wealth fund.

The Economy and Bond Market

Strengths

- The Conference Board’s Leading Economic Index (LEI) edged up 0.2 percent to 111.8 in November. “Despite the recent volatility in stock prices, the strengths among the leading indicators have been widespread. Solid GDP growth at about 2.8 percent should continue in early 2019. But the LEI suggests the economy is likely to moderate further in the second half of 2019,” said Ataman Ozyildirim, director of economic research at the Conference Board. The LEI has increased 2.2 percent over the past six months, slower than the 2.9 percent gain over the six months before that. However, strengths among leading indicators remain more widespread than weaknesses.

- Consumers increased spending again in November, suggesting that the U.S. economy is holding its momentum. Personal-consumption expenditures increased a seasonally adjusted 0.4 percent in November from the prior month, the Commerce Department said Friday. It was the ninth straight monthly increase in household outlays.

- Consumer sentiment remained at the same favorable levels in the December survey as it has recorded throughout the year, according to the latest University of Michigan Surveys of Consumers. The Sentiment Index averaged 98.4 in 2018, the best reading since 2000’s 107.6.

Weaknesses

- The Federal Reserve raised its key interest rate Wednesday for a fourth time this year, but it lowered its forecast to two hikes in 2019 amid the recent stock market selloff and uncertain growth prospects. "We have seen developments that may signal some softening," Fed Chairman Jerome Powell said. "In early 2018, we saw a rising trajectory for growth. Today, we see growth moderating ahead."

- Sales of previously owned U.S. homes lifted slightly in November from a month earlier, but they registered the largest annual decline in more than seven years. Sales in November decreased 7 percent from a year earlier, the largest year-to-year drop since a May 2011 decline that came after a surge of demand in the year-earlier period.

- The Empire State Manufacturing Index fell 12.4 points to 10.9 in December, the New York Fed said Monday. That’s the weakest level in 19 months. Economists had expected a reading of 21.

Opportunities

- U.S. solar and wind developers are rushing to invest in new projects to take advantage of renewable-energy subsidies. Wind credits are already being reduced, and an investment-tax credit that affects solar is slated to decrease in 2020. Bloomberg New Energy Finance (NEF) forecasts 173 gigawatts of clean-power capacity will be added through 2025, including 117 gigawatts of solar. Other factors driving the renewables boom include California’s mandate to switch to carbon-free power sources by 2045 and new renewables targets in states including Massachusetts and Connecticut.

- The Conference Board’s consumer confidence index comes out next Thursday. This week’s strength in the sentiment survey from the University of Michigan bodes well for the release.

- The last data item for the year will be the Chicago purchasing manager’s index (PMI) out on Friday. While it is expected to moderate somewhat, it remains at robust levels of activity.

Threats

- All eyes will be on the housing market next week as the S&P CoreLogic Case-Shiller 20-city home price index is due on Wednesday, followed by new home sales on Thursday and pending home sales on Friday. America’s housing industry has been showing some signs of weakness lately as higher borrowing costs have started to lower demand.

- President Donald Trump's trade war is already hitting pockets of middle America. The trade war will cost American taxpayers in the middle quintile of income earners $146 on average, a number expected to rise to $453 in a year if he goes ahead with his threatened tariffs, according to the Tax Foundation.

- The yield curve is the flattest it's been since 2007. The spread between the two-year and 10-year note yields is down to 11 basis points, the flattest since the second quarter of 2007.

Energy and Natural Resources Market

Strengths

- Iron ore was the best performing major commodity this week rising 8.2 percent. The commodity rose as stockpiles across ports in China declined amid restocking by steel mills.

- The best performing sector this week was the NYSE Arca Gold Miners Index. The index rose 1.8 percent after the spot price of gold broke above its 200-day moving average for the first time this year, attracting money flows into gold miner equities.

- The best performing stock for the week was OceanaGold Corp. The gold miner rose 10 percent, benefitting from the rise in gold prices and an announcement that it received preliminary approval for a mine life extension at one of its assets.

Weaknesses

- Crude oil was the worst performing commodity this week. The commodity dropped 11.5 percent after the U.S. Energy Information Administration increased its supply expectations for shale oil growth.

- The worst performing sector this week was the S&P 1500 Oil & Gas Exploration and Production Index. The index dropped 11.2 percent, to a 52-week low, tracking the decline in crude oil prices.

- The worst performing stock for the week was Westrock Co. The Atlanta-based packaging company dropped 16.7 percent to the lowest level this year after Bank of America lowered its recommendation on the stock citing weak channel checks data.

Opportunities

- Gold is heading for its best quarter since 2017 as equities decline. Investors who pushed equities to records this year are starting to seek haven in the asset they’d shunned: gold. The metal is heading gaining traction as economic headwinds including U.S.-China trade tensions weigh on stocks and fuel bets that the Federal Reserve will ease the pace of interest-rate increases.

- Japanese bank Nomura is bearish on the U.S. dollar. The bank notes that U.S. growth is already losing momentum, and even with a few more hikes, Fed policy rates would settle at their lowest level in history for the end of a hiking cycle. The punchline is that “U.S. yields are simply not high enough to make up for the U.S. growing twin deficits, and lack of foreign capital inflows,” concludes the report.

- Australia flagged a $122 billion rebound for commodities projects. Stronger prices, a brighter longer-term demand outlook and the rise of battery metals are laying the ground for a potential revival in mining and energy projects in Australia, according to the world’s top exporter of iron ore, alumina and coking coal. BHP Group and Rio Tinto Group, the world’s two largest miners, along with Fortescue Metals Group, have this year approved the development of new operations in Western Australia, highlighting confidence that the commodity sector may rebound.

Threats

- The U.S. Energy Information Administration said in a monthly drilling productivity report on Monday that production from seven key shale producing regions is set to rise to a record 8.2 million barrels a day in January from a month earlier. The projected 134,000 barrel-a-day increase from December is an acceleration from recent months and highlights the strength of U.S. production.

- The U.S. NAHB Housing Market Index declined to 56 points in December, down from 60 points the previous month, marking the lowest level since May 2015. In addition, the drop now constitutes the largest two month drop since October 2001, highlighting the negative momentum in a key end market for natural resources.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 1.5 percent. An improving geopolitical situation between the U.S. and Turkey boosted investors’ confidence. President Erdogan announced the delay of a planned offensive in Syria, and welcomed President Donald Trump’s decision to pull U.S. troops out of northeast Syria.

- The Hungarian forint was the best performing currency this week, gaining 95 basis points against the U.S. dollar. The central bank of Hungary left its main rate unchanged, at a record low 90 basis points, saying it sees cautions and gradual normalization that will depend on inflation outlook. Inflation is expected to reach 2.8 percent in 2018, below the bank’s target of 3 percent. Growth this year should stand at 4.7 percent and next year economic growth will slow down to 3.5 percent, according to the bank.

- Industrial was the best performing sector among eastern European markets this week.

Weaknesses

- Romania was the worst performing country this week, losing 19 percent. The Romanian finance minister announced fiscal measures to help the government lower its growing budget deficit, proposing taxes on banks, energy and telecomm companies. Similar reforms were introduced in Hungary and Poland, but Romania’s proposed taxes look elevated compared to CEE peers.

- The Russian ruble was the worst performing currency this week, losing 3.1 percent against the U.S. dollar. The ruble sold off with the price of Brent crude oil, which lost 11.5 percent in the past five days on worries over weaker demand due to a global slowdown.

- Energy was the worst performing sector among eastern European markets this week.

Opportunities

- The U.S. State Department approved the sale of Patriot air defense missiles to Turkey. Previously the U.S. refused to make the sell, which led Turkey to order Russian S400 missiles, exposing Turkey to potential U.S. sanctions. The Wall Street Journal reported that the U.S. military is preparing for a full withdrawal of its forces from Northeastern Syria, which should be also supportive for the local currency. Tension between the U.S. and Turkey has been the main diver of the Turkish lira depreciation in the third quarter of this year.

- Italy and the European Union (EU) reached a budget deal, ending months-long negotiations and avoiding sanctions for breaking an EU agreement. The Italian government has said that the agreement was achieved without making drastic changes to key budget proposals, such as the promise of a universal basic income and lowering the pension age. Next year’s initial budget had a spending deficit equal to 2.4 percent of gross domestic product, which was then lowered to 2.04 percent.

- Reuters reported that Greek lawmakers approved on Tuesday the country’s first post-bailout budget, which projects a high primary surplus next year and sees a pick-up in economic growth. The budget forecasts 2.5 percent GDP growth, compared to a projected 2.1 percent this year. Greece is also expected to generate a primary surplus, which excludes debt-servicing cost, of 3.6 percent of GDP next year.

Threats

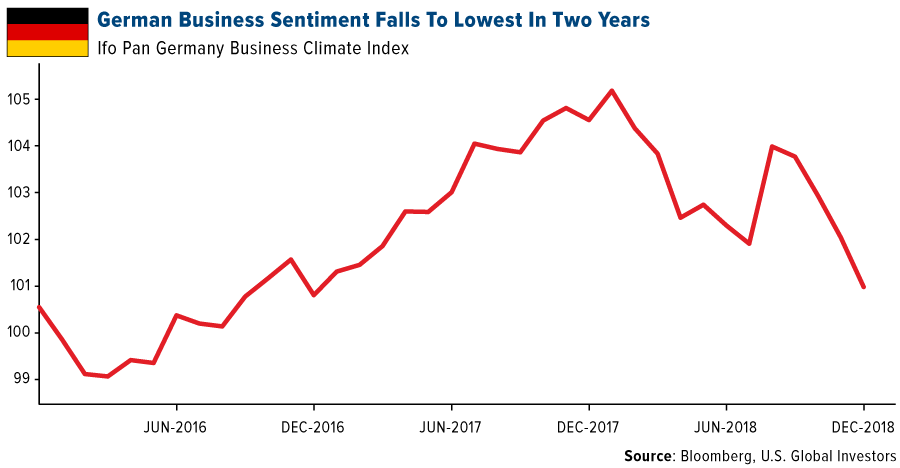

- The German business confidence index dropped to 101.0 points in December, down from 102.0 points in November, to the lowest level in more than two years. Worries are growing about the strength of the German economy due to Brexit negotiations and the U.S.-China trade war. The ECB last week announced the end of its 2.6 billion euro stimulus program, but rates should remain unchanged until the fall of the next year.

- Western European lenders mostly control the Romanian banking sector, and the banking tax proposed by the Romanian government will shift the burden of fiscal tightening from domestic to foreign companies. JPMorgan commented that Erste Bank, the biggest foreign bank in Romania, would face a 140 million euro charge, which is equal to 0.9 percent of group earnings, under the proposed banking tax. Austrian Raiffeisen Bank and Hungarian OPT bank are two other foreign banks that will be negatively affected by this new fiscal proposal in Romania.

- Emerging Europe, as measured by the MSCI Emerging Europe Index, declined more than 20 percent from its peak back in January, entering a bear market. Stocks trading on the Budapest exchange are the best performers year-to-date in dollar terms. Greece is the weakest link of Europe, losing almost 30 percent year-to-date.

China Region

Strengths

- What regional index finished in the green for the week? This guy: Malaysia’s Kuala Lumpur Composite Index, rising 50 basis points (though it did put in 52 week lows this week as well).

- Telecom cranked out a win for the week amid the otherwise red Hang Seng Composite Sectors. Telecom rose 28 basis points, the only sector to finish in the green for the week.

- Overseas remittances to the Philippines came in better than expected, rising 8.7 percent year-over-year, better than the 3.3 percent print analysts expected and better than the prior reading of 2.3 percent growth.

Weaknesses

- The Shanghai Composite tumbled 2.99 percent for the week, while the Hang Seng Composite Index fell 2.21 percent. Vietnam’s Ho Chi Minh Stock Index declined 4.16 percent for the week.

- Energy was the worst performing sector in the Hang Seng Composite Index, dropping by 7.61 percent for the week and accompanying crude oil amid its plummet lower this week.

- South Korea’s imports and exports numbers both came up short versus the prior month’s year-over-year readings. Imports clocked in at only a 2.2 percent rise, well below the last reading of 12.8 percent, while exports came in up 1.0 percent, down from 5.7 percent.

Opportunities

- China has offered up additional stimulus in 2019, promising more tax cuts and easier monetary policy, while continuing to open up the economy and seeking to advance trade talks with the United States.

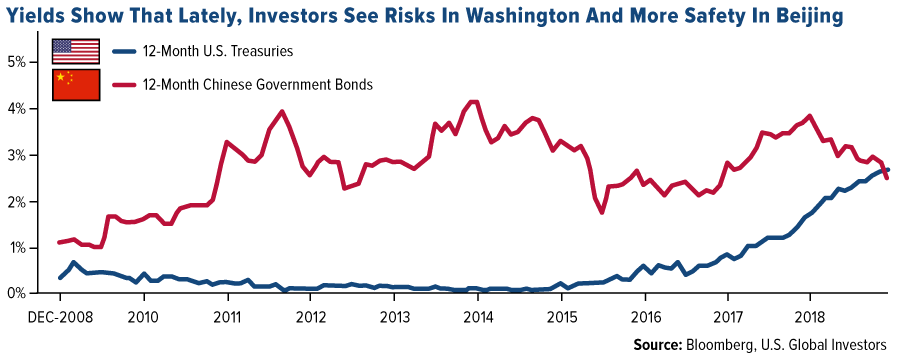

- An interesting chart put out by Bloomberg News last week under the title “Markets Conclude U.S. is Riskier Than China” was most intriguing. It demonstrates that since the Fed started raising interest rates in 2015, the gap between the two countries’ Treasury bills first narrowed and then reversed, with the U.S. now offering higher yields than China on one-year paper. The chart is now aging slightly but still interesting.

- Valuations remain interesting around the region and become even more so as markets sell off…

Threats

- While trade talks are supposedly still on schedule for January between the U.S. and China, and there remain definite risks to a trade war (or trade truce, at the moment), which may continue to cast dark clouds over the outlook until we get more clarity and certainty.

- Goldman Sachs may now be looking at possible charges coming from Singapore as well related to the ongoing fallout from the Malaysian 1MDB scandal.

- While the Philippine and Indonesian central banks stood pat most recently, the Fed did not this week, and investors will continue to watch monetary policy, economic outlook and inflation concerns for these two countries in particular.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended December 21 was ERC20, up 196.44 percent.

- Cryptocurrencies gained back a little of the ground lost in the past year, reports Seeking Alpha. Bitcoin rose 11 percent at the start of the week, reaching $3,600 in the afternoon on Monday while Ripple jumped 16 percent and Ethereum gained 14 percent. By Wednesday, bitcoin’s performance had jumped 22 percent, to a high of $3,929.10, reports CoinDesk.

- A Twitter poll conducted by the Bank of England found that a whopping 72 percent of respondents preferred digital currencies as a Christmas gift. “If you receive money as a gift for Christmas,” the poll asked, “what’s your favourite way to get it?” Of the 9,694 people who have taken the poll as of this writing, nearly three quarters chose “digital currency.” Twenty percent said “cash”; 6 percent, “bank transfer”; 2 percent, “gift voucher.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended December 21 was Twinkle, down 75.48 percent.

- Cryptocurrency trading is dwindling, writes Bloomberg, as interest among institutional players ebbs. According to analysts with JPMorgan Chase, there appears to be falling open interest and hashrates, signaling the cryptocurrency market is freezing over. “Participation by financial institutions in Bitcoin trading appears to be fading,” analyst Nikolaos Panigirtzolou wrote in a research note. “Key flow metrics have downshifted dramatically,” including in futures markets and in average volumes.

- Three top executives at UPbit, one of South Korea’s leading cryptocurrency exchanges, were formally indicted on charges of fraud. CoinDesk reports that the executives are alleged to have made fraudulent transactions in order to artificially inflate trading volumes and attract more prospective customers to the exchange.

Opportunities

- Despite what some call a “horrifying” year for cryptocurrencies, there are still plenty of industry experts that have a positive outlook on the sector. One of those individuals is Greg Tusar, former global head of electronic trading at Goldman Sachs Group and current chief technology officer and co-founder of Tagomi Holdings. “It feels like being at the early days of trading equities electronically,” Tusar said. “It’s early stage, there’s lots of opportunity to build great businesses and have impact.”

- HTC might not have the same presence in the smartphone market as it once did, reports AndroidCentral, but the company has a few different plans for 2019, one of which includes blockchain. HTC President Darren Chen says the company will be focusing on flagship and mid-range phones in the New Year and its other smartphone focus will be on its recent efforts with blockchain devices. DigiTimes reports that HTC is “mapping new strategy and business model for further promotion of blockchain smartphones,” the article continues.

- Facebook is reportedly developing a cryptocurrency transfer feature through its messaging app WhatsApp, Bloomberg reports. According to the article, Facebook “is developing a stablecoin—a type of digital currency pegged to the U.S. dollar—to minimize volatility.” Western Union could also be ready to involve itself with digital curr3encies. In a video interview with Reuters, Western Union President Odilon Almeida said that the company “is ready today to adopt any kind of currency. We already operate with 130 currencies. If we one day feel like it’s the right strategy to introduce cryptocurrencies to our platform, technology-wise it’s just one more currency.”

Threats

- Canadian gaming billionaire Calvin Ayre, once a strong supporter of cryptos, has turned alarmingly bearish on bitcoin. In an interview with Express.co.uk, Ayre said he believes bitcoin’s price is deliberately being pushed down and will eventually crash to zero in 2019. The coin “has no utility” and “does not do anything,” he added.

- One reason why many big fund managers in Asia are hesitant to invest in cryptocurrencies? Crypto exchanges are finding it difficult to insure themselves against the risk of hacks and thefts, reports Reuters. “Most institutionally minded crypto firms want to buy proper insurance,” says PwC’s Henri Arslanian, but “getting such coverage is almost impossible despite their best efforts.”

- JPMorgan believes that this year’s plunge in crypto prices have scared away institutional investors. “Participation by financial institutions in bitcoin trading appears to be fading,” the bank’s analysts write. “Key flow metrics have downshifted dramatically.” What will it take to raise sentiment?

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All