The Late Cycle Lament: The Dual Economy, Minsky Moments, and Other Concerns

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsExecutive Summary

Overoptimism and overconfidence are two well-known psychological traits of our species. They are particularly dangerous in the late stages of an economic cycle where these terrible twins result in investors overestimating return and underestimating risk – a potentially lethal combination of errors.

Far from the sanguine consensus of the current state of health of the U.S. economy, in this paper I demonstrate that this is the slowest and weakest recovery in post war history. Whilst GDP growth has been poor, labour productivity growth has been worse, and real wage growth worst of all. The headline data obscure even more worrying trends. Effectively, the U.S. is witnessing the rise of the “dual economy” – where productivity growth is reasonable in some sectors, and totally absent in others. Even in the sectors with good productivity growth, real wages are lagging (wage suppression is occurring). All the employment growth we are seeing is coming from the low productivity sectors. On top of this, the paltry gains in income that are being made are all going to the top 10%. This is not what a booming economy should feel like.

Real earnings growth in the corporate sector has been below the rate of GDP growth even after the significant boost from the financial engineering known as buybacks. So investors have little to celebrate. Indeed, a breathtaking 25% to 30% of firms in the Russell 3000 are actually loss-making! Yet the stock market remains well bid. In large part, this bid is sourced from the buybacks (and mergers) from USA Inc. itself. However, individual investors have returned to the “party” – never a good sign. Other portents of late-cycle capitulation include global fund managers throwing in the towel and buying into U.S. equities.

The corporate bid is really a massive debt for equity swap, with firms issuing massive amounts of corporate bonds (very low quality debt at that), and effectively leveraging themselves up. This creates a systemic vulnerability, and is potentially a Minsky Moment in the making. The listed sector has been at the vanguard (or perhaps better described as the forlorn hope) of this movement.

All of this occurs against a backdrop of an extremely expensive U.S. equity market, which is increasingly looking like Wile. E. Coyote – the hapless adversary of Roadrunner – having run off the edge of a cliff only to realise the ground is no longer below his feet. Tragically, it seems valuation is doomed to suffer Cassandra’s curse at a time when telling the truth is never believed.

In order to believe that U.S. equities are going to generate a “normal” return from these levels, you have to believe some quite extraordinary things. Perhaps you believe that P/Es are going to soar to levels not even seen at the height of the TMT bubble; or perhaps you believe that profitability is going to rise (from already extended levels) so that every firm in the U.S. looks like a FAANG stock; or perhaps you believe that growth is simply going to reach unprecedented levels. We, however, are not so prone to flights of fancy that require multi standard deviation outcomes. Unless you believe one of these extreme scenarios, you should be skeptical about the ability of the U.S. market to continue its outstanding performance. Ask yourself how much exposure you have to the U.S. stock market. Then ask yourself what is the minimum amount you could own. We at GMO own essentially zero in our unconstrained portfolios, but then again we are used to career risk and would rather run it than allocate to such an expensive and risky asset.

Let me start by asking you three simple questions. Are you above average as a driver? Are you above average at your job? And finally, are you above average when you make love?

If you are like the vast majority of people, chances are you will have answered these questions in the affirmative. Of course, the questions are designed to illustrate one of the most common human psychological traits – overoptimism. Indeed, it is perfectly possible that overoptimism provided an evolutionary edge: the pessimistic caveman probably never bothered going out to hunt woolly mammoths. George Bernard Shaw opined that both optimism and pessimism were necessary for human society…the optimist invents the aeroplane, the pessimist the parachute.

However, clinical studies have found one group of people who perceive reality the way it truly is. These are the clinically depressed, which is of course why they are clinically depressed! This leaves us with an unenviable choice – either be happy and deluded, or sad and accurate. Personally, I am clinically depressed at work, and then happily deluded when I am home in the evening.

Investors (unsurprisingly) are no different than other people. They too tend to be overoptimistic. Indeed, if investors had an anthem it would almost certainly be “Always look on the bright side of Life.”1 As I was reading the wonderful Eric Idle’s autobiography recently, I discovered this phrase has been around since at least the times of Samuel Taylor Coleridge! This tendency to optimism is particularly pronounced during the late stage of a cycle. When coupled with another all too common psychological trait of overconfidence, a dangerous double whammy of behaviour is born: investors end up overestimating returns and underestimating risk.

Take for example Exhibit 1. It shows the long-term EPS expectations from consensus bottom-up analysts. It appears that analysts are extremely optimistic about long-term growth prospects. Indeed, to borrow an expression from Toy Story’s Buzz Light Year, they appear to believe earnings can grow “To infinity and beyond.” Their expectations have now soared to levels last seen during the tech bubble of the late 1990s.

Now, I spent my career prior to joining GMO working alongside bottom-up analysts. I have a reasonable knowledge of many of their working practises. When coming up with a price target, they define a buy rating as, say, 20% above the current market price. They then need to build a discounted cash flow model to justify this rating. Because most of the analysts are spoon fed the short-term outlook from company managements, they don’t have many degrees of freedom in their model to twiddle with to get their desired outcome, so they end up jacking up long-term earnings growth. So, in some ways, the picture in Exhibit 1 is a reflection of market prices action.

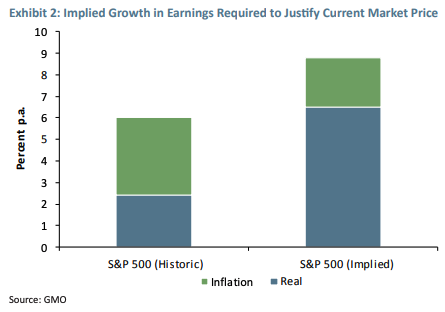

You might well say that everyone knows that analysts are a deluded bunch and no one believes them. So perhaps alternatively we should look to reverse engineer the problem to determine what we need to believe in order to arrive at today’s fair market value. There are many possible ways to do this. For instance, in Exhibit 2 we show the results of using a simple residual income model to estimate the earnings growth we would need to see over the next decade in order to justify the current price level of the market.

Alternatively, we could use GMO’s 7-year asset class forecast framework and ask what you, the investor, would need to believe in order to generate 5.7% real returns (our estimate as to fair value). As I’m sure you know, when we build forecasts we break them down into building blocks. For equities these are P/E, return on capital, yield, and growth. We regress these components from whatever their starting levels are, back towards what we think of as normal. However, we can also ask, what would need to happen to each component in order to reach 5.7% (while allowing the other components to still return to normal).

Historically, the S&P 500 has generated around 6% nominal earnings growth over the long term. Twothirds of this has been inflation, leaving real growth at around 2%. To make the current market fair value, you would need to believe that the S&P 500 is capable of generating 9% each and every year for a decade. The market believes inflation is going to be around 2% annually (based on the difference in yields between 10-year nominal bonds and 10-year inflation protected bonds [TIPS]). Thus, the implied real growth rate is a jaw-dropping 7% p.a…more than three times the historical average.

Let’s start with P/E. The long-run historical average P/E has been 14.5x. The P/E on the S&P 500 today stands at 24x. In order to achieve a real return of 5.7% p.a. over the course of the next 7 years, you need to believe that P/E is going to rise to 32x. This is a higher P/E than recorded at the height of the tech bubble, and represents a 3-standard-deviation event.

If you prefer to argue that return on capital (ROC) is going to be the mechanism for generating 5.7% real, then you need to believe that ROC is going to rise from its current 8% to a breathtaking 11%. As a point of reference, the historical average ROC is 6%. Incidentally, the FAANG2 stocks have an ROC of roughly 11%. Holding this view is akin to believing that we will have a nation of FAANGs. Getting to 11% represents a 5-standard-deviation event.

Finally, perhaps you think yield and growth will come to the rescue. Historically, they have delivered a combined 6% real p.a., comprising 4% yield and 2% real growth. You would need to believe that these elements could generate 16% in order to make that 5.7% real return. Starting with a yield of around 1.4%, this implies a 14.6% real growth. This would be a 6-standard-deviation occurrence.

To say you would need to be optimistic to believe pretty much any of these three things would make me a master of understatement.

So where does all this optimism stem from? Well, it isn’t hard to see if you read the headlines. Take for example this gem from Fox News, “Trumps says U.S. economic growth nears 5%...time to celebrate”; or “This is what a booming economy feels like” from the Chicago Tribune; or even “Economy hits a high note and Trump takes a bow.” Indeed a recent conference held by the National Association of Business Economists (an oxymoron if ever one existed) had a session entitled “Is the business cycle dead?” Whenever you hear that, you should head for the hills.

How does this unbridled economic enthusiasm fare when faced with a reality check? Sadly, not well. Exhibit 3 shows the flight paths of all post war economic expansions in terms of GDP. The current expansion is the slowest and weakest economic recovery witnessed in the entire post war period.

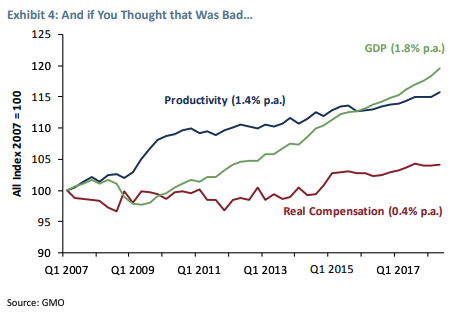

Unfortunately, the bad news doesn’t stop there. Exhibit 4 shows that productivity has been even weaker than GDP growth and, most depressingly of all, real wages have essentially been flat for over a decade! This is not what a booming economy feels like…particularly from a worker’s perspective.

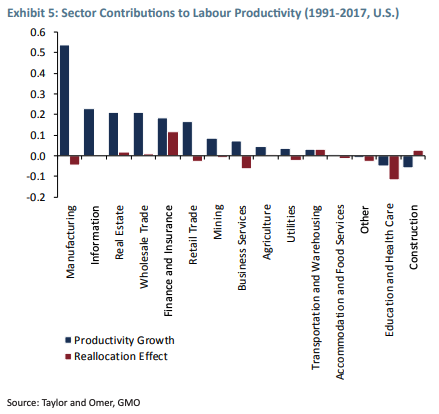

When we break the productivity data down,3 we can see which sectors have been driving the productivity gains and which have not.4 As Exhibit 5 shows, manufacturing has been by far and away the biggest single driver of productivity. Others have done pretty well, such as information and wholesale trade. At the other end of the spectrum, we see sectors such as transportation, accommodation, education, and health care. These sectors have both low levels of productivity and low growth rates of productivity.5

In fact, we appear to have witnessed the birth of what has been described as a dual economy.6 In essence, we have one group of sectors with reasonable productivity (both levels and growth), and a laggard group with no productivity growth. Wages in both groups are disappointing. In the high productivity sectors, wages have grown significantly more slowly than productivity (aka wage suppression). In the laggard group, zero productivity growth has gone hand in hand with zero real wage growth.

Whenever labour productivity outstrips real wages, the result is a falling share of the GDP pie going to labour. As Exhibit 7 illustrates, a declining labour share of income has been seen across a large number of sectors, although manufacturing really stands out once again.7

It is worth noting that employment has become increasingly dominated by the laggard sectors with their accompanying zero real wage growth. In 1990, the low productivity sectors accounted for around 46% of private sector employment; today they account for over 60% of all employment. So, the employment growth we have seen has been largely concentrated in zero real wage growth areas.

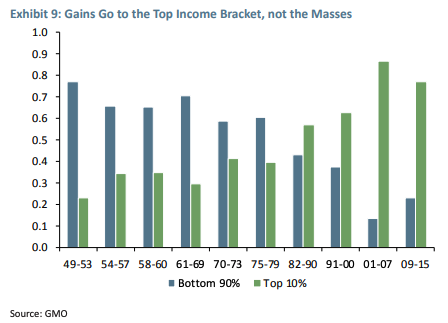

In addition, the economic growth we have seen has been increasingly captured by a very small minority of people. Exhibit 9 shows the share of income growth during expansions that is received by the bottom 90% and top 10% of households. It used to be the case that on average around 60% to 70% of the income gain was seen in the bottom 90%. However, a clear shift is visible in the Reagan years and after, when the top 10% started to capture the gains. In the last two expansions they have received over 80% of the income gains.

This all paints a very different picture from the headline hype that we started with. We have an increasingly fissured economy with low growth, lower productivity, and even lower real wage growth. An economy characterised starkly by growing differences between the haves and have-nots.

You may quite rightly point out that this is all about economics and that, while no doubt a concern, we as investors are really focused upon earnings, not GDP or productivity per se. So let’s switch gears and look at earnings. Exhibit 10 shows the by now familiar low GDP growth, but adds both real EPS and real aggregate earnings to the picture. It transpires that far from exceeding the poor performance of GDP, real earnings have actually undergrown GDP! Aggregate real earnings have delivered just 0.8% p.a. since 2007, and real EPS has delivered 1.2% p.a. since 2007. The difference between these two is, of course, the impact of share buybacks. So we can say that around 40% of EPS growth witnessed since 2007 has been the result of buybacks.

As if this wasn’t bad enough, when you dig down into the market you will find that a staggering 25% to 30% of firms are actually making a loss! There is a school of thought that argues this is all the artefact of the “death of accounting.” This line of thinking effectively argues that GAAP is no longer a good standard for understanding the nature of a business. Now, I have some sympathy with this view, but I wanted to see if it was actually driving this finding of so many loss-making firms. My colleague, Simon Harris, was kind enough to run the data for me based on this concept of economic earnings. Basically, it seeks to amortise rather than expense such items as R&D and advertising, amongst other adjustments. However, as Exhibit 11 shows, it really doesn’t matter which version of earnings you use, the conclusion you reach is still the same: one in four companies is making a loss.

Not that investors seem to allow losses to dampen their enthusiasm. Some 83% of IPOs this year have come to market with negative EPS, a higher percentage than that seen even at the height of the tech bubble.

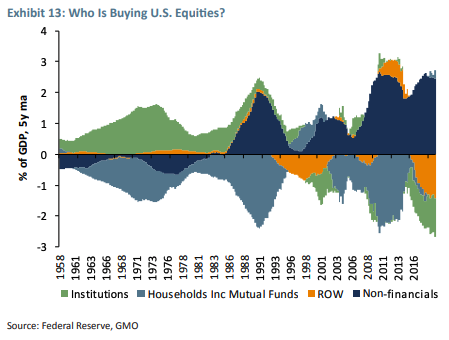

All of this raises the question: who is buying U.S. equities? Exhibit 13 reveals that the most stalwart buyer without a doubt has been USA Inc. itself. U.S. companies have been the largest buyers of U.S. equities for many years now (through a combination of M&A and buybacks). They remain the largest buyers by a large margin.

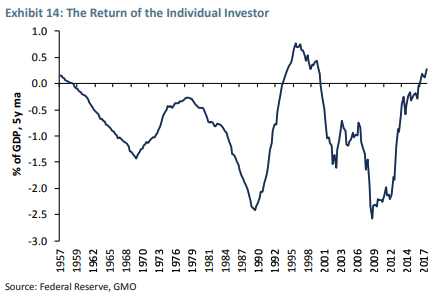

However, another group has recently returned to the fray. It is a little hard to spot them in Exhibit 13, so I have separated them out in Exhibit 14. The individual investor has returned as a net buyer of U.S. equities for the first time since the late 1990s! Traditionally, individual investors have been net sellers of equities over the long term. However, as you can clearly see, there are periods when they become net buyers…most notably during the tech bubble and today. Not the best market timers, perhaps.

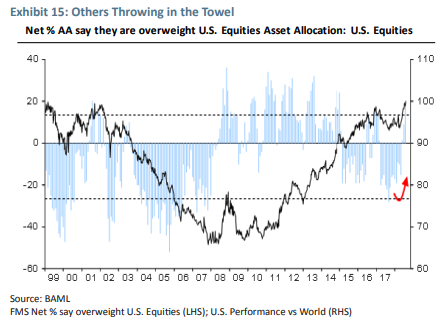

They are not alone in throwing in the towel after missing the run-up in the U.S. market. The BAML survey of global fund managers showed that they capitulated in September. Having been underweight the U.S. for a prolonged period (and having suffered a pain that we can relate to all too well), they performed a volte face, not only switching their position from negative to positive, but actually saying that the U.S. was the most attractive market of all!

Having highlighted these ominous portents, let us return to the main buyer of U.S. equities, USA Inc. This group has been engaged in a massive debt for equity swap – issuing enormous amounts of debt and buying back its own shares or purchasing other companies. Now it may be perfectly rational for each individual company to engage in this pursuit, issuing bonds at low interest rates and buying back their own equity. Of course, this raises leverage. And in aggregate it may create a fallacy of composition. What is good for each individual company is not necessarily good for every company as a whole.

Rising leverage creates a systemic fragility. It appears that everyone has forgotten about Minsky once more. Minsky was the creator of the financial instability hypothesis. Simply put, this states that stability begets instability. The quieter and safer the world appears, the more one is tempted to take on “risk” because extrapolation says there is no risk, and hence a free lunch exists. By taking on this risk, people sow the seeds of their own destruction. All the leverage makes the system more vulnerable, more fragile, and ensures that the outcome will be significantly worse than would otherwise have been the case.

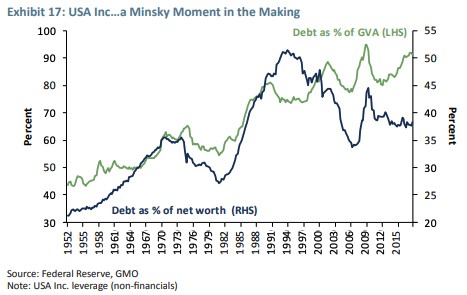

Exhibit 17 shows two ways of measuring the leverage of USA Inc. My preferred measure is the ratio of debt to gross value added (GVA), as this is akin to debt to EBITDA. It shows that we are once again approaching the levels of debt we saw in 2007. The other measure is debt to net worth, a frequently cited though, in my humble opinion, a pretty useless indicator. The problem with this measure is the denominator. If we had been looking at this measure in 2007 we would have concluded that we were well past the peak of vulnerability. It was only after markets collapsed that this measure rose (as net worth obviously fell).

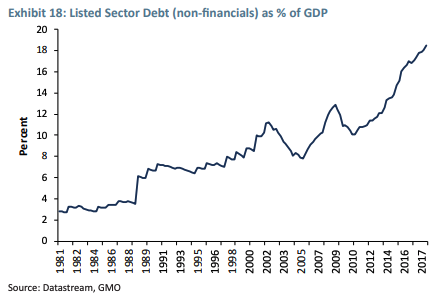

The listed sector is particularly vulnerable in this cycle as it has seen far faster growth in debt than the total of USA Inc. According to the Fed, corporate debt has been growing at around 4% p.a. since 2007. However, in the listed sector it has been growing at approximately 10% p.a. The stock of listed sector debt now stands at 20% of GDP, far above the level reached in 2007 (see Exhibit 18). This should obviously be of concern for equity holders as well as debt holders, because debt is a senior claim in the capital structure to equity.

We aren’t the only ones to voice concerns in this realm. The Bank of International Settlements (BIS) (the central bankers’ central bank) has also noted similar concerns (see Exhibit 19). It has shown the number of “Zombie” firms (defined as firms aged at least 10 years old with an EBIT to net interest expense below 1) has soared. BIS also notes the general drift down in corporate debt ratings over time. Indeed, today over half of the total stock of U.S. corporate debt is to be found in the lowest possible rating for investment grade bonds.

A similar concern about deteriorating credit quality can be seen in the high yield market as well. Moody’s tracks each high yield bond and gives it a score ranging from 1 to 5 in terms of the degree of covenant protection that it offers investors. The highest degree of protection is 1, and 5 is the lowest. Anything below 4.2 is defined as having the weakest level of protection. As Exhibit 20 shows, pretty much all the debt issued since 2014 has fallen into this weakest level of protection.

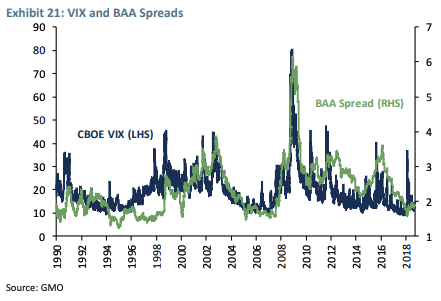

So we have massive amounts of debt issued, at very low quality.8 Surely investors are aware of this, and hence price bonds to reflect these kinds of risk. Of course not. Instead, corporate bond spreads continue to broadly follow equity volatility.9 But this does highlight that corporate bond investors are inherently short volatility (see Exhibit 21).

Corporate bond investors are far from alone in this position. Indeed, perhaps the investment world’s favourite strategy is to be short volatility. There also seem to be endless ways for investors to be able to get themselves short volatility (often without actually realising it). These range from the obvious selling of volatility itself, to activities such as following momentum strategies, or using a VAR-based risk management approach. They all share one common feature: you are forced to buy when prices rise and sell when they fall…the exact opposite of any value-based philosophy.

To pour petrol on an already raging fire, this is taking place against the backdrop of the second (or possibly third, depending upon the measure and the exact level of the S&P today) most expensive equity market in history!

The Shiller P/E currently stands at a nosebleed-inducing 30x, second only to the levels reached during the insanity of the tech bubble. Now, many people tend to get their knickers in a twist when it comes to the Shiller P/E. They bemoan the vulnerability to shifts in payout or the “fatal flaw” of including a bad year like 2009. However this is all much ado about nothing. Exhibit 22 shows an alternative measure, which I call the Hussman P/E, after John Hussman, the first person I have ever come across using this variant. The idea, like so many of the best ideas, is a simple one: compare the current price to the peak level of earnings seen. This has the advantage that 2009 is clearly a non-issue. However, the conclusion reached is the same as the Shiller P/E.

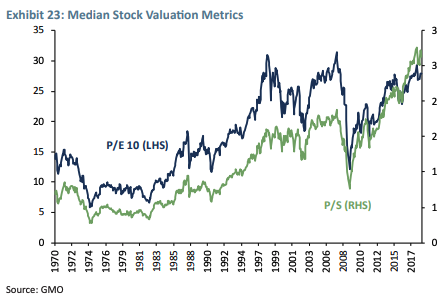

Similar conclusions are reached if you prefer to look at median valuations, rather than aggregate versions. Exhibit 23 shows the median price to sales and the median Shiller P/E. In both cases, exceptionally elevated levels of valuation are obvious to even the most cursory of glances. The median price to sales ratio has never been higher – even at the height of the tech bubble (thanks to the bifurcation of the market into some extremely expensive tech, media, and telecoms stocks, and a collection of old brick and mortar value stocks).

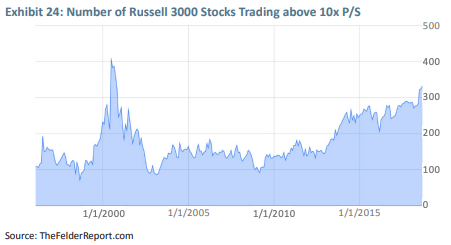

My colleague, Rick Friedman, sent me a chart that I could not resist including as Exhibit 24. (Yes, I’m a sucker for a good dose of confirmatory bias any day.) It shows the number of stocks in the Russell 3000 that currently trade at more than 10x price to sales. Once again we stand at levels not seen since the dot com era. Why is 10x P/S so interesting…well it reminds me of one my favourite quotations on the insanity of valuations. This one comes from Scott McNealy, the then CEO of Sun Microsystems:

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

One can’t help but think that should a bad outcome prevail, once again many an investor will be left with those words “What were you thinking?” ringing in their ears.

All of the above leaves me viewing the U.S. market increasingly as the hapless Wile E. Coyote in the everamusing Roadrunner cartoons, running in thin air only to eventually look down, realise his error, and plunge earthbound.

Now, of course, valuation is an excellent guide to long-term returns, and a terrible guide to short-term returns. This means that in the short term there is observational equivalence between being early and being wrong. I am regularly told either that valuation is irrelevant (or my favoured measures are irrelevant), or asked what the catalyst for a decline would be.

As I have confessed on prior occasions, I seem to be afflicted by a rare form of Tourette Syndrome, where I am compelled to tell the truth, and so I reply that I have no idea what the catalyst will be. Indeed, think back to the tech bubble of the late 1990s (or any other previous bubble for that matter). Can anyone tell me the catalyst for the market having a Wile E. Coyote realisation? I can’t, even with the benefit of 18 years of 20/20 hindsight.

In many ways, valuation seems to suffer Cassandra’s curse. For those who may have forgotten the tale, Cassandra was a priestess in the temple of Apollo. Apollo himself took a shine to Cassandra and decided to woo her, or more precisely to seduce her. In pursuit of his fancy, Apollo granted Cassandra the gift of prophecy in an attempt to win her over. However, Cassandra was a very chaste priestess and spurned Apollo’s advances. Being a typical capricious and vengeful God, Apollo didn’t handle rejection well, and cursed Cassandra. Rather than rescind his gift of prophecy, he ensured that Cassandra’s prophecies, whilst true, would never be believed. Valuation suffers a similar curse…just when it is most informative, it is least believed.

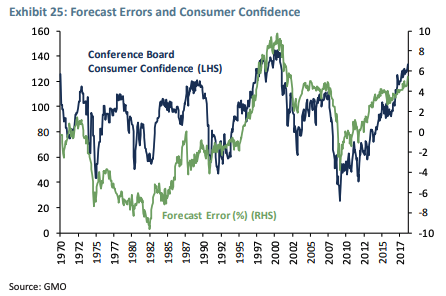

In the Greenspan/Bernanke/Yellen tenure at the helm of the Fed, there had been a close correlation between measures of cyclicality and the scale for the forecast error.10 For instance, Exhibit 25 shows the forecast error and the Conference Board’s Consumer Confidence measure.

So, standing in late 2008 (the last point for our forecast error because we are looking out 10 years), such a model thought the U.S. stock market would generate around 6% in real terms p.a. over the next decade. The actual outturn was 10% p.a., representing a forecast error of some 4%. But unless you believe the good times are set to continue ad infinitum, this error seems unlikely to persist as does the degree of optimism expressed by consumers (already hard to reconcile with the near zero real wage growth we showed above). Indeed, both the forecast error and consumer confidence display mean reversion.

As confessed above, I don’t know what the catalyst for a market downturn will be, nor do I know the path we will take. What I do know is that when things are priced for perfection they: 1) rarely turn out that way; and 2) usually change significantly to reflect “reality.”

Much of the material I have covered here is known. Yet should a market decline of substantial proportions emerge, we will almost certainly be told it was a black swan – something that no one could have known or predicted. However, it is important to remember that black swans are often a matter of perspective. Think about turkeys in the run up to Thanksgiving. Every day a very benign dictator arrives, feeds them, checks their water, and ensures they are safe and warm. Then a few weeks before Thanksgiving, the same dictator goes on what can only be described as a murderous turkey genocide. This is a black swan from the perspective of the turkeys, but anything but to the farmer.

In fact, most black swans in finance/investing are really “predictable surprises” to borrow Max Bazerman’s term (yes, I know that sounds like an oxymoron). Predictable surprises are characterised by three features: 1) at least some people are aware of them; 2) they get worse over time; and 3) they eventually explode into a crisis.

You might ponder why people are so bad at spotting predictable surprises. It turns out there is a plethora of psychological and institutional impediments. Two we have already met at the outset of this essay, overoptimism and overconfidence. They are aided by myopia – an overt focus on the short term – born of the institutional imperative to perform at all-time horizons; or its cousin, the relative performance derby; or simply a function of the human brain. Motivated reasoning plays a part as well. As Warren Buffett put it, “Never ask a barber if you need a haircut.” It is hard to get many finance professionals to think about the possibility of a crash when their employment and income depends upon that event not happening. Also noteworthy is inattention blindness…put simply, we just don’t expect to see the things we aren’t looking for. The classic example comes from Daniel Simon’s lab, where he shows a clip of two small teams passing a basketball between themselves. Participants are asked to count the number of passes by the players wearing black. Many people watching this video get so involved in counting they don’t spot a person in a gorilla suit enter the picture, beat its chest, and walk off.

Having read this entire essay, perhaps you believe one of the conditions I laid out earlier (in terms of P/E, ROC, or growth). If not, you are probably skeptical about the ability of the U.S. market to continue its outstanding performance. Ask yourself how much exposure you have to the U.S. stock market. Then ask yourself what is the minimum amount you could own. We at GMO own essentially zero in our unconstrained portfolios, but then again we are used to career risk and would rather run it than allocate to such an expensive asset.

James Montier. Mr. Montier is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2009, he was co-head of Global Strategy at Société Générale. Mr. Montier is the author of several books including “Behavioural Investing: A Practitioner’s Guide to Applying Behavioural Finance”; “Value Investing: Tools and Techniques for Intelligent Investment”; and “The Little Book of Behavioural Investing.” Mr. Montier is a visiting fellow at the University of Durham and a fellow of the Royal Society of Arts. He holds a B.A. in Economics from Portsmouth University and an M.Sc. in Economics from Warwick University

Disclaimer: The views expressed are the views of James Montier through the period ending December 2018, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2018 by GMO LLC. All rights reserved.

1 https://www.youtube.com/watch?v=SJUhlRoBL8M (from Monty Python’s “Life of Brian”)

2 Facebook, Amazon, Apple, Netflix, and Google (now Alphabet, Inc.).

3 Here we are following excellent work of Taylor and Omer (2018), “Where do profits and jobs come from? Employment and distribution in the U.S. economy,” INET working paper, May 2018; Taylor and Omer (2018), “Race to the bottom: low productivity, market power and lagging wages,” INET working paper, August 2018 (https://www.ineteconomics.org/ research/research-papers/where-do-profits-and-jobs-come-from-employment-and-distribution-in-the-us-economy; https://www.ineteconomics.org/research/research-papers/race-to-the-bottom-low-productivity-market-power-andlagging-wages). We are very grateful to Taylor and Omer for many helpful discussions.

4 This is all joint work with my colleague Philip Pilkington.

5 We will explore these issues in more detail in a forthcoming white paper.

6 See Servaas Storm (May 2017), “The New Normal: Demand, Secular Stagnation, and the Vanishing Middle Class,” International Journal of Political Economy, 46:4, 169-210 (https://doi.org/10.1080/08911916.2017.1407742).

7 Here we follow the work of Mendieta-Munoz, Rada, and Arnim (2018), “Sectoral dynamics of income distribution in the U.S. economy,” University of Utah working paper. We are very grateful to Codrina Rada for many helpful conversations. We will be exploring the impact of this finding on our work on profits in a forthcoming white paper.

8 See Matt Kadnar’s forthcoming paper for more on this topic.

9 Not an accident, given Merton (or KMV) models require asset volatility as an input. Because this is unobservable, equity volatility is substituted instead.

10 The forecast error shown here is a simple value-based forecast using the Shiller P/E and regressing it towards 17 over 10 years, adding constants to reflect yield and growth. The forecast horizon is 10 years. So, the forecast error reflects the degree to which realized returns were higher or lower than the forecast.

© GMO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All