A tightening of financial conditions, led by US Federal Reserve (Fed) rate hikes and an appreciating US dollar, have pressured emerging market (EM) assets so far this year. However, Invesco Fixed Income believes that concern over a generalized “crisis” in EM external debt (and external vulnerability) is largely unwarranted. That said, structural impediments are likely to limit EM growth over the medium term – particularly in the context of a stronger US dollar. We believe there is selective value in EM right now in markets that have been unjustifiably impacted by tightening US dollar funding conditions.

What has caused the EM volatility?

We believe recent volatility in EMs has been caused by a combination of idiosyncratic and exogenous (external) factors. The primary external factor has been a tightening in US financial conditions triggered by a rise in real interest rates and – importantly – the US dollar. This effective tightening in US dollar funding conditions has led to concerns about the ability of many EMs to fund external liabilities coming due.

Arguably, this concern was only exacerbated in countries with idiosyncratic issues, namely Argentina and Turkey. These economies were perceived to have been running policy “too hot” and in the process, generating external imbalances – that is, widening current account deficits and large external funding requirements. These imbalances ultimately require future financing, either through capital flows or via a drawdown in foreign exchange reserves. Both countries are perceived to have been externally vulnerable, given already low foreign exchange reserve coverage of external funding needs.

EM stress and rising external debt

It is true that external debt levels in EMs have climbed over the past decade. However, based on Bank for International Settlements data, most of this rise has been in China, and to a lesser extent, Mexico. In other countries, the rise in external debt has been more modest. Most of this rise comes from the private, corporate sector. Measures of capacity to repay have worsened since 2008, but for most countries they remain at comfortable levels. Additionally, EM external assets have grown faster than external debt. In aggregate, current liquid EM foreign exchange reserves (excluding gold) can pay down all EM external debt.

Important considerations

However, there are important caveats to bear in mind. First, foreign exchange assets are concentrated in some countries and scarce in others. For instance, based on our analysis, all else equal China’s reserves can cover its external funding needs over the next 12 months several times over, while Argentina and Turkey lack sufficient reserves to cover their needs from now until the end of 2019 (though Argentina’s recent deal with the International Monetary Fund secures their access to external funds so long as the program holds). Second, external assets are concentrated in the public sector and external liabilities in the private sector. Transferring external assets to the private sector can pose challenges that typically manifest via the exchange rate. Central banks can mitigate potential pressure on the domestic currency via various mechanisms, including foreign exchange swaps.

We see domestic debt as the true source of EM vulnerability

Domestic leverage in EMs has increased over the past decade, and more recently, government debt has also increased with fiscal expansion. A domestic debt overhang will likely restrain growth, absent a resurgence in productivity that boosts income and repayment capacity. The upturn in EM growth through the third quarter of 2017 reduced domestic debt and debt-servicing ratios, but this dynamic may not persist if EM countries fail to address underlying competitiveness concerns.

Why does this matter? As monetary policy normalization leads to rising developed market interest rates, growth differentials between EM and developed markets become more important determinants of capital and portfolio flows. The higher the growth differential in favor of EMs, the higher the capital inflows (and asset market support) to EMs, and vice versa. This dynamic becomes more problematic if global financial conditions continue to tighten, particularly via the US dollar.

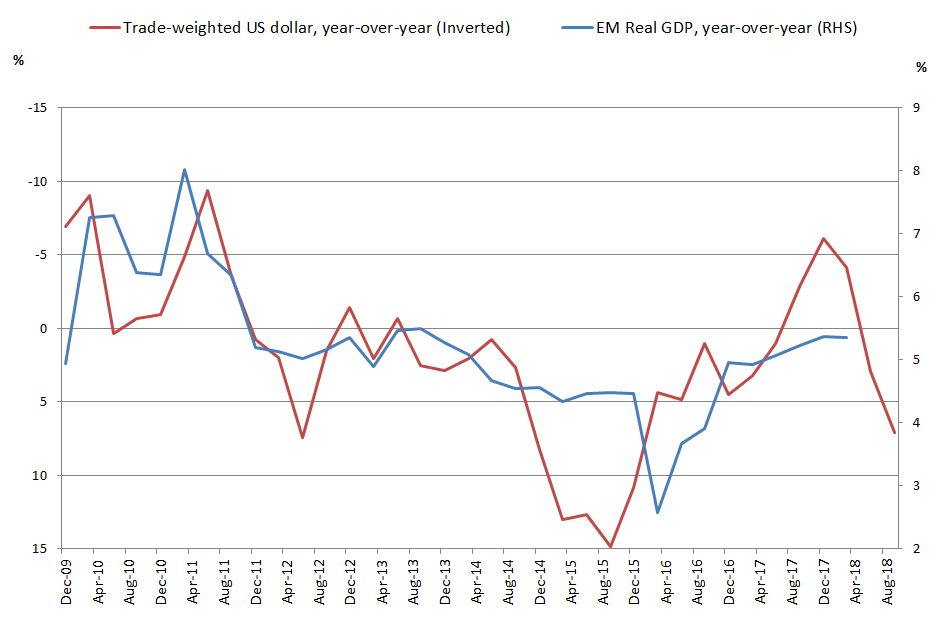

US dollar and EM growth inversely related

There is a persistent relationship between trends in the trade-weighted US dollar and EM growth. Though other factors contribute – such as commodity prices – the US dollar tends to dictate domestic financial conditions for many EM countries via the domestic currency. As the domestic currency depreciates versus the US dollar, domestic financial conditions tighten (and vice versa). It takes time for this depreciation to improve export competitiveness and contribute to net trade. Meanwhile, as domestic financial conditions tighten, so too does domestic demand and overall growth.

Figure 1: Past US dollar weakness has supported EM growth via financial conditions

Source: BIS, Macrobond, Invesco, Dec. 31, 2009 to Sept. 29, 2018.

Outlook and strategy

A scenario of further material tightening in US dollar funding conditions – particularly if the cost of borrowing increases while US dollar funding availability diminishes – may place lower-rated sovereign and corporate issues under repayment duress, particularly those without external funding backstops. However, Invesco Fixed Income believes there has been value creation in certain segments of the market. Some have been unjustifiably impacted by recent concerns over the tightening in US dollar-funding conditions. Therefore, there may be opportunities to add exposure to these select markets.

Stability in Argentina and Turkey alone should give way to an EM asset-price recovery, and the recent market-friendly election result in Brazil should have the same effect if we see a move towards pension and fiscal reform. At the same time, we acknowledge uncertainties related to policy orientation during the recent EM election cycle, which will continue into 2019 with elections in Argentina, Indonesia and South Africa in focus. More immediately, the public consultation in Mexico on the fate of the new airport in Mexico City has cast a long shadow on the policy priorities of the incoming administration. We will look for more supportive policy signals out of South Africa and Turkey. The prospect of additional US sanctions on Russia also looms.

In the context of recent policy easing efforts in China, stability in the renminbi along with indications of broader stability in the US dollar (and US funding conditions) would provide much needed support to EM fixed income. The importance of these macro drivers cannot be overstated. The rest will depend on policy outcomes in individual countries. In this sense – and importantly – the market is likely to be driven increasingly by idiosyncratic outcomes, a dynamic that is likely to endure well into 2019.

Important information

Blog header image: hxdbzxy/Shutterstock.com

Idiosyncratic developments refer to unique events that do not affect an entire market or portfolio.

Exogenous factors are external events or conditions not explained by an economic model or forecast.

The risks of investing in securities of foreign issuers, including emerging market issuers, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

The dollar value of foreign investments will be affected by changes in the exchange rates between the dollar and the currencies in which those investments are traded.

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Issuers of sovereign debt or the governmental authorities that control repayment may be unable or unwilling to repay principal or interest when due, and the Fund may have limited recourse in the event of default. Without debt holder approval, some governmental debtors may be able to reschedule or restructure their debt payments or declare moratoria on payments.

The performance of an investment concentrated in issuers of a certain region or country is expected to be closely tied to conditions within that region and to be more volatile than more geographically diversified investments.

Rashique Rahman

Head of Emerging MarketsRashique Rahman joined Invesco in 2014 as the Head of Emerging Markets (EM) for Invesco Fixed Income.

Throughout his career, Mr. Rahman has led or been a part of various EM strategy and research teams. Previously, he was co-head of global foreign exchange (FX) and EM strategy at Morgan Stanley, leading the global EM fixed income and currency effort. Prior to this, he led global strategy for EM at HSBC in its New York office. He has also held positions at Citigroup, both as a senior EM strategist and as a principal trader based in London. He worked as a portfolio manager for local EM (rates/FX) at Armored Wolf, a US-based, multi-asset alternative asset manager. His background also includes work as a sovereign analyst at Standard & Poor’s in the sovereign ratings group.

Mr. Rahman earned an MBA and MA at Columbia University and earned his undergraduate degree at UCLA.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2018 Invesco Ltd. All rights reserved.