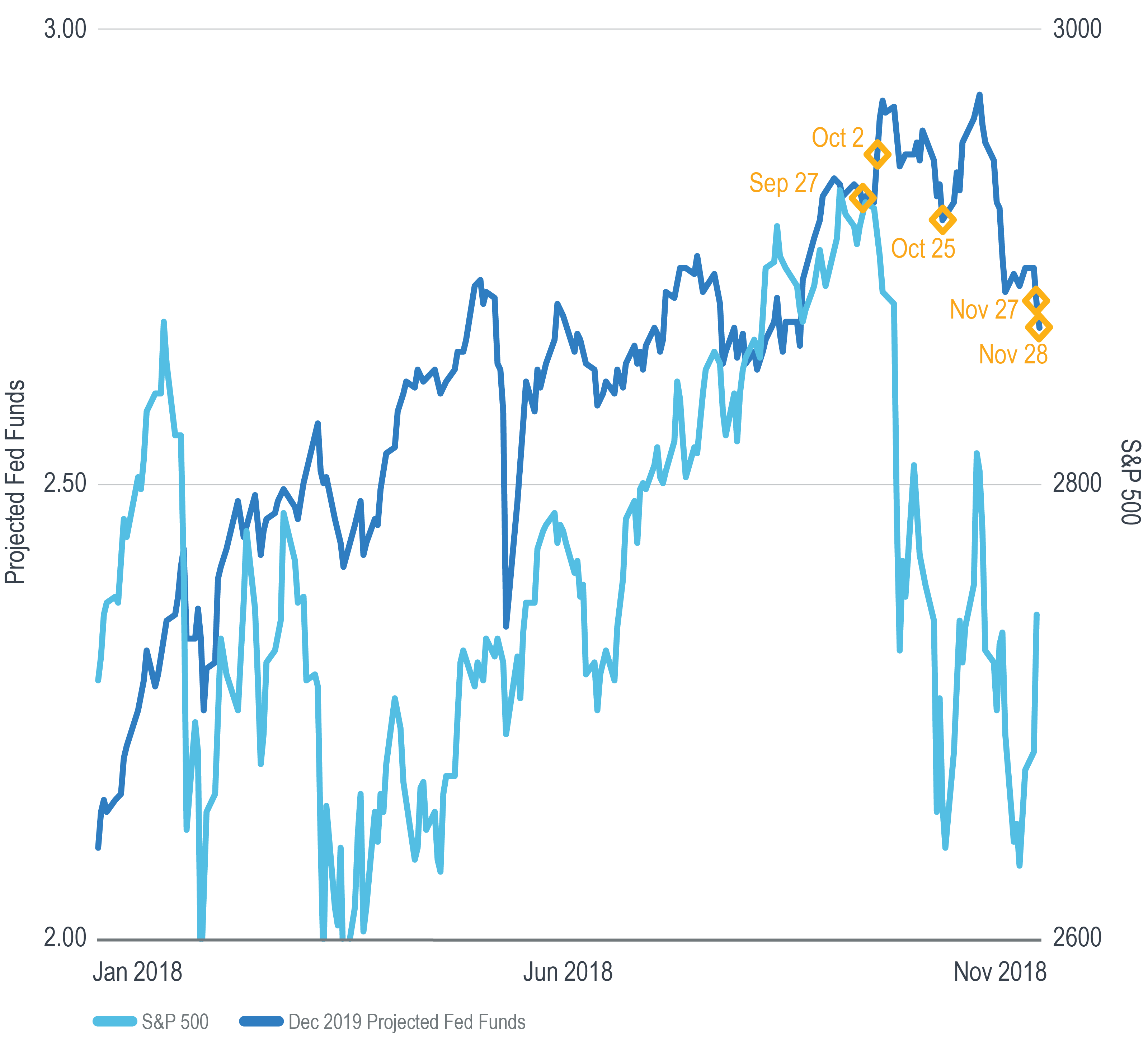

On Thursday, November 28, 2018, the S&P 500 rose by 2.30%, its largest one-day increase since March 2018. The bulk of the move came during the second half of the day, beginning at the precise moment when Federal Reserve Governor Powell commented on interest rates.

In the weeks leading up to November 28, he and other Fed officials had been indicating an intention to continue gradually increasing the fed funds rate. The change of sentiment from “long way from neutral” on October 3, to “just below neutral” on November 28, marked a sharp reversal of the forward guidance they had been giving.

This subtle change caused the projected fed funds rate to continue to fall and the stock market to rise. The following speech and interview excerpts chronicle the changes in the Fed’s sentiment, corresponding to the dates in the chart highlighted in orange.

- September 27, Chairman Powell: “We took another step on that path [toward normal] yesterday, with a quarter-point increase in short-term interest rates. These rates remain low”¹

- October 2, Chairman Powell: “The baseline outlook of forecasters inside and outside the Fed is for more of the same…Our ongoing policy of gradual interest rate normalization reflects our efforts to balance the inevitable risks”²

- October 3. Chairman Powell: “We may go past neutral, but we’re a long way from neutral at this point, probably.”3

- October 25, Vice Chairman Clarida: “even after our September decision [to raise rates], I believe U.S. monetary policy remains accommodative…the inflation-adjusted real funds rate remains below the range of estimates”4

- November 27, Vice Chairman Clarida: “Although the real federal funds rate today is just below the range of longer-run estimates”5

- November 28, Chairman Powell: “Interest rates are still low by historical standards, and they remain just below the broad range of estimates of the level that would be neutral for the economy”6

Whether it was the heightened market volatility in October and November, comments made by President Trump, or some other factor that lead to the change in Fed sentiment, investors may never know. They might, however, reasonably conclude that bringing an end to a period of unprecedented monetary accommodation is both easier said than done and unlikely to be without some recalibration along the way.

Links to speech transcripts:

- https://www.federalreserve.gov/newsevents/speech/powell20180927a.htm

- https://www.federalreserve.gov/newsevents/speech/powell20181002a.htm

- https://www.cnbc.com/2018/10/03/powell-says-were-a-long-way-from-neutral-on-interest-rates.html

- https://www.federalreserve.gov/newsevents/speech/clarida20181025a.htm

- https://www.federalreserve.gov/newsevents/speech/clarida20181127a.htm

-

https://www.federalreserve.gov/newsevents/speech/powell20181128a.htm

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.