When investors seek to take advantage of publicly listed real estate opportunities, they often favor traditional REIT common stock to gain exposure. This makes sense — from Oct. 1, 2008 through Sept. 30, 2018, US REIT common stock has provided attractive returns coupled with income generation, potential diversification benefits and a potential hedge against inflation.1 However, we believe US REIT preferred stock may offer a unique opportunity for investors to access real estate-like returns with even higher income (and lower volatility) versus traditional REIT common stock.

Understanding US REIT preferred securities

REIT preferred stock is a type of hybrid security with both equity- and bond-like characteristics. Within the capital structure of REIT companies, preferred stocks have a senior claim to earnings and dividends versus common stock but are generally junior to corporate bonds. The dividends paid on REIT preferred stock are often considerably higher than REIT common stock and shares are generally issued at a par value (often $25). While REIT preferred shareholders have no voting rights, they can often benefit from investing when issues are trading at discounts to par. REIT preferred stock is generally callable after five years from the date of issuance, at which point management reserves the right to redeem the shares at par. This five-year non-call period provides the potential not only for income, but also capital appreciation. The five-year non-call period also gives investors a more certain return opportunity over the time period, which may be an additional benefit.

Why do companies issue REIT preferred stock?

So why do REIT companies issue preferred stock at all given the options of simply issuing common equity or traditional corporate debt? First, when REIT companies issue preferred stock (versus traditional corporate debt) they are often given more favorable treatment by rating agencies. This allows companies to showcase lower leverage levels to prospective investors and analysts. Second, REIT preferred stock provides companies with a unique source of capital. While these shares are generally callable after five years at par, company management reserves the right to keep the shares outstanding in perpetuity. A broad array of REIT companies offer preferred stock, including those that operate in sectors focused on residential, office, retail, industrial, self-storage, data centers, infrastructure, healthcare and lodging. While the universe of US REIT preferred stock is relatively small by number of issuers and total capitalization, the benefits to investors have historically been quite compelling.

A comparison: US REIT preferred stock versus US REIT common stock

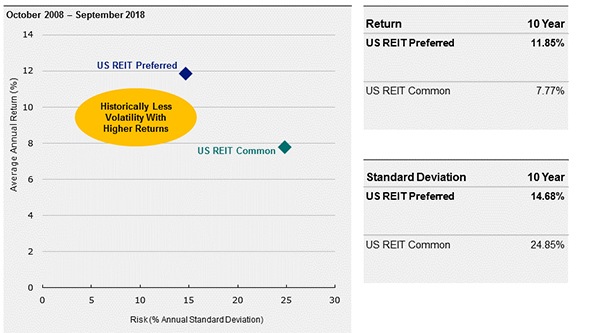

Over the last ten years – since the global financial crisis in October 2008 to the present – REIT preferred stock has outperformed REIT common stock with roughly half the volatility. The higher level of income generated by the preferred shares, coupled with the potential for capital appreciation for discounted securities, has allowed this segment of the capital structure to generate excess returns.

Over the past ten years, US REIT preferred stock has outperformed US REIT common stock

Source: Invesco Real Estate, Wells Fargo and Zephyr StyleADVISOR. US REIT Preferreds represented by Wells Fargo Hybrid and Preferred Securities REIT Index; US REIT common represented by FTSE NAREIT All Equity REITs Index. Data from October 2008 through September 2018. Past performance does not guarantee future results. An investment cannot be made directly into an index.

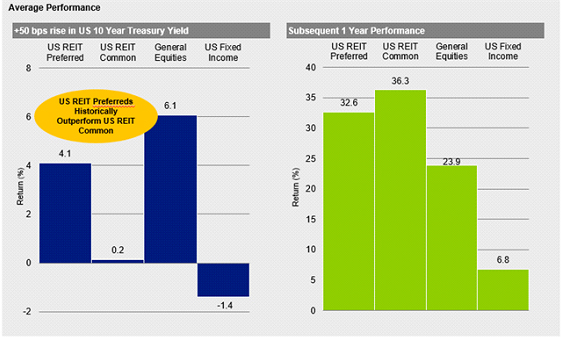

Over the last ten years through September 30, 2018, the Invesco Real Estate team has also observed that US REIT preferred stock has tended to outperform REIT common stock during periods of rising interest rates. We believe that the higher level of yield spreads versus the 10-year Treasury and other preferred sectors have allowed these securities to insulate themselves more to periods of rising interest rates. Concurrently, the subsequent one-year performance of the US REIT preferred universe was slightly less that of US REIT common stock while outperforming equities and fixed income. As of Sept. 30, the US REIT preferred market sported an average yield of 6.69%, relative to the 4.06% yield of the FTSE NAREIT All Equity REIT Index.

US REIT preferred stock has tended to outperform REIT common stock during periods of rising rates

Source: Invesco Real Estate, Bloomberg and Wells Fargo. Average total returns where the cumulative rise in 10-Year US Treasury yields for each full month period is above 50 basis points and the one year subsequent periods from October 2008 through September 2018. US REIT Preferred represented by Wells Fargo Hybrid and Preferred REIT Index. US REIT Common represented by FTSE NAREIT All Equity REITs Index. General Equities represented by S&P 500. US Fixed Income represented by Barclays US Aggregate Bond Index. Past performance does not guarantee future results. An investment cannot be made directly into an index.

Given the yields of US REIT preferred stock today (which generally span from 5% to 8%), investors have the right to question the sustainability of these distributions. Unlike financial preferreds, which have experienced certain periods of double-digit levels of payment defaults, since 2000 the US REIT preferred universe has never seen a year with more than a 1% level of missed payments. In the past 18 years, the average annual default rate for US REIT preferred stock has been a modest 0.25%, reflecting the stable and predictable cashflows generated by real estate-related companies over the period. And in the last four calendar years there have been no defaults in the broader US REIT preferred universe at all.2

Making the case for active management in US REIT preferred stock

Despite a relatively healthy environment for US commercial real estate — backed by a modest economic expansion, rising consumer and business confidence, relatively high occupancy rates and reduced leverage for the real estate sector overall — the Invesco Real Estate team believes that a prudent and active approach is still vital to achieving better risk-adjusted outcomes for investors. To that end, we intend to analyze all 150 available REIT preferred securities in the US and evaluate them based on three key criteria:

- The management quality and structure of the REIT company (by evaluating its focus and strategic plan, alignment of interest with shareholders and assessment of the firm’s balance sheet strength).

- The market strength of the REIT company (by analyzing its sector and geographic footprint).

- The asset evaluation of the REIT company (by analyzing the locational and physical attributes of its assets).

Other criteria which will be evaluated for all REIT preferred securities will be the weighted-average coupon, duration to call, credit rating, issuance size, leverage and fixed charge coverage for all eligible investments. As a residual of this overall analysis, the investment team is likely to uncover attractive US REIT preferred securities with convertible optionality to common stock. We believe convertible REIT preferred securities may create better tracking relative to common stock and may provide more robust protection against rising interest rates than non-REIT preferred stock.

Key takeaways

The Invesco Real Estate team believes that the utilization of US REIT preferred stock (in portfolios allowing these securities) may enhance return, reduce volatility and add to income generation over time compared to a pure REIT common stock portfolio. The team has the ability to actively monitor and analyze the broader capital structure of the US REIT universe to find attractive REIT opportunities — both in common and preferred stock. By utilizing a number of qualitative and quantitative tools, we can narrow the universe of eligible investments into a pool of what we consider more attractive REIT preferred securities and maintain the ability to overweight and underweight sectors and stocks.

While the industry trend has traditionally focused on the creation of real estate vehicles exclusively focused on REIT common stock, we believe that by leveraging the various funding mechanisms of real estate, we may obtain stronger risk-return outcomes over the long term. By pairing REIT common stock positions with REIT preferred stock (and considering REIT corporate debt and collateralized mortgage-backed securities in select portfolios) the team believes it can help generate the capital appreciation and income generation needed by clients in a more risk-controlled fashion. The objective: generate real estate equity-like returns with lower volatility, better Sharpe ratios, shallower drawdowns, higher income and less correlation to the broader equity market.

About Invesco Real Estate

Invesco Real Estate has nearly 490 employees in 21 different markets worldwide with assets under management exceeding $65 billion as of June 30, 2018. Our focus areas include US and global real estate, global real estate income, infrastructure and master limited partnerships.

Learn more about Invesco Global Real Estate Income Fund.

1 Source: Bloomberg L.P., S&P and FTSE/EPRA, data as of Nov. 1, 2018

2 Source: Invesco Real Estate, Bloomberg, and Wells Fargo. Data as of Sept. 30, 2018 and updated annually. US REIT Preferred represented by Wells Fargo Hybrid & Preferred REIT Index. US Financial Preferred represented by Wells Fargo Hybrid & Preferred Securities Financial Index. Invesco defines a “default” as when a scheduled cash payment is not made for any reason, including an unpaid cash dividend prior to the initial non-payment date.

Important information

Blog header image: Roman Babakin/Shutterstock.com

A real estate investment trust (REIT) is a company that owns (and typically operates) income-producing real estate or real estate-related assets.

Preferred stock is class of ownership in a corporation that has a higher claim on its assets and earnings than common stock.

A collateralized mortgage-backed security is a fixed income security that uses mortgage-backed mortgage as collateral.

The Sharpe ratio is a measure of risk-adjusted performance calculated by dividing the amount of performance a portfolio earned above the risk-free rate of return by the standard deviation of returns; a higher Sharpe ratio indicates better risk-adjusted performance.

The Wells Fargo Hybrid and Preferred Securities REIT Index is a market capitalization-weighted index that is designed to track the performance of preferred stocks issued by real estate investment trusts. It is comprised of preferred stock and other securities that Wells Fargo believes are functionally equivalent to preferred stocks including (but not limited to) depositary preferred securities, perpetual subordinated debt and certain capital securities.

The FTSE NAREIT All Equity REIT Index is an unmanaged index considered representative of US REITs.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The Barclays US Aggregate Bond Index is an unmanaged index considered representative of the US investment-grade, fixed-rate bond market.

There is no guarantee that companies will declare future dividends, or that if declared, they will remain at current levels or increase over time.

Investments in real estate related instruments may be affected by economic, legal, or environmental factors that affect property values, rents or occupancies of real estate. Real estate companies, including REITs or similar structures, tend to be small and mid-cap companies and their shares may be more volatile and less liquid.

Preferred stock generally has a preference as to dividends and liquidation over an issuer’s common stock but ranks junior to debt securities in an issuer’s capital structure. Unlike interest payments on debt securities, preferred stock dividends are payable only if declared by the issuer’s board of directors. Preferred stock also may be subject to optional or mandatory redemption provisions.

Preferred securities may include provisions that permit the issuer to defer or omit distributions for a certain period of time, and reporting the distribution for tax purposes may be required, even though the income may not have been received. Further, preferred securities may lose substantial value due to the omission or deferment of dividend payments.

David Wertheim

Senior Client Portfolio Manager

David Wertheim is a Senior Client Portfolio Manager focused on real asset securities. In this capacity, he works with Invesco’s real assets investment management team, serving as its representative to clients and prospects.

Mr. Wertheim began his career in 2000 and joined Invesco in 2018. Prior to joining Invesco, he was a senior client portfolio manager for real assets, commodities and equities with Deutsche Asset Management.

Mr. Wertheim earned a BBA from George Washington University with a dual concentration in international business and marketing.

Darin Turner

Managing Director, Portfolio Manager

Invesco Real Estate

Darin Turner is a Managing Director and Portfolio Manager for Invesco Real Estate. He performs quantitative and fundamental research on real asset securities, and his primary portfolio responsibilities include midstream energy, utilities, renewables and transportation infrastructure on a global basis.

Mr. Turner joined Invesco in 2005 as an acquisitions analyst and later served as the associate portfolio manager for Invesco Real Estate’s US Value Added Funds. Prior to joining Invesco, Mr. Turner was a financial analyst in the corporate finance group of ORIX Capital Markets, where he was responsible for the daily evaluation of a structured finance portfolio, as well as for analyzing the performance of specific collateralized debt obligations. Additionally, he was responsible for the execution of a high yield repurchase facility and a leveraged loan swap agreement, as well as the implementation of certain portfolio hedging strategies.

Mr. Turner earned a BBA in finance from Baylor University, an MS degree in real estate from the University of Texas at Arlington and an MBA degree specializing in investments from Southern Methodist University.

Jim Pfertner

Associate Director

Real Estate Securities

Jim Pfertner is a member of the Real Estate Securities Portfolio Management and Research team with Invesco Real Estate. He performs fundamental and quantitative research on master limited partnership, infrastructure and real estate securities, including common and preferred equities, structured products and corporate bonds. Mr. Pfertner also provides capital structure analysis and debt pricing analysis for equity portfolios.

Prior to joining Invesco, Mr. Pfertner worked as a director at Highland Capital Management, LP, where he focused on identifying investment opportunities in both debt and equity investments. In addition, he managed a portfolio consisting of commercial mortgage-backed securities, real estate investment trusts, syndicated loans and equity real estate investments. Prior to Highland, he worked as an investment analyst for Prudential Mortgage Capital Company, underwriting commercial and multi-family properties across the US for debt investment opportunities. Prior to Prudential, he held various roles with JPMorgan Chase and Morgan Stanley. He entered the industry in 2001.

Mr. Pfertner earned an MBA from Southern Methodist University and a BA degree in economics from The University of Texas at Austin.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

| NOT FDIC INSURED |

MAY LOSE VALUE |

NO BANK GUARANTEE |

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2019 Invesco Ltd. All rights reserved.

Read more commentaries by Invesco

Source: Invesco Real Estate, Bloomberg and Wells Fargo. Average total returns where the cumulative rise in 10-Year US Treasury yields for each full month period is above 50 basis points and the one year subsequent periods from October 2008 through September 2018. US REIT Preferred represented by Wells Fargo Hybrid and Preferred REIT Index. US REIT Common represented by FTSE NAREIT All Equity REITs Index. General Equities represented by S&P 500. US Fixed Income represented by Barclays US Aggregate Bond Index. Past performance does not guarantee future results. An investment cannot be made directly into an index.

Source: Invesco Real Estate, Bloomberg and Wells Fargo. Average total returns where the cumulative rise in 10-Year US Treasury yields for each full month period is above 50 basis points and the one year subsequent periods from October 2008 through September 2018. US REIT Preferred represented by Wells Fargo Hybrid and Preferred REIT Index. US REIT Common represented by FTSE NAREIT All Equity REITs Index. General Equities represented by S&P 500. US Fixed Income represented by Barclays US Aggregate Bond Index. Past performance does not guarantee future results. An investment cannot be made directly into an index.