For the stocks of Facebook, Amazon, Netflix, and Google, often referred to as a group under the acronym of FANG, 2017 and 2018 have been remarkable.

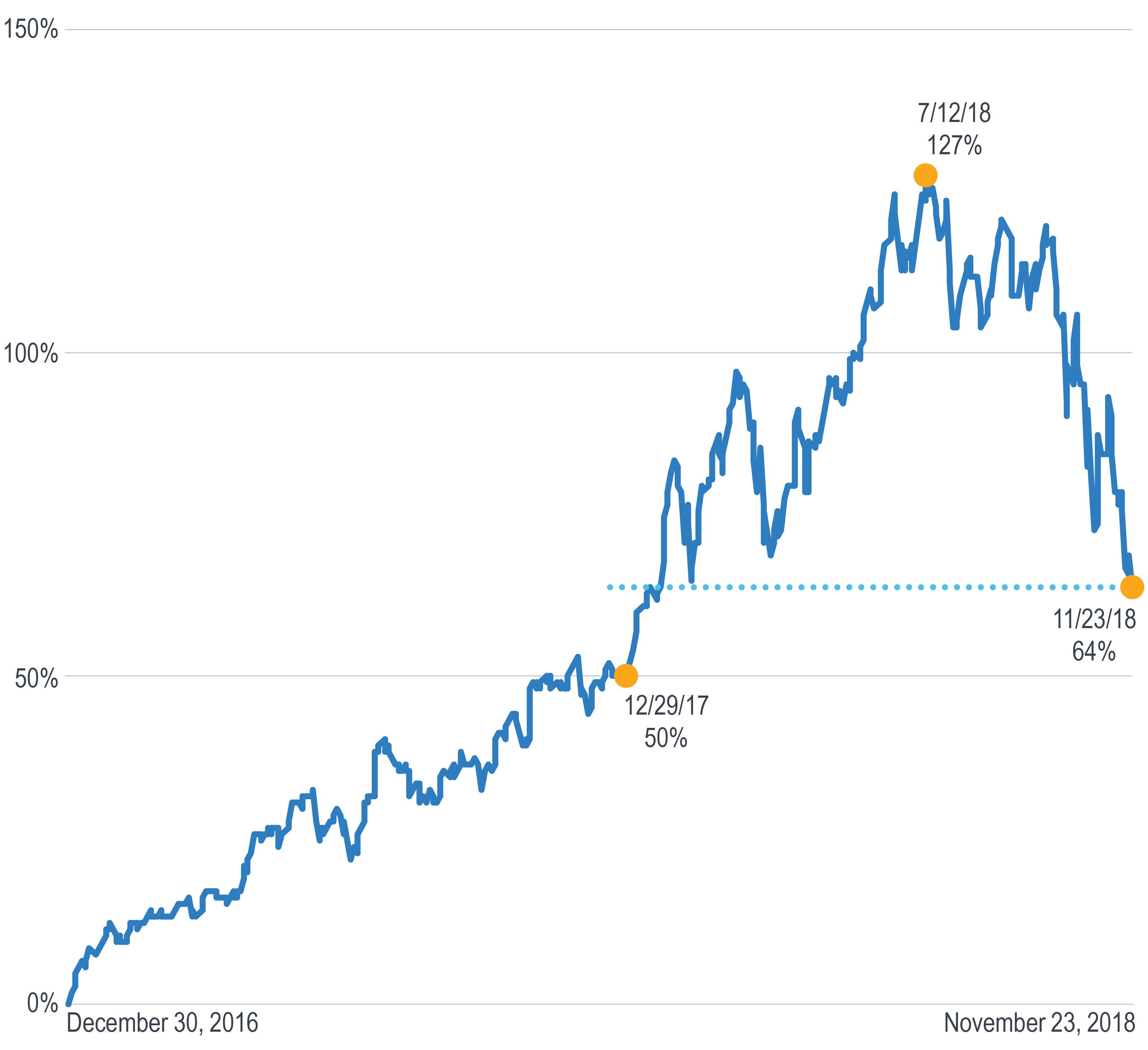

A portfolio equally weighted between the four, purchased at their respective closing prices at the end of 2016 would have climbed 50% in 2017. Letting that portfolio ride into 2018, it would have climbed another 51% through July 12, for a cumulative increase of 127%.

Since then, however, the FANG group has struggled. Over the course of the last four months, from its peak on July 12 through November 23, the group is down 28%. Recent news isn’t helping.

Amazon’s revenue guidance for the seasonally important Q4 came in well below estimates.

In late October Netflix issued another $3.8 billion of bonds on top of the $10 billion it already had outstanding, to finance what it expects will be negative cash flow of $3 billion for 2018.

Meanwhile, Facebook and Google continue to deal with legal and reputational challenges stemming from data breaches.

For the period from Jan.1, 2017 through July 12, 2018, the FANGs made up four of the six top contributions to the return of the S&P 500. After climbing by so much and reverting so quickly, FANG will be under close watch by market participants to gauge their potential to contribute going forward.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.