Whole Lotta Shakin’ Goin’ On

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWell, come on over baby

Whole lot of shakin' goin' on

I said come on over baby

Baby, you can't go wrong

We ain't fakin'

Whole lotta shakin' goin' on

Well, come on over baby

We got chicken in the barn

(Whose barn, what barn, my barn)

I said come on over baby

Really got the bull by the horn

We ain't fakin'

Whole lotta shakin' goin' on

(From “Whole Lotta Shakin’ Goin’ On”, written by Dave "Curlee" Williams and James Faye "Roy" Hall, recorded by Jerry Lee Lewis, 1957)

We're caught in a trap

I can't walk out

Because I love you too much, baby

Why can't you see?

What you're doing to me

When you don't believe a word I say?

We can't go on together

With suspicious minds

And we can't build our dreams

On suspicious minds

(From ”Suspicious Minds”, by Mark James, recorded by Elvis Presley, 1969)

Last month, we referenced the phrase “October Surprise” in its usual political context. Well, we certainly had a surprise, but it was markets-related rather than political. After months of investor complacency and a sky-rocketing technology sector, the markets suddenly got spooked on the backs of global trade tensions, non-US economic deceleration (especially in China), a very strong US dollar, and the seeming realization that the growth catalysts provided by the tax law reforms, regulatory relief, and fiscal stimulus would, at some point, work through the system and begin to trail off.

The market decline has been fairly continuous since late August, right through late-November, as we write this. A pre-Thanksgiving Wall Street Journal article pointed out that since its September 3rd peak, the S&P 500 index had fallen 7.7%, while the NASDAQ index, which is dominated by tech stocks, had fallen 13.3% since its August 29th peak. As we go to publication, all major global equity markets are now trading in negative territory for the year.

Non-US markets have fared even worse over the course of the year, victims to slowing global growth, repressed commodity prices, the strong US dollar, and a corresponding “flight to quality” by investors. The Developed International markets (as measured by the MSCI EAFE index) are down roughly 11.50% year-to-date (YTD), and the Emerging Markets (as measured by the MSCI EM index) is down more than 16%. Interestingly enough, many contrarian investors are beginning to consider re-allocating back into non-US markets, as valuations have become “oversold” relative to economic and earnings growth potential.

One of the recent catchphrases seen in various publications is “Live by the FAANG, Die by the FAANG”. “FAANG”, of course, refers to Facebook, Amazon, Apple, Netflix, and Alphabet (Google) which, along with Microsoft, have been the predominant drivers of the stock market rally for some time. Callan, LLC, a large institutional consulting firm, indicated that, over the past five years through August 31st, those six tech-oriented stocks had driven 35% of the growth in the S&P 500 index (and a whopping 47% of the growth in the Russell 1000 Growth index).

Given the market’s tendency to mean-revert over time, it therefore is not surprising that these same stocks have fallen especially hard over the past six weeks. Facebook in particular has struggled, as investors react to issues regarding data privacy, decelerating earnings, and changing user demographics as younger social media users move on to newer, “cooler” platforms.

But some perspective is in order. In the US, earnings and economic growth remain positive, though both are expected to slow as we move through 2019. Interest rates remain fairly low (and have moved even lower during the recent market decline and corresponding “flight to quality”), and inflation remains under control. The Fed will still most likely raise rates in December, but the recent volatility may result in it slowing its rate hike plan for 2019, which the markets will view as positive. Finally, while the past 5-6 weeks have been stressful for investors, in some respects all we have witnessed is the proverbial “taking some air out of the tires” of what arguably could be called an “over-exuberant” market (especially in the US, and especially in technology stocks).

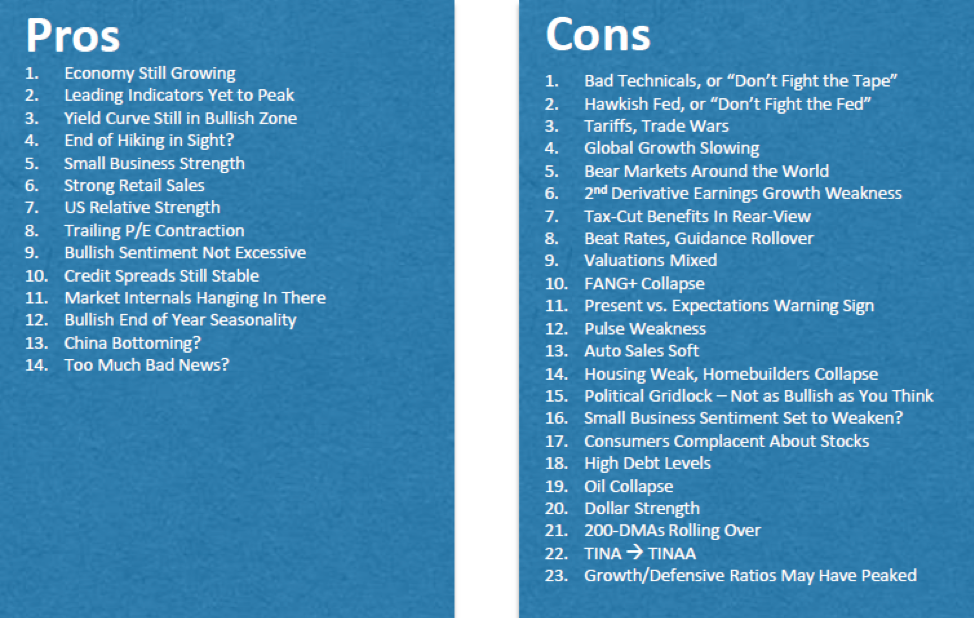

Bespoke Investment Group summarizes the situation in the US very nicely in the following tables*:

[* Number 22 on the “Con” side, “TINA à TINAA”, requires an explanation. “TINA” stands for “There is No Alternative”, and refers to a market environment in which investors’ only hope of a positive return is to invest in stocks (i.e., when interest rates are close to zero). Now that rates are rising, investors can earn a positive return in the bond market, and so we have evolved into a “TINAA” market – “There is Another Alternative” – the implication being that some investors may choose to de-risk their portfolios by reallocating out of stocks and back into bonds.]

While the “cons” outnumber the “pros”, we believe the relative strength of the “pros” is greater. We are not blindly optimistic or bullish (we never are) but, given the generally still positive economic and earnings environments here in the US, we do believe that US markets can move higher from current levels and end the year in positive territory, albeit with increased volatility.

With that as a backdrop, looking out over the current economic and investment landscapes, here is what we see.

The Current Economic Landscape

The global economy continues to grow, though with distinct signs of deceleration, especially outside the US:

- The first estimate for Q3 GDP growth in the US is a solid 3.5%, in line with expectations. That growth is expected to decelerate to 2.6% in Q4 (lower than previous estimates, as the effects of tax reform, regulatory relief, and fiscal stimulus begin to taper off), bringing overall 2018 GDP expectations to 3.1%; (source: The Wall Street Journal);

- This GDP forecast remains sensitive to ongoing trade negotiations, political tensions in Europe regarding Italy and “Brexit”, and continued unrest in Saudi Arabia and the broader Middle East;

- The US mid-term elections turned out largely as expected: the Democrats regained control of the House and several governorships, while the Republicans slightly increased their majority in the Senate. While the partisan rhetoric is likely to be raucous and negative, the bottom line result is likely to be gridlock, with no major policy initiatives moving forward but, on the other hand, no reversal of recently passed tax and regulatory reforms. Historically, the markets largely have been “unbothered” by DC gridlock;

- Both US manufacturing and services remained strong in October, with the PMI (manufacturing index) coming in at 57.7, down from 59.8 in September, while the NMI (non-manufacturing index) fell slightly to 60.3, down from 61.6 in September; any reading above 50 is considered expansionary. The manufacturing index has now been in expansionary territory for 114 consecutive months, while the non-manufacturing index notched its 105th consecutive expansionary month (source: Institute for Supply Management);

- One possible future trouble spot for the US economy is a marked slow-down in the housing sector, as permits, housing starts (especially in the multi-family sector), and affordability have all trended downward for several months. The stock prices of homebuilders have been hit especially hard by the recent market declines (source: Bespoke Premium);

- Inflation (as measured by CPI) increased to 2.5% year-over year in October, up slightly from 2.3% in September, continuing a 4-month trend. Oil prices (as measured by WTI) have declined steadily since late September, falling from roughly $76 per barrel to roughly $53 per barrel as we head into late November. Wages continue to increase (up 4.6% year-over-year in September, the most recent reading), but a slowing global economy outside the US, especially in China, combined with a strong US dollar, are keeping commodity prices under control (even falling). The Personal Consumption Expenditure (PCE) index – the Fed’s preferred measure of overall inflation – increased 1.9% year-over-year in September (the most recent reading), down slightly from 2.2% in August – still generally in line with the Fed target rate (source: TradingEconomics).

- We continue to believe that inflation will increase slowly, but will remain somewhat dampened by (1) continued slow (but positive) wage growth; (2) a strong dollar; and (3) a decelerating global economy (ex-US), which will dampen demand. As such, we continue to believe that inflation does not yet constitute a primary risk to economic growth;

- As expected, the Fed raised interest rates in late September, and there is a strong consensus that it will do so again at its December meeting. Recent market volatility, however, has introduced a distinctly more “dovish” tone to the public pronouncements from different Fed members, and we may very well see a backing off of its proposed 3-4 additional rate hikes in 2019, to perhaps only one or two over the course of the year.

- As we’ve written previously, President Trump does not agree with current Fed policy, and has made it clear that he wants the dollar weaker and interest rates kept low (he is unlikely to achieve either objective). Should the economy slow down or the current market downturn continue, it is a safe bet that Trump will hold the Fed responsible, but also make it more likely that the Fed will back off its “normalization” plan;

- The yield curve has risen steadily over the past several months but remains very flat, as the Fed raises rates on the short end but the long end remains “tamped down” by high demand (especially in recent weeks due to a “flight to quality” rally) and a lack of inflation fears. As of late November, there remains less than 30 basis points difference between the yield on the 2-year and 10-year Treasury (source: YCharts).

- We saw a rally in the longer end of the curve through late November, due to the market disruption, but the 10-year rate remains (slightly) above the psychological barrier of 3%, and we repeat that we do not anticipate (or fear) an inverted yield curve – should one occur, we believe it will be because of investment flows and Fed actions, not a harbinger of an imminent recession;

- The US dollar remains strong. It has risen fairly steadily since April against the euro, the Japanese yen, and (especially) the Chinese yuan. The Chinese are actively devaluing the yuan in an attempt to kick-start their economy and mitigate the impact of the ongoing trade tensions with the US. With non-US global growth slowing down and the Fed raising rates, it is hard to see any catalyst that would reverse the dollar’s current strength over the near term (source: YCharts);

- The Q3 earnings season is now largely over, and it was another strong quarter. Of the roughly 450 S&P 500 companies that had reported through the second week of November, we saw a 26.2% increase in earnings on 8.8% higher revenues. The earnings “beat rate” (i.e., reported earnings higher than expected) was 78.5%, while the revenue “beat rate” was 63.5%. Both are good levels and in line with historical averages. Many companies continue to use financial engineering (stock buybacks, etc.) versus top-line organic growth to generate earnings growth. Growth is still to decelerate as we head into Q4 and then 2019, with Q4 earnings growth estimates of 13.7% and 2019 earnings and revenue growth estimates of 9.7% and 5.1%, respectively (sources: Zachs Earnings Report);

- Manufacturing across the Eurozone remains expansionary, though the Markit Manufacturing index fell to 52 in October, versus 53.2 in September, a continuation of a general YTD decline. Likewise, the Services index fell slightly to 53.7 in October from 54.7 in September – the slowest services expansion rate since October 2016 (source: TradingEconomics);

- The economic slowdown in China is having a particularly hard effect on German manufacturing (e.g., autos and machinery), with the German manufacturing index falling to 52.3 in October, the lowest level since May 2016 (source: TradingEconomics);

- Eurozone unemployment remained at 8.1% in September (the most recent reading), the same level as in August, and it remains at its lowest level since December of 2008. Annualized inflation edged up to 2.2% in October, up slightly from 2.1% in September (source: TradingEconomics);

- Japan’s GDP fell 1.2% (annualized) in Q3, its second negative quarter in 2018, driven by slowing exports (despite a generally weakening yen) and slowing internal consumer demand. The Japanese economy is expected to continue to decelerate, and there is a possibility it will post negative overall growth in 2018 (source: TradingEconomics);

- China’s (official) GDP growth in Q3 was 6.5% (annualized), down from previous quarters, and the lowest (official) growth rate recorded since Q1 2009. There are other (non-official) signs that suggest the Chinese economy is slowing faster than the official numbers indicate. For example, the Chinese Caixin Manufacturing Index fell to a 17-month low of 50.1 in October (barely expansionary), the Chinese stock market is down roughly 20% YTD, and the yuan continues to weaken significantly against the dollar (source: TradingEconomics).

The Dynasty Economic & Market Outlook:

- The global economy continues to (slowly) expand, though there remains a distinct deceleration and “desynchronization” of growth. The US economy shows continued solid growth, with perhaps some yellow lights beginning to flash (e.g., housing and the recent market correction), and there is an expectation of a decelerating economy through 2019 as the effects of fiscal stimulus and regulatory and tax reform begin to tail off. At the same time, the rest of the world appears to be decidedly decelerating – still expansionary, but slowing down (especially in Japan and China);

- US Inflation is trending higher, but we maintain our belief that it (as of yet) does not represent a problem for continued economic expansion. Wages in the US are increasing slowly, oil prices have fallen significantly over the past two months, and overall commodity prices remain repressed by slowing demand and the strong dollar. Outside the US, inflation simply is not a problem, and in fact Europe may soon begin to worry once again about entering into a deflationary regime;

- In the US, tax and regulatory reform and fiscal stimulus continue to win the ongoing economic tug-of-war against monetary tightening, and continue to pull future consumption forward. The Fed previously had a laid out a fairly aggressive tightening program over the next 12-15 months, but there is now some belief it may “back off” of that plan in the face of the recent market correction and expectations for a slowing economy in the latter half of 2019;

- There is some concern about a potential government shutdown over budget disagreements, especially now that we have a split Congress, but the market does not seem to be pricing in that risk at the current time. Likewise, at some point, the markets will need to be concerned once again about massively increasing deficits and debt, but right now neither party (nor, especially, President Trump) show the slightest interest in addressing this rapidly growing problem;

- Solid US GDP growth, as well as respectable earnings and revenue growth, make for a generally positive market environment, and despite the recent sell-off, we maintain our view that US stocks will end the year higher than where they began.

- As we discussed above, however, the markets seemingly have begun to react to expectations of decelerating earnings growth, decelerating economic growth, and generally rising interest rates. Through late November, we’ve seen these factors, plus uncertainty over trade policy, all combine to push valuations down and volatility up;

- It is important to maintain perspective on the recent market downturn. According to Bespoke Investment Group, the current market correction (through mid-November) does not even rank in the top five worse corrections since the current bull market rally began back in March of 2009. In our view, this simply is a return to more normal market valuations and volatility;

- Ongoing trade tensions between the US and China, European tensions over Italy’s fiscal state and the UK’s struggles with “Brexit”, and decelerating non-US economic growth seem to be the largest potential threats to the current generally positive market regime;

- EM and EAFE (Developed International) markets continue to be hurt by a generally strong US dollar, trade tensions, and a corresponding “risk off” mentality driving investment outflows.

- That said, both EAFE and EM markets have outperformed the US markets on a relative basis since the current US market correction began in October. Investors are beginning to reenter these markets due to attractive valuations following the steep declines earlier this year. These markets almost undoubtedly will post negative performances in both local and US terms in 2018, as well as show continued volatility, but we still like them as longer-term positions, from both a valuation and economic growth perspective;

- At current interest rates and credit spreads, the public credit markets continue to look very expensive to us, and our return expectations are muted accordingly. We are nearing the end of the current credit cycle and risks are increasing, especially in the High Yield space (where spreads have increase more than 100 bps since early October), which is often a harbinger of an impending market correction;

- The leveraged loan market (i.e., floating rate bank loans) has seen a decided deterioration in both the credit quality of borrowers and in the covenant structures of the loans – both distinct warning signals.

- Likewise, the traditional Investment Grade bond market has seen a downturn in the average credit rating of borrowers. This could have dramatic implications if/when the next recession hits and corporate revenues decline;

- Many investors increasingly are turning to shorter-duration bond strategies and even cash solutions, which finally have a positive real yield again due to the Fed rate hikes. The curve is so flat that investors simply are not being sufficiently compensated to take on term or duration risk;

- For investors who can access the private markets and handle some degree of illiquidity, we still believe there are better opportunities in the private markets versus the public markets, though investors face compressed premiums versus historical levels, driven by huge investment flows over the past 18-24 months, and performance will be very manager and strategy specific;

- We expected that rising rates, increased volatility, and greater security price dispersion would create a more positive environment for both traditional active managers and for alternative investments. This generally has been true for most of the long-only and hedge fund managers we recommend;

- With most public markets viewed as fairly to fully valued (though valuations certainly have fallen over the past 5-6 weeks), many investors are revisiting the use of alternative investments within their portfolios, both for diversification purposes and as a means of accessing lower-correlated sources of potential return. We continue to believe that hedge funds generally will deliver superior performance than their liquid alternative brethren, because of less liquidity and leverage constraints;

- We have muted our expectations for real assets and the overall commodity complex, due to lower than expected global inflation, slowing demand, falling oil prices, and the strong US dollar;

- While we generally are constructive on the global economy and overall market performance, the public markets are “rationalizing”, and the market volatility we have long expected has materialized. We still believe that the market can move higher over the next 3-6 months, though with increased volatility.

The mid-term elections are behind us (thank goodness) and we can now turn our attention back to the economy and the markets. We have entered a new economic and market regime, and investors need to respond accordingly. Investors should remain calm, stay disciplined, and keep their investment horizons aligned with their long-term financial goals and objectives.

Warm Regards,

Scott Welch, CIMA®

Chief Investment Officer

Dynasty Financial Partners

Source: Bloomberg, Data Analysis, 1/2017-Present

Source: Zephyr, Data Analysis, 1/2017 – Present

Source: Morningstar, Data Analysis, 1/2017 – Present

Past performance shown is model performance shown is no guarantee of future results. The model portfolio performance does not reflect actual trading or any advisory, management, or transaction fees, all of which could result in substantially lower results. This does not reflect the impact that material economic and market factors have had on decision making. You cannot invest directly in an index.

Important Disclaimers and Disclosures

General Disclosures: Dynasty Financial Partners is a U.S. registered trademark of Dynasty Financial Partners LLC ("Dynasty"). Dynasty is a brand name and functions through Dynasty's wholly owned subsidiary Dynasty Wealth Management, LLC, (“Dynasty Wealth”) a registered investment adviser with the Securities and Exchange Commission when providing investment services. A copy of Dynasty Wealth's current written disclosure statement discussing our advisory services and fees is available for your review upon request. This message is intended for the exclusive use of members or prospective members considering joining the Dynasty Network of registered investment advisors for educational purposes. It is not intended for any other persons, clients or other entities. It should not be construed as an attempt to sell or solicit any products or services of Dynasty, Dynasty Wealth or any investment strategy, nor should it be construed as legal, accounting, tax or other professional advice. Information contained herein is based on sources believed to be reliable, but there are no representations or warranties as to the accuracy of such information.

This presentation is for illustrative purposes only. Past performance is not indicative of future results. The information contained in this presentation has been gathered from sources we believe to be reliable, but we do not guarantee the accuracy or completeness of such information, and we assume no liability for damages resulting from or arising out of the use of such information.

The performance numbers displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. The index is unmanaged and does not incur management fees, transaction costs or other expenses associated with investable products. It is not possible to directly invest in an index. All returns reflect the reinvestment of dividends and other income.

Historical performance results for investment indices and/or product benchmarks have been provided for general comparison purposes only, and do not include the charges that might be incurred in an actual portfolio, such as transaction and/or custodial charges, investment management fees, or the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices.

The views expressed in the referenced materials are subject to change based on market and other conditions. This document may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. The information provided herein does not constitute investment advice and is not a solicitation to buy or sell securities.

This content may not be modified, distributed or otherwise provided in whole or in part to a prospective investor or someone considering investing in the portfolio models without the express authorization of the party delivering the presentation. Please note that nothing in this content should be construed as an offer to sell or the solicitation of an offer to purchase an interest in any security or separate account. Nothing is intended to be, and you should not consider anything to be direct investment, accounting, tax or legal advice to any one investor. Consult with an accountant or attorney regarding individual accounting, tax or legal advice. No advice may be rendered, unless a client service agreement is in place.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Dynasty Financial Partners, who reserve the right at any time and without notice to change, amend, or cease publication of the information contained herein. This material has been prepared solely for informative purposes. The information contained herein includes information that has been obtained from third-party sources and has not been independently verified. It is made available on an "as is" basis without warranty. Strategies and investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor

DWM is a registered investment advisor with the Securities and Exchange Commission. DWM serves as a sub-advisor to Dynasty Strategist Portfolios (“the Portfolios”), however DWM does not directly manage client assets within the Portfolios. Any reference to the term “registered investment adviser” or “registered” does not imply that Dynasty or any person associated with Dynasty has achieved a certain level of skill or training.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits