For the first time in 12 years, investors are forced to wrestle with the challenge of navigating a multi-year upward trend in interest rates at both the short and long end of the bond universe. Bond laddering is a timeless strategy used by generations of investors to help manage the risks associated with future changes in market interest rates. But bond laddering has become markedly more difficult to implement in the decade since the financial crisis. In this blog, I explain the potential benefits of bond laddering, and tools that can help with the difficulties.

What is a bond ladder?

A bond ladder is a portfolio of bonds that mature at staggered intervals across a range of maturities. If rates continue to rise, proceeds from each maturing rung of bonds can be reinvested in longer-dated bonds at higher rates. If rates fall or remain flat, bondholders will be forced to accept lower yields only on the portion of bonds that are maturing and being reinvested during the period of lower rates.

One of the greatest benefits of buying a bond and holding it to maturity is that the investor has insulated themselves from the negative effect of rising interest rates on the return generated by that bond between the purchase date and the maturity of the bond.

The effect of diversification on bond ladders

Investors who hold a bond to maturity have locked in their total return, subject mainly to the risk of default. Now, they must consider how to mitigate that default risk: How many different bonds should they own to diversify their portfolios against an economic downturn that weighs on companies’ ability to repay their debts?

Investors who are considering this question often ask us, “How did investment grade corporate debt perform during the 2008-2009 global financial crisis and the recession that ensued?” Diversification plays a role in the answer to that question.

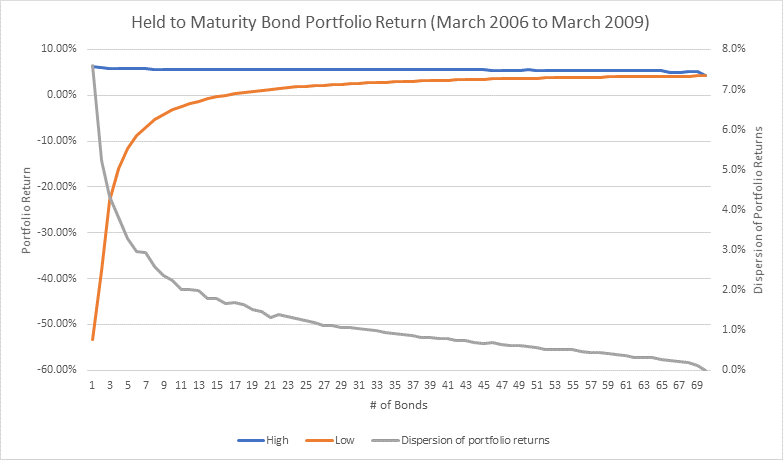

The chart below shows the range of outcomes that would have been generated by hypothetical, randomly selected portfolios of one to 70 bonds held to maturity during the market stress of 2006-2009. The blue line represents the best-case scenario for each portfolio, and the orange line represents the worst-case scenario.

As you can see, a random one-bond portfolio would have generated one of two possible outcomes. Either the bond successfully matures (blue line), returning the stated coupon and par value to the investor, or the bond defaults (orange line), and the investor experiences a significant loss of their investment. The upward path of the orange line nicely illustrates the value of diversification during this particular period of market stress — the return generated by the worst-case scenario gradually improves as the number of bonds held in the portfolio increases. The worst-case and best-case outcomes converge when a portfolio includes all 70 bonds. As you can see, the 70-bond portfolio that included all the defaulted bonds from the sample universe delivered a total return only modestly below the originally stated yield of the portfolio.

Source: Barclays POINT. The study analyzed the bond universe defined by the Bloomberg Barclays 1-5 Year US Corporate Index and selected from the 70 bonds that matured during Q1 2009. These bonds were held to maturity starting in March 2006. For illustrative purposes only.

Bond laddering made easier

While bond laddering may be a helpful tool for investors, it has become markedly more difficult to implement in the decade since the financial crisis — the large banks that were the traditional sources of bond inventory for individual investors have drastically reduced the amount of bonds held in inventory. Furthermore, achieving a desirable level of diversification in a bond portfolio requires significant time and research.

That’s where defined-maturity exchange-traded funds (ETFs) can help. Traditional bond ETFs usually sell bonds well before their final maturity dates and reinvest those proceeds into other bonds. But defined maturity ETFs invest in a variety of bonds that all mature within a defined window of time. At the end of that window, proceeds are returned to investors, who can either spend them or reinvest them into longer-dated funds as rates increase.

In short, defined maturity ETFs help investors build bond ladders quickly and easily, with a range of bonds that can help provide diversification. Investors interested in defined maturity ETFs may wish to consider Invesco’s BulletShares suite of ETFs, which offers the choice of investment grade, high yield or emerging markets bond exposure.

Important information

Blog header image: Sergey Tinyakov/Shutterstock.com

Diversification does not guarantee a profit or eliminate the risk of loss.

The Bloomberg Barclays 1-5 Year US Corporate Index includes US dollar-denominated, investment-grade, fixed-rate, taxable securities with maturities between one and five years.

There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The funds’ return may not match the return of the underlying index. The funds are subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the funds.

Investments focused in a particular sector are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.

The funds are non-diversified and may experience greater volatility than a more diversified investment.

Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.

During the final year of the funds’ operations, as the bonds mature and the portfolio transitions to cash and cash equivalents, the funds’ yield will generally tend to move toward the yield of cash and cash equivalents and thus may be lower than the yields of the bonds previously held by the funds and/or bonds in the market.

An issuer may be unable or unwilling to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Income generated from the funds is based primarily on prevailing interest rates, which can vary widely over the short- and long-term. If interest rates drop, the funds’ income may drop as well. During periods of rising interest rates, an issuer may exercise its right to pay principal on an obligation later than expected, resulting in a decrease in the value of the obligation and in a decline in the funds’ income.

An issuer’s ability to prepay principal prior to maturity can limit the funds’ potential gains. Prepayments may require the funds to replace the loan or debt security with a lower yielding security, adversely affecting the funds’ yield.

The funds currently intend to effect creations and redemptions principally for cash, rather than principally in-kind because of the nature of the funds’ investments. As such, investments in the funds may be less tax efficient than investments in ETFs that create and redeem in-kind.

Unlike a direct investment in bonds, the funds’ income distributions will vary over time and the breakdown of returns between fund distributions and liquidation proceeds are not predictable at the time of investment. For example, at times the funds may make distributions at a greater (or lesser) rate than the coupon payments received, which will result in the funds returning a lesser (or greater) amount on liquidation than would otherwise be the case. The rate of fund distribution payments may affect the tax characterization of returns, and the amount received as liquidation proceeds upon fund termination may result in a gain or loss for tax purposes.

During periods of reduced market liquidity or in the absence of readily available market quotations for the holdings of the fund, the ability of the fund to value its holdings becomes more difficult and the judgment of the sub-adviser may play a greater role in the valuation of the fund’s holdings due to reduced availability of reliable objective pricing data.

The funds’ use of a representative sampling approach will result in its holding a smaller number of securities than are in the underlying Index, and may be subject to greater volatility.

BulletShares High Yield ETFs

The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

BulletShares Emerging Markets ETFs

Non-investment grade securities may be subject to greater price volatility due to specific corporate developments, interest-rate sensitivity, negative perceptions of the market, adverse economic and competitive industry conditions and decreased market liquidity.

The funds may invest in privately issued securities, including 144A securities which are restricted (i.e. not publicly traded). The liquidity market for Rule 144A securities may vary, as a result, delay or difficulty in selling such securities may result in a loss to the fund.

The funds may hold illiquid securities that it may be unable to sell at the preferred time or price and could lose its entire investment in such securities.

Government obligors in emerging market countries are among the world’s largest debtors to commercial banks, other governments, international financial organizations and other financial instruments. Issuers of sovereign debt or the governmental authorities that control repayment may be unable or unwilling to repay principal or interest when due, and the fund may have limited recourse in the event of default. Without debt holder approval, some governmental debtors may be able to reschedule or restructure their debt payments or declare moratoria on payments.

Shares are not individually redeemable and owners of the Shares may acquire those Shares from the Fund and tender those Shares for redemption to the Fund in Creation Unit aggregations only, typically consisting of 10,000, 50,000, 75,000, 80,000, 100,000, 150,000 or 200,000 Shares.

Jason Bloom

Director, Global Macro ETF StrategyJason Bloom is the Director of Global Macro ETF Strategy for Invesco’s family of exchange-traded funds (ETFs). In his role, Mr. Bloom is responsible for providing a macro market outlook across all asset classes globally, in addition to leading the team’s specialized efforts in fixed income, commodity, currency, and alternatives research and strategy. He joined Invesco in 2015.

Prior to joining Invesco, Mr. Bloom served as an ETF strategist for six years with Guggenheim Investments and then River Oak ETF Solutions, where he helped launch several funds focused on both energy and volatility-related strategies. Previously, he spent eight years as a professional commodities trader specializing in arbitrage strategies in both the energy and US Treasury markets.

Mr. Bloom earned a BA degree in economics from Gustavus Adolphus College and a JD from

the University of Iowa College of Law. He holds the Series 7, 24 and 63 registrations.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

| NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE |

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2018 Invesco Ltd. All rights reserved.