There is not much to say about the mid-term elections beyond what has already been said ad naseum. The bottom line is that the outcome was largely as anticipated – the Democrats regained control of the House (though by a smaller margin than expected by those hoping for a “Blue Wave”) and they also made net gains in gubernatorial races, but the Republicans increased their majority in the Senate. The pollsters who so badly called the 2016 Presidential election were at least partially redeemed.

Elections can drive extreme emotions in all directions, but the relevant question for investors is, “What is the impact on US markets?” A handful of charts makes the case that the answer is, “Business as usual.”

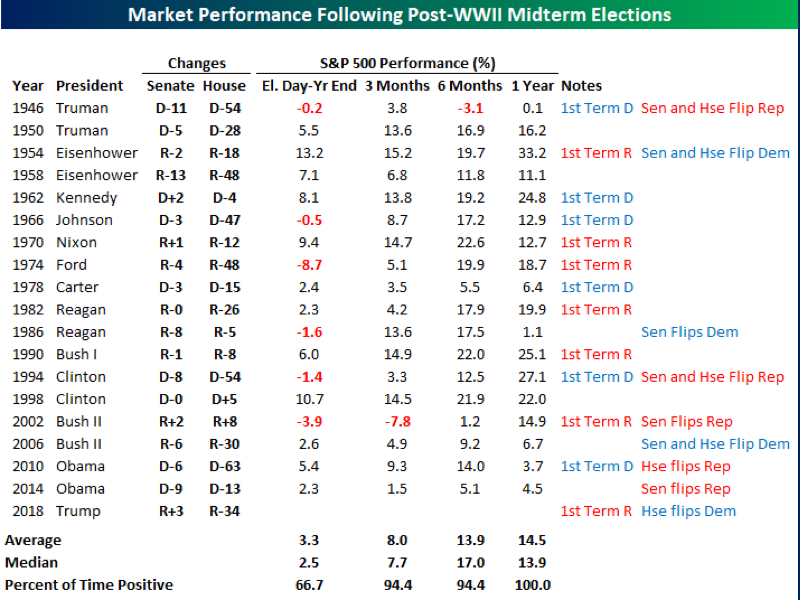

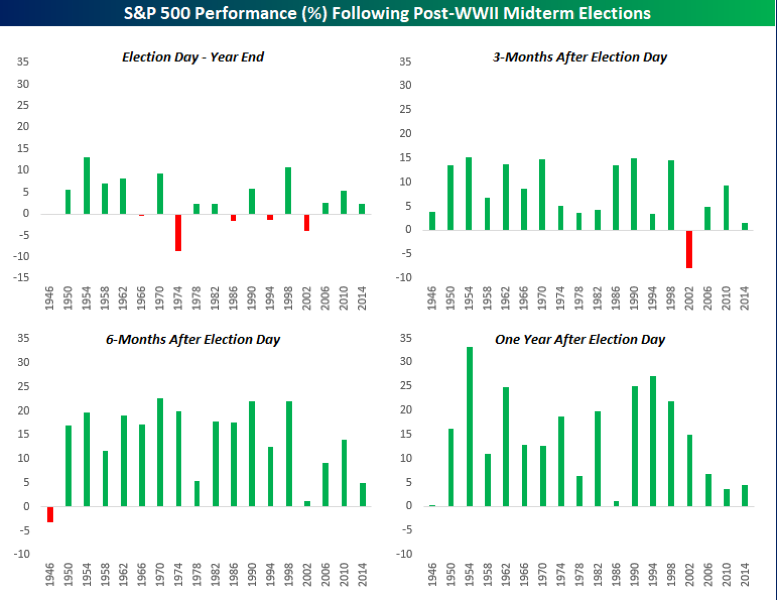

First, from Bespoke Investment Group comes two charts that illustrate the historical performance of the stock market following mid-term elections, breaking it down by which party was in charge:

Quoting Bespoke, “Looking at both the table and charts, from Election Day through year-end, the S&P 500 has seen an average gain of 3.3% (median: +2.5%) with gains two-thirds of the time. While these returns are relatively good, they aren’t necessarily off the charts. Where returns really start to turn positive, however, is in the three, six, and twelve-month windows that follow midterm elections. Three months later, the S&P 500 saw an average gain of 8.0% (median: 7.7%) with positive returns in all but one period. Six months later, the S&P 500 was once again up in all but one period for an average gain of 13.9% (median: 17%). Finally, one year later, the S&P 500 was up every time for an average gain of 14.5% (median: 13.9%).”

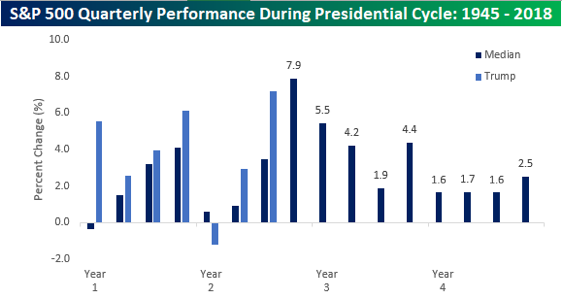

A third chart from Bespoke compares the historical market performance over full presidential cycles to the current market performance under President Trump. History does not dictate the future, but it is helpful to see that markets go up and go down, no matter who is running the government:

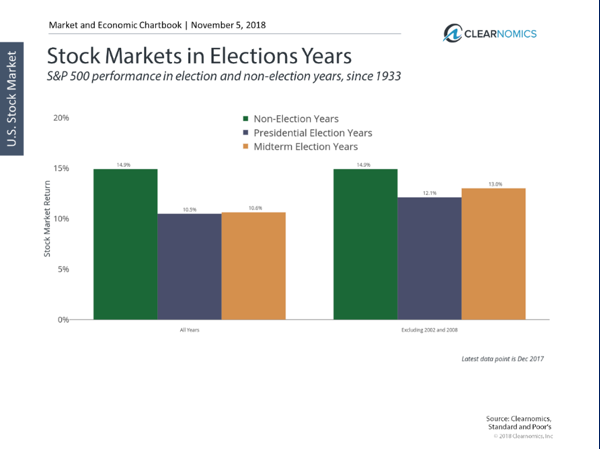

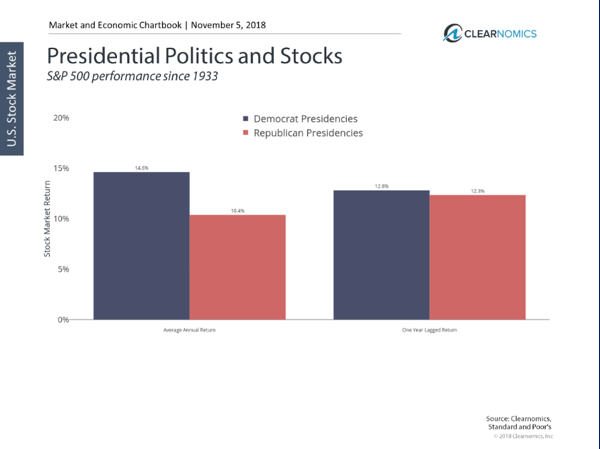

Next, two charts from Clearnomics illustrate it is important to recognize that market performance is not always linked to election outcomes or who is in charge, since that performance might be driven by policies or events that happened months or even years before the election:

The point to be made is that markets may be influenced temporarily by elections, but ultimately what matters is the state of the economy, the state of corporate earnings, the current valuation of stocks, and investor expectations.

As we write this, both the economy and earnings are in solid shape (though expected to decelerate through 2019). Valuations are not cheap, however, and investors should not be surprised by continued volatility going forward as the economy decelerates, earnings slow down, interest rates rise, and the Fed continues to “normalize” its policy.

This is why we consistently recommend remaining diversified and keeping your investment horizon aligned with your long-term financial goals and objectives.

Please do not hesitate to contact us with any questions,

The Dynasty Investments Team

Past performance shown is model performance shown is no guarantee of future results. The model portfolio performance does not reflect actual trading or any advisory, management, or transaction fees, all of which could result in substantially lower results. This does not reflect the impact that material economic and market factors have had on decision making. You cannot invest directly in an index.

© Dynasty Financial Partners

© Dynasty Financial Partners

Read more commentaries by Dynasty Financial Partners