For several months, the din of political advertisements and media coverage has been unavoidable. For all the issues at stake in the midterms, however, the economy is not a source of tension. Markets have done a great job of shrugging off political news and continuing to perform.

We view this week’s election news as another event with limited economic ramifications. Outside of significant legislative actions like tax code changes, the actions of political leaders have little day-to-day bearing on economic activity, and that is to be celebrated. The economy remains fundamentally strong.

Recent volatility has calmed, the yield curve continues to slope upward and the Fed remains on course for continued rate increases. We expect economic growth to taper in the quarters ahead as the economy cyclically ends its outperformance and returns to its long-term potential growth rate of around 2%.

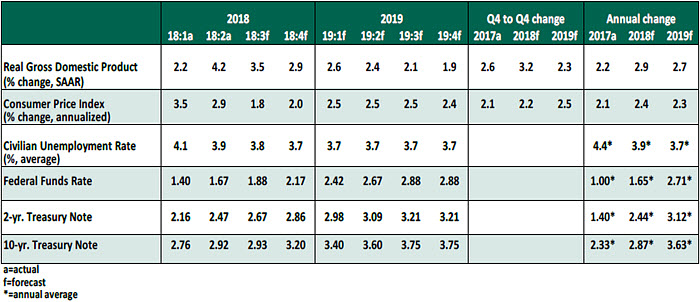

Key Economic Indicators

Influences on the Forecast

- The initial estimate of inflation-adjusted gross domestic product (GDP) growth for the third quarter was 3.5%, a strong reading that follows an exceptional 4.2% growth rate in the second quarter. The most recent reading was weighed down by sluggish business investment, which grew at an annualized rate of only 0.8%.

- Consumer spending was the upside surprise of third quarter GDP results, growing at an annualized rate of 4%. With employment remaining strong as we enter the holiday shopping season, consumer activity is poised to continue to bolster economic growth in the fourth quarter.

- Nonfarm payrolls rose by a strong 250,000 in October, a surprising degree of growth for an economy this far into a recovery cycle. The unemployment rate held steady at 3.7% despite this increase in hiring, demonstrating that discouraged workers are returning to the workforce.

- The labor force participation rate is approaching the levels seen during past expansions. Prime-age (25-54 years old) participation set a cycle high with a seasonally adjusted value of 82.3%; during the last growth cycle of 2002-2007, the rate averaged 83.0%. This recovery has been supported by older workers (over age 55); throughout this cycle, their participation has hovered around 40%, a level last seen before 1970.

- Average hourly earnings grew by 3.1% in October, the strongest wage growth since 2009, suggesting employers are starting to feel the need to increase pay to attract and retain workers. Wage increases were strongest in the transportation and healthcare sectors, both of which are in need of large numbers of trained workers.

- Market volatility characterized the month of October. Some initial blame was placed on the Fed chair’s statement that overnight rates are “a long way from neutral.” Volatility continued on days when no Fed commentary was released, suggesting a wider array of underlying causes. A sustained correction could alter the Fed’s rate trajectory, but recent calm indicates no need for the Fed to support markets.

- We expect another 25 basis point increase to the Fed funds rate at the FOMC meeting which concludes December 11, with further increases in March and June 2019.

- Inflation remains moderate. The personal consumption expenditures (PCE) price index grew 2.0% year-over-year in September, on both a headline and core (excluding food and energy) basis, in line with the Fed’s target. The consumer price index (CPI) grew at 2.3% year-over-year, a decline from recent high readings.

- Rising oil prices have been a recurring theme in 2018, but they appeared to reach a peak of $76 (per barrel of West Texas Intermediate) on October 3, falling gradually to $63 this week. This reduction should benefit energy-consuming industries and help to keep inflation moderate in the fourth quarter.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust