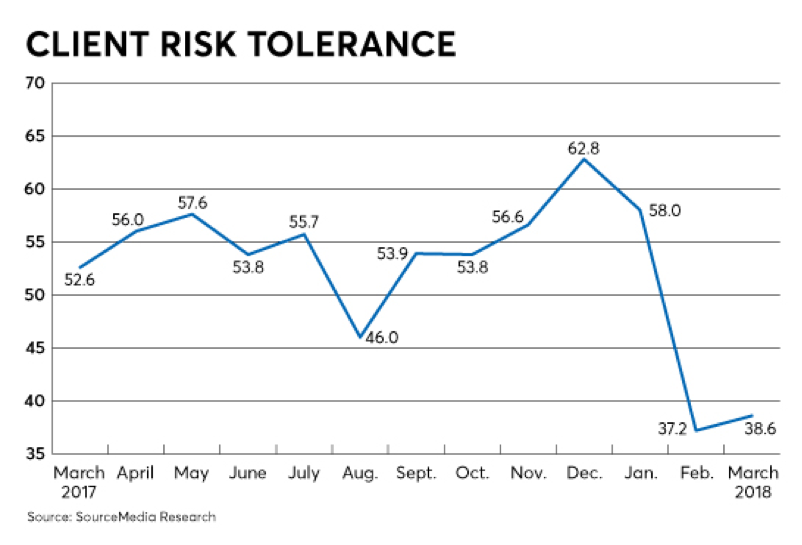

The quarterly Retirement Readiness Index (RRI), which accompanied the latest Retirement Advisor Confidence Index (RACI) from Financial Planning, reflects that investors were significantly more risk averse in the first quarter of 2018 than in the 12 months prior:

Table Source: https://www.financial-planning.com/index/client-risk-aversion-deepens-amid-trade-war-fears1

This finding squares with numbers the global fund tracker EPFR reported in February, 2018, about how investors responded to a surge in market volatility. Approximately $30.6 billion was pulled out of equity funds, $3.7 billion was funneled into bonds, and money-market fund investments ballooned by $45 billion — the largest move to cash ever, based on Bank of America Merrill Lynch analyses dating back to 2004.2

Investors’ heightened sensitivity to market volatility and their sharp shift away from equities is fueled by a number of factors, including an uncertain political climate that encompasses the imposition of certain tariffs and escalating tensions around worldwide trade wars.1 The unpredictability of this environment has investors seeking ways to control their finances, which at least partially explains the lure of cash holdings. Investopedia contributor Lisa Smith sees keeping cash as an antidote to steep equities losses because “Cash can be seen, felt and spent at will, and having money on-hand makes many people feel more secure.”3

While keeping cash on-hand is a surefire way to avoid market losses, Smith is also quick to point out that the mental “feel good” cash provides in the short-term also undermines long-term strategies. Investments may lose money on paper at some point as the market falls, but an inevitable market turnaround will often bring the investor back to break-even, or maybe ahead of the game. Cash cannot do that. Any losses — including inflation erosion — are permanent, with no chance for making up the difference.3

Which brings us to how to help your risk averse clients who may be inclined to pull out of the market when volatility spikes. Holding cash is a limited and possibly counterproductive long-term solution. Fixed annuities offer guarantee and predictable returns, but could yield lower returns.4

Risk control annuities, on the other hand, provide clients with an opportunity to remain in the market largely on their terms. They participate with you in customizing investment upside potential with downside protection that fits their individual circumstances — a personal risk/reward balance that provides more confidence in riding the market highs and lows, and a greater sense of control over their finances and future.

SOURCES

1https://www.financial-planning.com/index/client-risk-aversion-deepens-amid-trade-war-fears

2https://www.marketwatch.com/story/stock-market-tumble-sends-investors-fleeing-equity-funds-2018-02-09

3https://www.investopedia.com/articles/basics/09/cash-is-king.asp

4https://www.annuitieshq.com/annuity-guide/types-of-annuities/fixed-annuities-safe-investment/

MGA-2117046.1-0518-0620