Weighing the Week Ahead: What do the Mid-Term Elections Mean for Financial Markets?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe have a huge economic calendar. While employment data will get most of the attention, there are also important reports on ISM manufacturing, personal income, PCE prices, consumer confidence and auto sales. Earnings season continues with another big week of reports. In normal times these topics would provide plenty to think about. Nowadays, none of this seems important. If the stock decline continues at the start of the week, that will take center stage. We’ll probably get another “crisis” prime-time feature from CNBC, bumping Shark Tank or Jay Leno.

If things calm down a bit, expect to see the punditry turn attention to the US mid-term elections, asking:

How will the mid-term elections affect financial markets?

As always, WTWA does not advocate particular candidates. As citizens, we should all do what we think is correct. As investors, we should be politically agnostic. That does not mean blind and deaf. Elections have an impact on the markets overall as well as individual stocks. That should be our focus.

Last Week Recap

In my last edition of WTWA I suggested to expect a week of wondering what could go wrong, mostly fueled by misperceptions. That is exactly what happened, with daily discussions of the “message” of the market, telling us something we otherwise would not see. There may well be more of the same, but this week will have even more competition for attention.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring the futures chart from Investing.com. The image posted here shows a static view. If you go to the site, you can check out the news at various points during the week and adjust the view in many other ways. Since futures trade when the stock market is closed, you can also see that trading.

The market declined 3.9% and the weekly trading range was 4.8%. Both were extremely high. The VIX implied volatility measure remained higher than the actual results. I summarize actual and implied volatility each week in our Indicator Snapshot section below.

Noteworthy

There is a fascinating update of the four-year old “trolley problem.” The original question asked whether you should switch a speeding, runaway trolley from one track (with five people in the path) to another (with only one potential victim). The new study, with the inclusion of self-driving cars, raises questions of great interest without obvious answers. Those interested might also consider the variations from different cultures. For example, which countries give emphasis to the elderly?

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. This week reflects some softening in all three time frames reported, although the nowcast remains a “weak positive.” NDD concludes, “An economic slowdown looks baked in the cake, with the issue of whether it leads to outright recession in a year or so still outstanding”.

When relevant, I include expectations (E) and the prior reading (P).

The Good

-

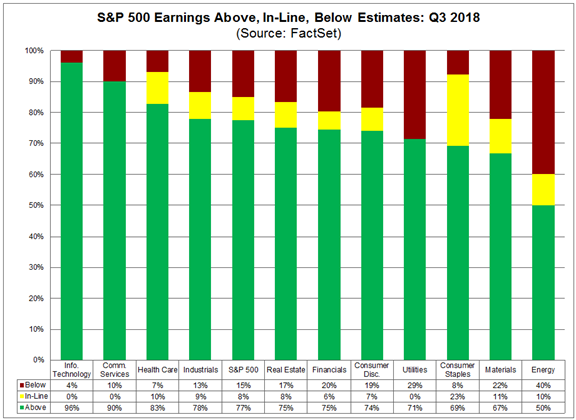

Earnings season showed continuing strength. FactSet reports as follows (with more facts and figures in the full report):

Companies are outperforming recent averages on the earnings side and performing in line with recent averages on the revenue side. In terms of earnings, the percentage of companies reporting actual EPS above estimates (77%) is above the five-year average.

Here is the record by sector.

- Durable goods increased in September by 0.8%. E -1.8% P 4.6%. Subtracting transportation, the report was a small miss. (Steven Hansen, GEI) takes a deep look, with interesting measures and comparisons.

- Pending home sales increased 0.5% in September, beating expectations for a decline of 0.2%. P -1.9%. (Calculated Risk)

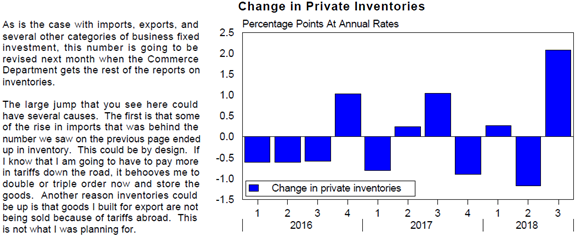

- Q3 GDP registered growth of 3.5% in the first estimate. This was a decline from 4.2% in Q2, but a solid number that beat expectations. Looking a bit more deeply, some analysts had less enthusiasm. Economy “deniers” jumped on the increase in inventories as a sign of hidden weakness in the report. I have often commented that inventories are one of the most spinnable statistics. Bob Dieli had his usual “no spin” take:

He also notes that the tariff effects are just beginning to show up.

The Bad

-

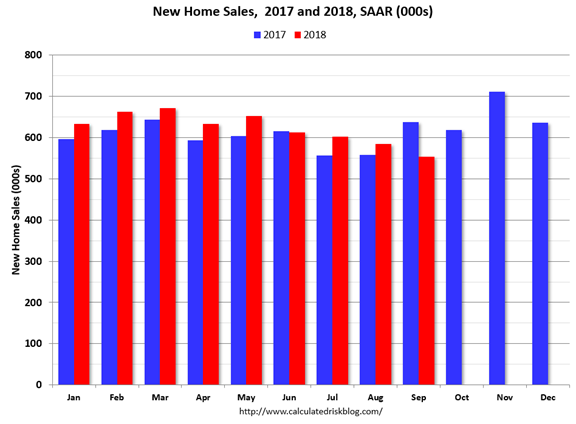

New home sales disappointed at a SAAR of 553K. E 625K P 585K revised down from 629K. Calculated Risk concludes, “It is not time to panic – or start looking for a recession – but this was a very weak report.”

-

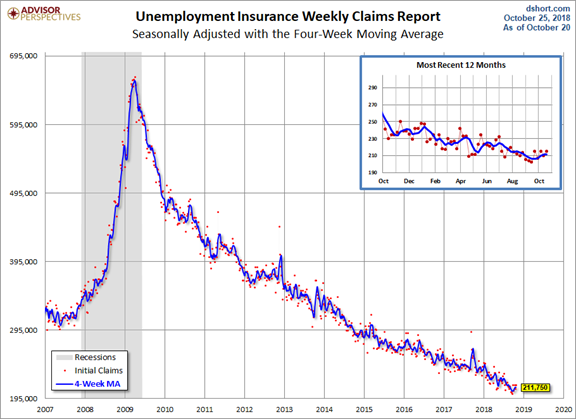

Initial jobless claims up-ticked to 215K. E 211K P 210K. Like many other data points, this is a very good level, but a little weaker than recent reports. Jill Mislinski provides analysis as well as this chart:

-

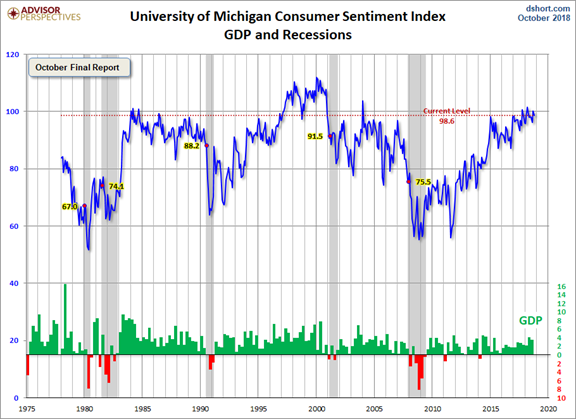

Michigan sentiment sagged a little to 98.6. E and P both 99.0. Jill Mislinski has the full story along with the great charts we have come to expect. She also quotes survey chief economist Richard Curtin:

Importantly, stock price declines, rising inflation and interest rates, and the negative mid-term election campaigns, have not acted to undermine consumer confidence. Needless to say, consumers are not immune to these negative factors. The data only indicate that the tipping point toward escalating pessimism has not been reached. This resilience was primarily due to the prevailing belief that the economy would produce robust job growth during the year ahead, even if overall wage growth remained dismal.

The Ugly

Bombs. More shooting of innocents, even while worshipping. I am deeply saddened by the violence, and by the circumstances and reactions. What does it say about our ability to debate and decide, essential to democratic processes?

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

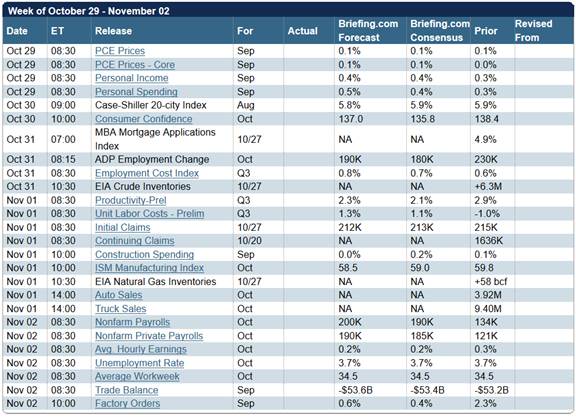

The Calendar

The calendar is among the biggest we see with a focus on employment. I am also watching the important reports on PCE prices (the favorite Fed inflation measure), personal income and spending, consumer confidence, and auto sales – especially Ford F150’s. The ISM manufacturing index is one of the best of the reads on current conditions. There will be plenty of earnings news.

Briefing.com has a good U.S. economic calendar for the week (which is why I am a subscriber). Here are the main U.S. releases.

Next Week’s Theme

If the week beings with more market declines, expect to see that subject dominate the news. If not, the punditry is running out of time to analyze the 2018 mid-term elections, and many posit a link to financial markets. I expect many to be asking:

What might the 2018 mid-terms mean for investors?

Please remember – others take up advocacy. Our mission is to analyze what this means for our investments. As always, I’ll offer an overall guide to the potential effects, including links for those who want to do further research. I save my own conclusions and ideas for the Final Thought.

A Digression about the Current Market

Financial news continues to be very good, and financial markets are “ugly” in the terms of many veterans. The news has everyone worried, especially since there is no satisfying explanation. Briefing.com’s weekly stock analysis puts it very well:

The thrust of matters is that the market is worried about growth. That might sound odd considering it was revealed on Friday that third quarter real GDP increased at an annual rate of 3.5%, yet it is the sobering message that has resonated loud and clear in the stock market’s price action.

The worry isn’t about the growth that was just left behind. Rather, it is about the growth to come — or perhaps lack thereof.

There are various explanations regarding the causes of the stock market’s correction: the adverse effect of a strong dollar; the slowdown in China and other foreign markets; tariff issues, raw material price increases; political uncertainty; diplomatic uncertainty; price increases for consumers; rising interest rates; and profit margin pressures.

Ultimately, they all feed into the one thing that matters most for the stock market: earnings growth.

WTWA readers should not have been very surprised about last week’s market move. For the last month I have analyzed the potential effect of interest rates,corporate earnings, and market mythology. I certainly did not predict this as the specific time for a correction, but I have highlighted the deviation between trader sentiment and the realities of earnings growth and the economic cycle. If you are a trader, you need to guess the psychology of other traders. If you are an investor, you should stick to your own conclusions about the value of companies you own, ignoring the emotional Mr. Market. If you have chosen an “all-weather” portfolio, you should just have a hurricane party. Don’t read the news.

I’m not going to review all the dumb explanations offered for last week’s selling. I monitor them because it is my job. I don’t recommend it! Those who have been bearish forever embrace the move as validation of their theories. Those who get on TV and have a microphone thrust in front of them, seek the “message from the market.” There are plenty of newly-minted experts on recession. Explanations about “delayed reactions” or taking a while for the message to sink in are particularly lame. If you believe the market is efficient, it does not take three weeks to digest whatever it is you think the Fed Chairman meant as a new policy signal.

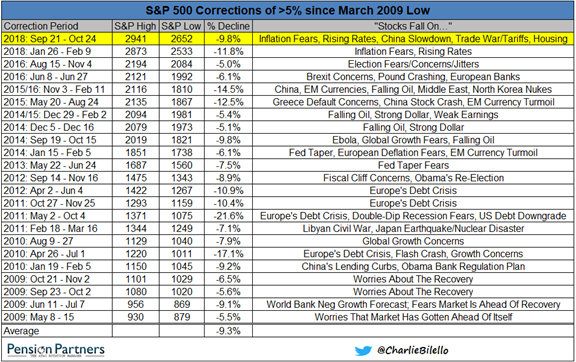

Charlie Bilello (Pension Partners) notes the insatiable human desire to know the reason, and reminds us of the futility of this approach.

The message of the markets is about what traders think might happen. It does not have a good record for predicting recessions, notes Ben Carlson, who provides the evidence below:

Many of the recession forecasters have a valid indicator but are just itching to pull the trigger. Leading business cycle expert Dr. Robert Dieli calls this forecasting the forecast. It can be very costly, since the “boom” phase of the business cycle is often very profitable. He believes that we are almost there.

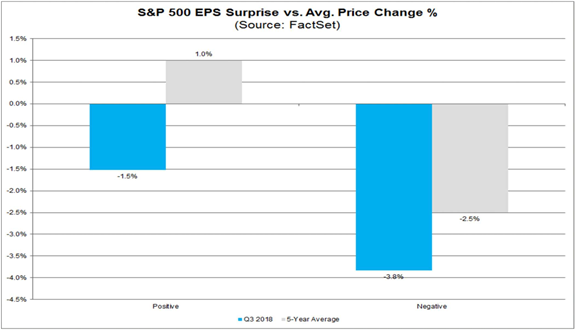

The result of this is dramatically shown by John Butters of FactSet. He tracks stock reaction to earnings surprises. In this season, even a positive surprise (and these estimates did not get reduced in advance) has not helped the stock reaction.

I have seen this story before. No one knows what will happen next week, but eventually stock prices reflect corporate earnings, which reflect economic conditions. I was buying last week, but I am not worry-free. More in the Final Thought.

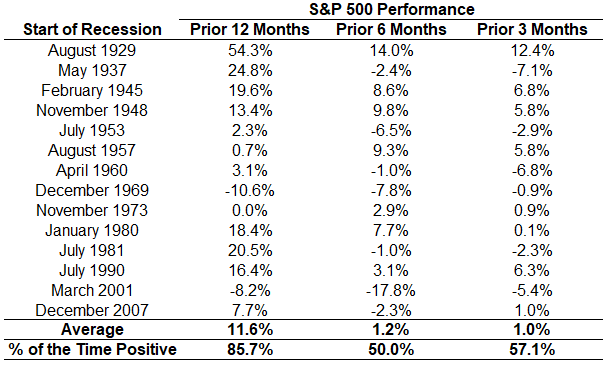

The Mid-Term Election

In this section, I will intersperse some ideas in italics, an approach that some readers have encouraged for clarity and flow. Let’s split this into three different components: who will win, the impact on markets, and the impact on individual stocks.

- Who will win? The leading sources see a 6-1 chance for Democrats to take control of the House (84.5%), and a 5-1 chance (83.2) for Republicans to maintain control of the Senate. Since people take high percentages and turn them into absolute, 100% predictions, most are looking for a split Congress. If the two events were independent, the chance of both occurring is about 70%. The chance of the Dems sweeping would be about 15%. Any combination is a realistic possibility. Much depends upon turnout, especially among base voters for both parties. In the Senate the Democrats have more seats to defend and few vulnerable targets. Here are the key sources I follow: https://fivethirtyeight.com/ and http://www.centerforpolitics.org/crystalball/. Both offer commentary on individual races and provide plenty of sources and references. I do not have an opinion or forecast, other than finding the best experts.

- What will be the market impact? Most market observers see a Dem sweep as negative and a split Congress as not important. Darren Fonda (Barron’s) opines that it will not make much difference. The basis is historical as well as an opinion about trade tensions with China. A Barron’s cover story from a month ago highlighted a panel with a different conclusion. The key questions relate to the potential for tax policy changes, a new course in regulation, attention to the deficit, and changes in Obamacare. The participants speculated on various policy themes. [I did not find the policy speculation to be very convincing. Democrats will not be able to repeal tax cuts or offset regulations. Republicans will remain unable to repeal Obamacare. I see two key considerations. First, if Democrats win the House they will take over the chairmanship of all committees. This gives them power to convene hearings and issue subpoenas—potential for far-reaching effects. Second, it might force some cooperation on budget issues and problems like immigration and infrastructure policy.]

- Can we find winners and losers among individual stocks? The Barron’s panel covered this topic, and Ben Phillips of EventShares (PLCY) had a leading role, providing more specific ideas than the other members. He highlighted potential regulations for policy-sensitive companies including Amazon (AMZN), Alphabet (GOOG), Facebook (FB), and Twitter (TWTR). He also suggested infrastructure stocks that would benefit from a stronger Democratic showing. EventShares has a summary of specific ideas for each of the three key resulting scenarios. [My sense is that a Democratic House might challenge some of the Administration’s asserted powers on tariffs. This has traditionally been a legislative process. The “national security” exemption seems to be stretched in many cases].

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

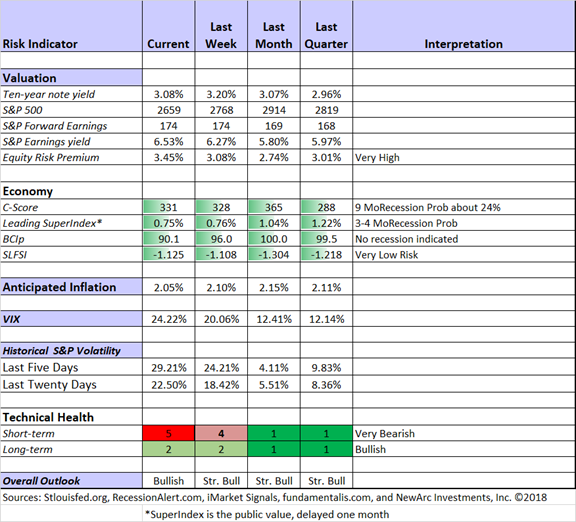

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

Short-term trading conditions have moved to our highest alert stage. The identification as “very bearish” is a reaction to volatility, not a prediciton of a continued decline. There is always a risk/reward balance to consider in your trading. Sometimes it is just better to go fishing (or ice fishing if you live in Mrs. OldProf’s home town).

When conditions are technically challenged, we watch trading positions even more closely. Each of our models has a specific exit strategy. The technical health rating may drop enough for a complete trading exit. It got close to that level this week, and remains there.

Long-term trading has also dropped a point on a technical basis.

And finally, fundamental analysis, the key for investors, has grown even stronger. Earnings are great, prices are lower, and there is even less competition from bonds.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession. Here is the latest chart on the Business Cycle Index.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Guest Commentary

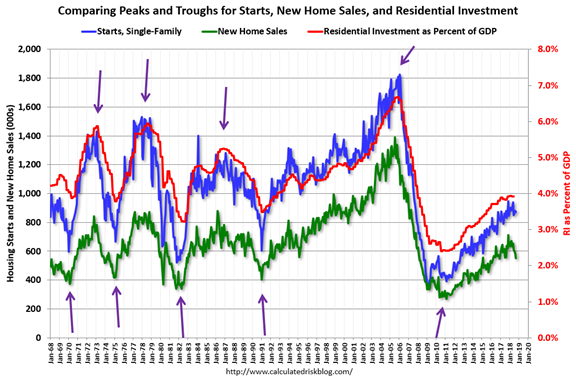

Bill McBride explains how to use housing data as an indicator for the overall economy. He shows the relationship among starts, new home sales, and residential investment as a percentage of GDP.

He notes that there is sluggishness mostly due to multi-family residential, and that a downturn in the RI % from current low levels would be surprising. Read the full post to see the relationship between new home sales and the overall economy. See also his featured guest commentary with Brad Hunter, a leading economic forecaster for the homebuilding business.

Insight for Traders

Check out our weekly Stock Exchange post. We combine links to important posts about trading, themes of current interest, and ideas from our trading models. This week we asked traders: Will you adjust your strategy or go down with the ship?

Our trading models all have some method for limiting losses. If you are a trader, you should too. We also shared advice by top trading experts and discussed some recent picks from our trading models. Our ringleader and editor, Blue Harbinger, provided fundamental counterpoint for the models, all of which are technically-based.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility.

Best of the Week

If I had to pick a single most important source for investors to read this week it would (once again) be this great advice from “Davidson” via Todd Sullivan. Here is the key point:

The current environment appears scary much like a ship in a storm without a rudder. Events seem to come out of nowhere from unanticipated directions. Each new headline threatens to topple what seemed positive consensus a few weeks past. Positive earnings reports are ignored adding to the appearance the markets have become illogical and no headline provides comfort. Pessimistic shifts in market psychology when positive economic signals abound are specially disconcerting. But, fortunately the markets are littered with many such events. The many times short-term panics have occurred during positive economic signals define how markets operate. Market psychology impacts short-term market prices but is not driver of long-term economic trends.

He notes that several policy shifts may well provide a further spur to economic growth. So why the stress?

One should be specially aware that most investors are Momentum Investors at any point in time. Momentum Investors believe that price trends predict economic activity. Some even believe price trends determine future economic activity. Investors are generally wrongly focused on price trends and have produced a long history of selling into panics and buying at market tops. If one observes closely when markets respond to reported events which have been long in the making, markets are highly inefficient and illogical. The belief that markets track Fama’s “Efficient Market Theory” arises from a ‘Top Down’ perception which misses the fact that prices adjust quickly after the headlines.

Turning to the business cycle, he looks at a rate spread indicator and a business cycle indicator – an approach I advocate each week. Here is a look at the business cycle.

Read the full post for more detail and his investment thesis.

Stock Ideas

Chuck Carnevale takes up an important and common question: How Many Stocks Should I Own? He draws upon experts before drawing his own conclusion.

As promised last week, I acted upon an idea from this section. I bought IBM and sold a near-term call against the position. (Boost your Dividend Yield –IBM) The trade itself is simple, but the rationale of the overall strategy is more challenging. I plan to write up several trades of this type in future weeks.

Looking for a wide moat? Morningstar says that Polaris (PII) fits the bill.

Stone Fox Capital warns against overreacting to AT&T’s (T) lower subscriber numbers.

Brian Gilmartin recommends buying dips in Microsoft (MSFT) an old tech giant that is “successfully transforming its business model.”

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich’s Asset Allocation Daily is consistently both interesting and informative. Each week he highlights stories of interest for both advisors and investors. He also provides insightful commentary on important topics. Be prepared for something that cuts against the grain!

This week he has a thoughtful analysis of artificial intelligence, sparked by Brenda Jubin’s review of Prediction Machines: The Simple Economics of Artificial Intelligence by Ajay Agrawal and colleagues at the University of Toronto. Using Amazon as an example because of the high use of AI, he considers the implications for the labor market. This is not just a matter of lost jobs, but also displacement, underemployment, and the gig economy.

Abnormal Returns is an important daily source for all of us following investment news. His Wednesday Personal Finance Post is especially helpful for individual investors. As always, there are several great choices. I especially liked the piece from Mike Piper, who explains why buying an annuity with a “period certain” provision is a mistake. It is just another example of how such contracts have been crafted to meet a buyer’s concern – but without an assessment of the actual cost. Mike takes you through the numbers.

Watch out for…

Noodles & Company (NDLS) warns Stone Fox Capital. Some big investors “want out quick following the (recent) turnaround.” They are also negative on Caterpillar (CAT) because of decelerating sales.

Final Thought

On the question of “what next?” I have two thoughts about when the disparity between stock prices and fundamentals might end:

- Two of my favorite sources spotted something this week. David Templeton (HORAN) notes that the VIX curve is now moving toward contango. You don’t hear this on TV, since none of the people there could explain the sentence, much less the implications. He notes that a major difference between the near-term and three- month VIX, with the former registering higher values, is a positive signal for equity markets.

Ralph Vince (at Daily Speculations) writes:

And at this very minute, the ten day correlation between VIX and he S&P 500 is -.97. VIX is running a positive carry both to cash and futures months more distant for any given futures month.

It is a condition which, if persists, allows a portfolio manager to in effect get a completely free lunch via Markowitz. Either stocks go up in the not-too-distant future, or the carry on VIX goes negative again (which occurs….when stocks go up).

- My second idea is tied to expectations for Trump policy moves. Many of the things currently troubling the markets relate to trade policy – more inflation and a reduction in growth. Other favorite agenda items like immigration and another round of tax cuts are also troubling. We are seeing this both in the earnings reports, and in the reaction to those reports. The campaign background has encouraged both parties into extreme positions when we really need some cooperation. Regardless of the election outcome, we will have a better chance to resolve the most important economic issues. A recent IMF report on the effect of tariffs looks at 151 countries over 51 years. Tariffs hurt productivity and economic growth, while raising prices. Put another way, an extensive study shows that economic theory is correct.

We have been living through what I call a reality show about learning economics. The big administration supporters are feeling the economic pain. (Barron’s) I expect deals to be done and victory declared once the election is behind President Trump. Given recent declines, my estimate of the trade effect on the market is about 15%.

So What Next?

Many investors have been out of the market, planning to find a good opportunity to get back in. This is a poor approach. Making “all-in” decisions is much more difficult than choosing a reasonable adjustment to your allocations.

If you are a long-term investor, and have been waiting for people to get fearful, it is time to get more aggressive.

I’m more worried about:

- Frightened investors. Will those who have “all weather” portfolios stay the course? Will those who have been waiting for palpable fear start to buy? I fear for investors with no compass and the ripple effects on others.

- The polarizing election effects. Congress is on recess. It is a strange idea, but maybe the market should close until they come back! (Mrs. OldProf informs me that no one will recognize my intended humor).

I’m less worried about:

- Earnings growth. It is a strong positive, even if not recognized right now.

- The Fed. The Fed speaking circuit provides a more balanced take on upcoming policy. I expect another hike in December (as does the market), but economic data will factor into future moves.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits