Will You Still Love Me Tomorrow?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTonight you're mine, completely

You give your love so sweetly

Tonight the light of love is in your eyes

But will you still love me tomorrow?

Is this a lasting treasure

Or just a moment's pleasure

Can I believe the magic in your sighs

Will you still love me tomorrow?…

I'd like to know that your love

Is a love I can be sure of

So tell me now and I won't ask again

Will you still love me tomorrow?

(From “Will You Still Love Me Tomorrow?” by Carole King and Gerry Goffin, 1971)

I gave a letter to the postman, he put it in his sack

Bright and early next morning, he brought my letter back

She wrote upon it

Return to sender, address unknown

No such number, no such zone

We had a quarrel, a lover's spat

I write I'm sorry but my letter keeps coming back

So then I dropped it in the mailbox and sent it special D

Bright and early next morning it came right back to me

She wrote upon it

Return to sender, address unknown

No such person, no such zone

(From ”Return to Sender”, by Otis Blackfield and Winfield Scott, performed by Elvis Presley, 1962)

The phrase “October Surprise” usually refers to a sudden, politically-motivated “reveal” about the opposition candidate just prior to an election. The hope is to announce negative news about the opposition candidate just when voters are finally focusing on who and what they want to vote for (or against).

This year, there very well may be a political “October Surprise”, though as we write this we are running out of days in which one may occur (perhaps the recent spate of “pipe bomb” deliveries to prominent Democrats qualifies, though the actual sender of those bombs remains highly questionable).

But, for many investors, this October certainly has been a negative surprise, as most major markets have sharply corrected over the course of the month, with the S&P 500 index, for example, giving back in roughly three weeks roughly half of its YTD gain through the end of September. And Small Cap stocks have fared even worse. As of the end of September, the Russell 2000 (a commonly used index for Small Cap stocks) was up more than 11%. As we write this, that index now has slipped into negative territory.

But how big of an “October Surprise” is all of this, really? Many of the equity market’s worst disruptions occurred in October – The Panic of 1907, the Great Depression market crash of 1929, “Black Monday” in 1987 and, of course, the Great Financial Collapse of 2008, though the final (but by no means only) catalyst for this event – the collapse of Lehman Brothers – occurred in mid/late September. Not all bad market events occur in October, of course, and in many cases these crashes were the final outcome of a series of events that took place over many prior months or even years. But October gets a “bad rap” for sure, and with some justification.

To be clear, we are not suggesting that the market corrections of this past month remotely resemble those historic seismic disruptions (although it may feel like them to complacent investors who have enjoyed years of central bank-manipulated positive capital markets action). In fact, we’ve been suggesting for months that just such a correction was due – we do not have a crystal ball and never “time stamped” when this correction might occur, but we believed it would at some point. To quote from our July Monthly Market Commentary:

Look for volatility to increase as the (trade) rhetoric heats up and we work our way through the typically slow summer trading months. As has been the case for the past several years, September and October look to be much more “interesting”, and it is not too early to start thinking about how to allocate your portfolios accordingly. (emphasis added)

Let’s review some of the factors that contributed to this most recent edition of an “October Surprise”:

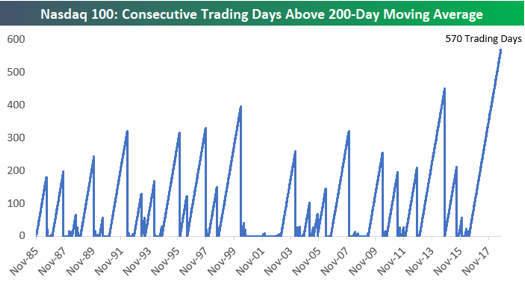

- The markets (especially the Tech sector), were remarkably complacent for months. See, for example, the following chart from Bespoke Premium that illustrates just how consistent the Tech rally had been in comparison to historical performance. If you believe (as we do) in even a modicum degree of market mean reversion, the recent pullback is no surprise, and perhaps even long overdue.

- Market valuations are inversely correlated to interest rates and volatility. Put differently, valuations tend to go up when interest rates and volatility are low, as they have been for much of the past 7-8 years. But they also tend to decrease when interest rates rise and/or when volatility increases.

Interest rates have risen steadily over the course of 2018 (albeit fairly slowly), and even with the recent rally the 10-year Treasury rate now trades consistently above 3.00%:

Likewise, volatility (as measured by the VIX) has also increased recently, after trading at historically low levels for most of the past two years (with the exception of the last market correction we experienced in late January of 2018):

- Perhaps most importantly, the stock market is a discounting mechanism – it focuses less on current market conditions (which are already priced in) and more on future expected conditions. The US economy is humming right now, and corporate earnings are fairly strong. But, as we increasingly get through the Q3 reporting season in the US, we see a troubling trend – the earnings “beat rate” remains strong, above 70%. But the revenue “beat rate” has fallen off dramatically (currently below 60%). In other words, companies are engaging in financial engineering to drive earnings growth, but top line revenue growth is decelerating, and the markets are reacting accordingly.

- Furthermore, while the current US economy is doing well, there are distinct signs that the effects of tax reform and fiscal stimulus legislation of late last year and early this year are beginning to wear off. We are not suggesting imminent recession, simply a deceleration of growth and, again, investors are reacting accordingly.

- The outcome of the upcoming mid-term elections in the US, combined with ongoing trade uncertainties, continue to contribute to a fair level of market uncertainty.

We have been suggesting for several months that market valuations are expensive and that market complacency was high. In this “perfect storm” of rising rates, increased volatility, expected deceleration of economic growth and corporate earnings, and exogenous issues such as the elections, trade negotiations, and Middle East tensions, no one should be surprised that the market (finally) reacted.

With that as a backdrop, looking out over the current economic and investment landscapes, here is what we see.

The Current Economic Landscape

The global economy continues to grow, though with distinct signs of deceleration, especially outside the US:

- The consensus estimate for Q3 GDP growth in the US is now a solid 3.4%. That growth is then expected to decelerate to 2.9% in Q4, bringing overall 2018 GDP expectations to 3.1%; (source: The Wall Street Journal);

- This GDP forecast remains sensitive to ongoing trade negotiations, political tensions in the Middle East following the assassination of journalist Jamal Khashoggi, and the outcome of the upcoming mid-term elections here in the US;

- On the election front, the polling averages from Real Clear Politics suggest (a) the Republicans will retain control of the Senate (and perhaps even pick up a seat or two) and (b) the Democrats will regain control of the House, though earlier suggestions of a “blue wave” election have subsided and even Democrats acknowledge that this is likely to be a very close election;

- Both US manufacturing and services remained strong in September, with the PMI (manufacturing index) coming in at 59.8, down slightly from 61.3 in August, while the NMI (non-manufacturing index) jumped to 61.6 in September, up from 58.5 in August; any reading above 50 is considered expansionary. The manufacturing index has now been in expansionary territory for 113 consecutive months, while the non-manufacturing index notched its 104th consecutive expansionary month (source: Institute for Supply Management);

- One possible future trouble spot for the US economy is a marked slow-down in the housing sector, as permits, housing starts (especially in the multi-family sector), and affordability have all trended downward for several months (source: Bespoke Premium);

- We continue to believe that inflation will increase slowly over the rest of this year, but will remain somewhat dampened by (1) continued slow (but positive) wage growth; (2) a generally strong dollar; and (3) a decelerating global economy (ex-US), which will dampen demand. As such, we continue to believe that inflation does not yet constitute a primary risk to economic growth;

- As expected, the Fed raised interest rates in late September, and there is a strong consensus that it will do so again at its December meeting. President Trump does not agree with current Fed policy, and has made it clear that he wants the dollar weaker and interest rates kept low (he is unlikely to achieve either objective). Should the economy slow down or the current market downturn continue, it is a safe bet that Trump will hold the Fed responsible;

- The yield curve has risen steadily over the past several months but remains very flat, as the Fed raises rates on the short end but the long end remains “tamped down” by high demand and a lack of inflation fears. As of late October, there remains less than 30 basis points difference between the yield on the 2-year and 10-year Treasury.

- We saw a brief rally in the longer end of the curve due to the market disruption in early/mid October, but the 10-year rate remains above the psychological barrier of 3%, and we repeat that we do not anticipate (or fear) an inverted yield curve – should one occur, we believe it will be because of investment flows and Fed actions, not a harbinger of an imminent recession;

- The US dollar generally remains strong. It weakened slightly against the euro through October, but continued to strengthen against both the Japanese yen and (especially) the Chinese yuan;

- The Q3 earnings season is underway, and we are seeing a mixed bag of results. Of the roughly 70 S&P 500 companies that had reported through the third week of October, we saw a 20% increase in earnings on 7.8% higher revenues. More troubling, however, is that while the earnings “beat rate” remains strong, above 70%, the revenue “beat rate” has fallen off dramatically (currently below 60%). This simply means that companies are using financial engineering (stock buybacks, etc.) to generate earnings growth versus organic top-line growth. Further, the number of companies issuing reductions in future earnings guidance is increasing. So, while the numbers certainly remain positive, growth is still expected to decelerate as we head into 2019, with earnings growth of 9.7% and revenue of 5.1% (sources: Zachs Earnings Report and Bespoke Premium);

- Manufacturing across the Eurozone remains expansionary, though the Markit Manufacturing index fell to 52.1 in October, versus 53.2 in September, a continuation of a general YTD decline. Likewise, the Services index fell slightly to 53.3 in October from 54.7 in September – the slowest services expansion rate since October 2016 (source: TradingEconomics);

- Eurozone unemployment edged down to 8.1% in August (the most recent reading), from 8.2% in July, and it remains at its lowest level since December of 2008. Annualized inflation edged up to 2.1% in September, up from 2.0% in August (source: TradingEconomics);

- Japan’s GDP rose 3% (annualized) in Q2, after a decline in Q1. The expansion was driven by strong consumer and business spending and was the strongest reported growth rate since Q1 of 2016. The consensus estimate for 2018 GDP growth is 1.7% (source: TradingEconomics);

The Dynasty Economic & Market Outlook:

- The global economy continues to expand, though there remains a distinct “desynchronization” of growth. The US economy shows continued growth, with perhaps some yellow lights beginning to flash (e.g., housing), and there is an expectation of a decelerating economy through 2019 as the effects of fiscal stimulus and regulatory and tax reform begin to tail off. At the same time, the rest of the world appears to be decidedly decelerating – still expansionary, but slowing down (especially in China);

- US Inflation is trending higher, but we maintain our belief that it (as of yet) does not represent a problem for continued economic expansion. Wages in the US are increasing slowly, oil prices have actually fallen over the past 5-6 weeks (despite tension in Saudi Arabia over the assassination of journalist Jamal Kashoggi), and overall commodity prices remain repressed by slowing demand and the generally strong dollar. Outside the US, inflation simply is not a problem, despite the rise in oil prices;

- In the US, tax and regulatory reform and fiscal stimulus continue to win the ongoing economic tug-of-war against monetary tightening, and continue to pull future consumption forward as consumers and small business owners lean fully into the ongoing recovery. That said, the Fed has a laid out a fairly aggressive tightening program over the next 12-15 months and there perhaps is a risk it will “overshoot” in its tightening and choke off the expansion. As the cliché goes, “Economic expansions rarely die of old age – they generally are killed by the Fed”;

- At some point, the markets will need to be concerned again about massively increasing deficits and debt, but right now neither party (nor, especially, President Trump) show the slightest interest in addressing this rapidly growing problem;

- Solid US GDP growth, as well as respectable earnings and revenue growth, make for a generally positive market environment, and we maintain our view that US stocks will end the year higher than where they began.

- As we discussed above, however, the markets seemingly have begun to react to decelerating earnings growth, decelerating economic growth, and generally rising interest rates. Through October, we’ve seen these factors, plus uncertainty over trade policy and the mid-term elections, all combine to push valuations down and volatility up;

- Ongoing trade tensions and (perhaps) an overly aggressive Fed seem to be the largest potential threats to the current generally positive economic regime;

- Interestingly enough (perhaps because of lower starting point valuations), non-US markets generally have held up better than US markets (especially Small Caps, which have taken it on the chin) during the market gyrations of October;

- At current interest rates and credit spreads, the public credit markets continue to look very expensive to us, and our return expectations are muted accordingly. We are nearing the end of the current credit cycle and risks are increasing;

- In particular, the leveraged loan market (i.e., floating rate bank loans) has seen a decided deterioration in both the credit quality of borrowers and in the covenant structures of the loans – both distinct warning signals.

- Likewise, the traditional Investment Grade bond market has seen a downturn in the average credit rating of borrowers. This could have dramatic implications if/when the next recession hits and corporate revenues decline;

- Many investors increasingly are turning to shorter-duration bond strategies and even cash solutions, which finally have a positive real yield again due to the Fed rate hikes. The curve is so flat that investors simply are not being sufficiently compensated to take on term or duration risk;

- For investors who can access the private markets and handle some degree of illiquidity, we still believe there are better opportunities in the private markets versus the public markets, though investors face compressed premiums versus historical levels, driven by huge investment flows over the past 18-24 months, and performance will be very manager and strategy specific;

- We expected that rising rates, increased volatility, and greater security price dispersion would create a more positive environment for both traditional active managers and for alternative investments. This generally has been true for most of the long-only and hedge fund managers we recommend, though we remain somewhat disappointed with the overall performance of the liquid alternatives space (i.e., ’40 Act mutual funds that trade in non-traditional strategies);

- With most public markets viewed as at least fully valued (though valuations certainly have fallen over the past month), many investors are revisiting the use of alternative investments within their portfolios, both for diversification purposes and as a means of accessing lower-correlated sources of potential return. We continue to believe that hedge funds generally will deliver superior performance than their liquid alternative brethren, because of less liquidity and leverage constraints;

- While we generally are constructive on the global economy and overall market performance, the public markets are not cheap, and the market volatility we have long expected has materialized (in spades). We still believe that the market can move higher over the rest of the year, though with increased volatility. We also believe, however, that clients need to have their expectations managed as to what a globally diversified portfolio can deliver over a full market cycle.

“We have met the enemy and he is us” is the famous quote from the iconic comic strip character Pogo. Investors need to remember that market volatility is normal, geopolitical uncertainty is normal, and evolving economic cycles are normal. We collectively have enjoyed 8+ years of central-bank induced complacency, but those days are over. As the Brits used to say in WWII, “Stay calm and carry on”. Investors should, of course, be paying attention, but they also need to remain calm, stay disciplined, and keep their investment horizons aligned with their long-term financial goals and objectives.

Warm Regards,

Scott Welch, CIMA®

Chief Investment Officer

Dynasty Financial Partners

Source: Bloomberg, Data Analysis, 1/2017-Present

Source: Zephyr, Data Analysis, 1/2017 – Present

Source: Morningstar, Data Analysis, 1/2017 – Present

Past performance shown is model performance shown is no guarantee of future results. The model portfolio performance does not reflect actual trading or any advisory, management, or transaction fees, all of which could result in substantially lower results. This does not reflect the impact that material economic and market factors have had on decision making. You cannot invest directly in an index.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits