KEY TAKEAWAYS

- The U.S. economy likely grew at a moderate to strong pace in the third quarter.

- Consumer spending continues to be the primary driver of output, while business spending’s contribution may drop off.

- Net exports and inventories may have meaningfully influenced GDP as effects of the U.S.-China trade dispute bled into manufacturing and demand.

Investors’ first look at third-quarter gross domestic product (GDP) will be released on Friday, October 26. Based on the economic data and projections we’ve seen, the economy grew at a moderate to strong pace in the third quarter, with the Bloomberg-surveyed economists’ consensus at 3.4%. The benefits of fiscal stimulus, continued consumer strength, and improved business spending have powered the U.S. economy this year, and we’ll likely see largely the same general story for the third quarters, although business spending may be somewhat less robust. Both trade and extreme weather in parts of the country are expected to have an impact on the number, increasing the likelihood of a surprise, with our bias to the upside. While we may not again achieve the near 5% growth seen in the second and third quarter of 2015, we think the expansion is durable at least into 2019—and possibly beyond—as the growing impact of deficit-financed stimulus and deregulation outpace headwinds from trade, slower global growth, and Federal Reserve (Fed) tightening.

FISCAL STIMULUS FUELS SPENDING

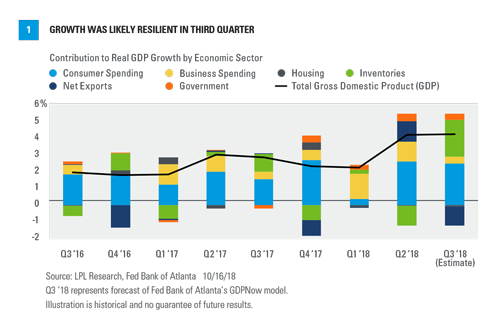

When we prepare for GDP report releases, we like to reference several published GDP projections when gauging what to expect for headline growth and underlying details. These include economist surveys, with the consensus at 3.4% for both Bloomberg’s and the Wall Street Journal’s surveys. We also look at forecast models by several Fed regional banks based on data received so far. Of these, we find the Atlanta Fed’s forecast most useful, since it breaks down GDP growth by traditional economic sectors: consumer spending, business investment, housing, net exports, change in private inventories, and government spending. While we don’t put too much faith in a single forecast, we think the underlying detail helps provide an overview of the data we’ve seen in recent months and a rough guide to how these have impacted economic growth [Figure 1].

Overall, the U.S. economy is on solid footing, and has been for a while. However, fiscal stimulus has kicked the expansion into a new gear, following a midcycle slowdown in late 2015–2016 due to a dramatic collapse in oil prices and an accompanying decline in financial conditions and global growth. Consumer spending, which typically accounts for about 70% of GDP, continues to be the primary driver of output. The Atlanta Fed model estimates that consumer spending grew at over 3% in the third quarter, which would be a slowdown from a very strong second quarter but still well ahead of the expansion average. Personal spending growth continues to be fueled by a strong job market, modestly accelerating wages, rising stock prices, and near cycle highs in consumer confidence.

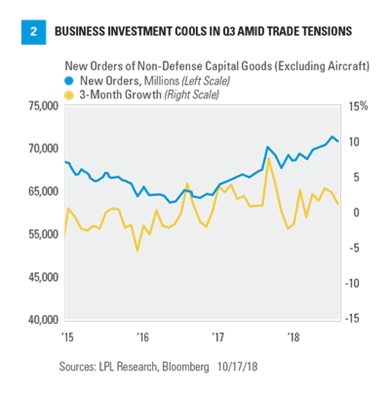

Business investment’s share of GDP growth likely slowed last quarter. Our favorite measure of business spending, new orders of non-defense capital goods (excluding aircraft), has cooled from a dramatic rise over the past few months as growth nears the longer term trend [Figure 2]. However, the level of capital expenditures still sits near the highest point of the economic cycle. While growth remains strong, there may be a chilling effect from trade, with the Fed reporting in its latest Beige Book survey that multiple districts noted that trade uncertainty has prompted some U.S. businesses to scale back or postpone capital investment. While we expect trade to weigh only minimally on overall growth, the increased uncertainty makes it more difficult for U.S. firms to plan.

TRADE IMPACT CREEPS IN

Third-quarter GDP may also be heavily influenced by two highly volatile components: inventories and net exports, both of which also may have been affected by trade. The change in private inventories weighed on GDP in the second quarter, making the strong growth level even more compelling. Rebuilding inventories may make a strong contribution to third quarter GDP, with the Atlanta Fed model attributing 2.2% of the overall 4.1% growth expected to inventories. On the other hand, the model has net exports reversing direction after strong activity ahead of new tariffs in the second quarter.

These changes exemplify trade’s growing impact on output, for better or worse. Wholesale inventories have been climbing at the fastest pace since 2015, indicating companies’ expectations for stronger consumer demand, which is supported by the lowest inventory to sales ratio in nearly four years. However, the most recent uptick is partially due to supply chain disruptions, which could eventually weigh on growth. Unfilled orders for durable goods continue to increase with inventories, hinting at breakdowns in the supply chain as manufacturers and firms digest growing labor shortages and rising input costs. We attribute these disruptions to stress from trade tensions, a tight labor market, and the impact of extreme weather in regions of the country. An increase in exports boosted second-quarter GDP as purchasers rushed to beat the implementation of retaliatory tariffs, but the glut of exports was just borrowing growth from future quarters. U.S. exports have dropped for three straight months for the first time since January 2016, as the amount of levied Chinese goods is now $250 billion and the U.S. dollar hovers near a 15-month high. While we are optimistic that the U.S. and China will eventually reach an accord on trade, we expect these conditions to persist until that agreement.

WHAT ABOUT THE FED?

Despite another quarter of potentially strong growth behind us, we don’t expect the Fed to accelerate the pace of rate hikes, as inflation remains manageable. We believe the solid macroeconomic environment combining solid growth and low inflation reflects the effectiveness of Fed policy, while at the same time effecting a smooth transition from monetary policy to fiscal policy as the driver of the business cycle.

CONCLUSION

If third-quarter GDP comes in near consensus Friday, it will be our sixth consecutive quarter of GDP growth above 2%, a level of stability not seen since 2004, reflecting a positive overall growth environment in the United States. We continue to emphasize that while we may see some impact from trade on the data, the impact of fiscal policy continues to be much larger. We expect more of the same from the third quarter and looking forward—a moderate pace of economic growth accompanied by gradual interest rate increases, potentially resulting in U.S. GDP growth near 3% this year and sustainable at 2.5–3% growth in 2018.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

Any economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing involves risk including loss of principal.

© LPL Financial

Read more commentaries by LPL Financial