Boston - As the old bond market axiom portends, "Don't fight the Fed." The reason why has been underscored for all of 2018.

Bond prices fall as interest rates rise, and this year has proven to be a downright case study. Why? The Federal Reserve has remained on its unwavering course to normalize interest rates from their still-low levels. And its "dot plot" projections for the rest of 2018 as well as 2019 show plenty more Fed hikes to come. Being a discounting mechanism by nature, the markets have begun to take all of this into account.

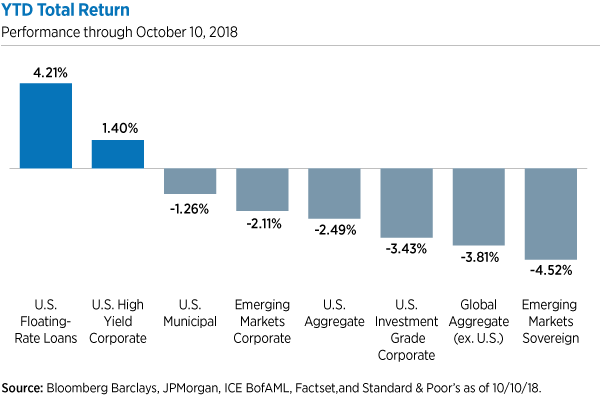

The resulting performance picture hasn't been pretty for fixed-income positions, with deteriorating net asset values subtracting from investor total returns. In fact, most bond market sectors have posted negative results so far this year -- bonds have served only to detract from investors' overall performance experience. Alas, the so-called "balanced portfolio" of 60% stocks (S&P 500) and 40% bonds (U.S. Aggregate) has returned just 2.5% year-to-date, making it a tough year for investors indeed.

Meantime, our asset class -- the market for senior, secured, floating-rate corporate loans -- has proven to be a bright spot in capital markets. The main driver of year-to-date loan market performance has been the combination of high coupon income, limited credit situations and healthy supply/demand equilibrium. The performance picture is worth a thousand words.

Data provided is for informational purposes only. Past performance is no guarantee of future results.

Floating-rate loans: The anti-bond

Note that loan market performance has little to do with changes in interest rates, with the exception of the very front end of the yield curve (i.e., where the Fed operates). That is, loans "float" over variable short-term rates, generally 1-month or 3-month Libor. Because of this, traditional bond duration is broadly absent in loans. As a result, loans do not fall in price when interest rates across the yield curve are on the rise. In fact, loan returns have tended to improve during these periods, thanks in no small part to the way loan coupons track higher with rising short-term interest rates. Year-to-date results are simply our market's latest "Exhibit A."

There's a time-tested strategic case for this asset class to be sure -- it's uniquely different and therefore blends well with other portfolio ingredients -- but right now investors might also think about loans tactically. Loans offer an important escape hatch from bonds today, delivering not only the much-needed higher income, but also the asset class's defining "anti-bond" properties. They say history rarely repeats but often rhymes, and loans' mid-single-digit returns in the tough bond years of 1994, 1999 and 2004-2006 can be particularly instructive today.

There are things to consider, of course, and loans are by no means a panacea. The move from bonds to loans is a swap in risks, from interest-rate risk to credit risk. That said, economic and credit indicators suggest that credit risk is indeed worth undertaking for now, as barometric readings on credit health continue to hover in historically normal ranges. There are indeed things to watch -- and at Eaton Vance we're watching them closely -- such as the latest pickup in mergers-and-acquisitions-related issuance and the slow-but-sure trend toward the covenant-lite model.

Choosing a capable and experienced manager -- in any asset class -- is always important. Eaton Vance is one such manager in the loan space. We've managed loan portfolios since 1989, and we have a large and highly specialized team dedicated exclusively to this space. Moreover, we have high conviction in the risk/return orientation underlying our loan strategies today.

Bottom line: At the midpoint of 2018, loans have proven their mettle yet again. Investors in need of income, diversification and a much-needed hedge against inflation and interest rates might give loans a look.

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. The secondary market for loans is a private, unregulated inter-dealer or inter-bank resale market. Purchases and sales of loans are generally subject to contractual restrictions that must be satisfied before a loan can be bought or sold. These restrictions may impede the Fund's ability to buy or sell loans and may negatively impact the transaction price. It may take longer than seven days for transactions in loans to settle. It is unclear whether U.S. federal securities law protections are available to an investment in a loan. In certain circumstances, loans may not be deemed to be securities, and in the event of fraud or misrepresentation by a borrower, lenders may not have the protection of the anti-fraud provisions of the federal securities laws. There can be no assurance that the liquidation of collateral securing a loan will satisfy the issuer's obligation in the event of non-payment or that collateral can be readily liquidated. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer's ability to make principal and interest payments. Investments rated below investment grade (typically referred to as junk) are generally subject to greater price volatility and illiquidity than higher-rated investments. As interest rates rise, the value of certain income investments is likely to decline. Bank loans are subject to prepayment risk. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. Changes in the value of investments entered for hedging purposes may not match those of the position being hedged. No fund is a complete investment program and you may lose money investing in a fund.

S&P 500: An unmanaged index of large-cap stocks commonly used as a measure of U.S. stock market performance.

U.S. Floating-Rate Loans: S&P / LSTA Leveraged Loan Index, an unmanaged index of the institutional leveraged loan market.

U.S. High Yield Corporate: ICE BofAML US High Yield Index, an unmanaged index of below-investment grade U.S. corporate bonds.

U.S. Municipal Bonds: Bloomberg Barclays Municipal Bond Index, an unmanaged index of Municipal bonds traded in the U.S.

Global Aggregate (ex-U.S.) Bonds: Bloomberg Barclays Global Aggregate Ex -U.S. Index, a broad-based measure of global Investment grade fixed-rate debt investments, excluding USD-denominated debt.

Emerging Markets Corporate Bonds: JPMorgan Corp. EM Bond Index (CEMBI) Broad Diversified, an unmanaged index of USD-denominated emerging market corporate bonds.

U.S. Investment Grade Corporate Bonds: Bloomberg Barclays U.S. Corporate Investment Grade Index, an unmanaged index that measures the performance of investment-grade corporate securities within the Barclays U.S. Aggregate Index.

Emerging Markets Sovereign Bonds: JPMorgan Emerging Markets Bond Index (EMBI) Global Diversified, an unmanaged index of USD-denominated bonds with maturities of more than one year issued by emerging markets governments.

© Eaton Vance

© Eaton Vance

Read more commentaries by Eaton Vance