October Doesn’t Disappoint: Volatility Is Back After a Tranquil Third Quarter

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

According to the 2018 edition of the Stock Trader’s Almanac, October has been a “great” time to buy. Once ranked last in terms of stock performance, the 10th month has delivered relatively average returns since 1950. What makes it so attractive is that it’s followed by November and December, historically among the very best months for stocks. We’re also entering the three most bullish quarters of the four-year presidential cycle, based on 120 years of stock market data.

At the same time, October is sometimes known as the “jinx month” because an inordinate number of huge selloffs have occurred in the month, including those in 1929 and 1987. The worst month of the global financial meltdown was October 2008, when stocks gave up close to 17 percent.

There have been only six trading days in S&P 500 Index history in which stocks sold off by eight or more standard deviations, according to a report this week by Goldman Sachs. This past Wednesday was one of those six days, the fifth largest in history, following trading days in September 1955, October 1989, October 1987 and February 2007. The selloff in 1955, interestingly enough, was prompted by news that President Dwight Eisenhower had suffered a heart attack.

If you’ve read my whitepaper “Managing Expectations,” you should know that eight standard deviations (or more) represents a massive, exceedingly rare variance from the mean. Days like this past Wednesday remind us of the importance of diversification into assets that have little to no correlation with stocks—assets such as municipal bonds and gold.

Gold Helped Investors Stanch the Losses

I was impressed with how well gold did this week. The yellow metal behaved exactly as you would expect it to, edging up slightly on safe haven demand Wednesday as stocks—large and small, domestic and foreign—tumbled.

On Thursday, the spread between gold and equities was even more pronounced, with gold closing almost 3 percent higher and the S&P 500 ending down more than 2 percent, below its 200-day moving average.

Wednesday’s laggards included big-name tech firms such as Apple, Amazon and Netflix. Combined, these three companies lost nearly $120 billion in market value on that day alone.

As I shared with you last month, e-commerce is the second largest equity bubble of the last four decades following housing. E-commerce is also vastly overpresented in indexes, meaning extraordinary amounts of money have flowed into a very small number of stocks by way of passive index funds that track them.

Apple alone is featured in almost 210 indexes. Consequentially, when the iPhone-maker’s stock plummets 4.5 percent or more, as it did on Wednesday, a huge percentage of investors are affected.

Again, this is one of the reasons why I advocate the Golden Rule—a 10 percent weighting in the yellow metal, with 5 percent in bullion and gold jewelry, the other 5 percent in high-quality gold stocks, mutual funds and ETFs.

The Return of Volatility

This week the CBOE Volatiliy Index (VIX), sometimes called the “fear gauge,” had its biggest one-day surge since February. But after such a tranquil third quarter, a substantial move in either direction might have been anticipated. LPL Financial Research reports that this year was the first time since 1963 that the normally volatile third quarter didn’t have a single one-day jump of more than 1 percent, up or down.

“Volatility is back and it may require more active strategies on the part of investors to pursue their long-term goals,” LPL Financial’s chief investment strategist, John Lynch, said.

Higher Rates Reflective of a Strong Economy

In response to the selloff, President Donald Trump put the blame squarely at the feet of the Federal Reserve, saying it’s “ridiculous what they’re doing” and calling monetary policy “too tight.”

The Fed is indeed tightening, and I’ve pointed out before that rate hike cycles in the past have preceded market downturns. But calling policy “too tight” at the moment might be a stretch. After being hiked yet again last month, the federal funds rate stands at 2.25 percent. That’s up considerably from near-zero—which is where it remained during much of Barack Obama’s two terms as president—but it’s still historically low, not yet having reached the long-term average of 4.82 percent.

It must also be said that higher rates are reflective of a strong economy—something Trump has fought hard for. In the second quarter, U.S. gross domestic product (GDP) grew 4.2 percent, its fastest pace since 2014, and the Atlanta Fed is now forecasting the same for the third quarter. Unemployment is currently at a multi-decade low, wage growth hit a nine-year high of 2.9 percent in August and median household income in 2017 climbed to $61,372, the most on record. U.S. consumer confidence, as measured by the Conference Board, reached an 18-year high in September.

The private sector is also seeing healthy expansion. S&P 500 companies are expected to report earnings growth above 20 percent for the third straight quarter, according to FactSet. Stocks rebounded Friday morning after a number of companies reported earnings that surprised to the upside. Delta Air Lines, for example, beat expectations, with net income in the third quarter coming in at $1.31 billion, or $1.91 a share, up from $1.16 billion, or $1.61 a share, in the same three months last year.

Although stocks appear to be stabilizing, I think the two-day selloff this week should be enough to convince investors to make sure they have a 10 percent weighting in gold and gold stocks, with allocations to municipal bonds and ultrashort government bonds.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 4.19 percent. The S&P 500 Stock Index fell 4.10 percent, while the Nasdaq Composite fell 3.74 percent. The Russell 2000 small capitalization index lost 5.23 percent this week.

- The Hang Seng Composite lost 3.88 percent this week; while Taiwan was down 4.48 percent and the KOSPI fell 4.66 percent.

- The 10-year Treasury bond yield fell 7 basis points to 3.16 percent.

Domestic Equity Market

Strengths

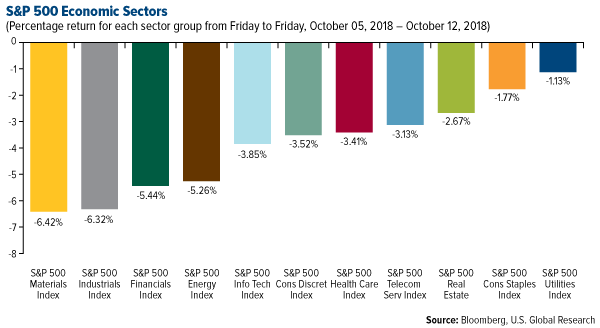

- Utilities was the best relative performing sector of the week, down slightly 1.13 percent versus an overall decrease of 4.03 percent for the S&P 500.

- L Brands Inc. was the best performing stock for the week, increasing 10.26 percent.

- Shares of L Brands Inc., the parent company to Victoria’s Secret, jumped after announcing its intent to pursue “all alternatives for its La Senza business.” La Senza is a Canadian retailer that sells “the world’s sexiest lingerie at seriously hot deals.” On the same day that the Dow Jones Industrial Average fell 545 points, L Brands rose nearly 6 percent as a result of this announcement, demonstrating its commitment focusing on its core business.

Weaknesses

- Materials was the worst performing sector for the week, decreasing by 6.42 percent versus an overall decrease of 4.03 percent for the S&P 500.

- Fluor Corp. of America was the worst performing stock for the week, falling 20.45 percent on weak forecasts for its third-quarter results.

- Suffering its third largest one-day drop in history, the Dow Jones Industrial Average fell 3.15 percent on Wednesday, losing 831 points as traders struggled with concerns about global growth, the trade war and potential additional Federal Reserve interest-rate hikes.

Opportunities

- Volkswagen’s truck unit, Traton, is nearing an initial public offering (IPO) according to Reuters. Citigroup, Deutsche Bank, Goldman Sachs, and JPMorgan are in the running to help the German carmaker with this move.

- Activist investor Bill Ackman disclosed his 15.2 million share stake in Starbucks, worth around $900 million, during a presentation at the Grant’s fall 2018 Conference in New York according to CNBC.

- Tesla outsold Mercedes-Benz in the United States for the first time, selling 69,925 vehicles during the third quarter and topping the 66,542 vehicles sold by the German luxury carmaker.

Threats

- John Hussman, an outspoken stock bear, is warning investors of “immediate and severe consequences” for the market according to Business Insider. Largely blaming the Federal Reserve, Hussman forecasts an looming crash that could wipe out $20 trillion worth of stock market value.

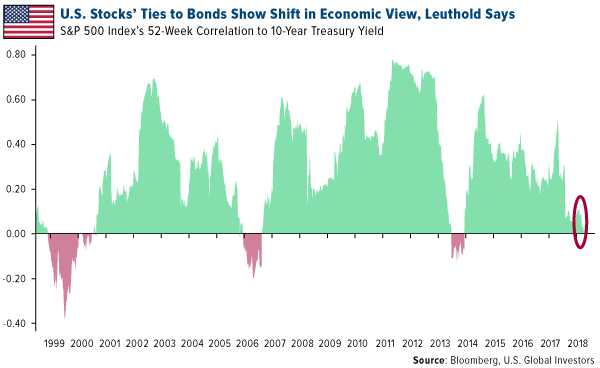

- In recent days, the market has behaved in a manner rarely seen during the past 20 years, and it could mean the meltdown is just getting started. Stocks and bonds have been battered recently and their negative correlation suggests there could be further pressure ahead, according to Jim Paulsen, the chief investment strategist at The Leuthold Group.

- Sears appears to be preparing to file for bankruptcy. The struggling retailer hired M-III Partners to aid in the filing according to the Wall Street Journal.

The Economy and Bond Market

Strengths

- Wholesale inventories in the U.S. rose 1 percent in August as businesses boosted production to keep up with rising sales, which increased by 0.8 percent. An increase in inventories adds to gross domestic product (GDP), suggesting the third quarter will be fairly strong.

- A survey of consumer sentiment in October fell just short of expectations on Friday. However, American confidence in U.S. economic policy is at a 15-year high. The University of Michigan's monthly survey of consumers hit 99 in its preliminary reading for October, just below the 100.4 expected from economists polled by Reuters. The index came in lower than September's reading of 100.1. A key data point in the survey revealed growing bipartisan support for the government's economic policies.

- U.S. producer prices increased 0.2 percent in September, reversing an unexpected decline in August and in line with expectations. A rise in services prices offset a slight drop in prices for goods. In the 12 months through September, the producer price index rose 2.6 percent, slightly less than expected.

Weaknesses

- The number of Americans filing for unemployment benefits unexpectedly rose by 7,000 to a seasonally adjusted 214,000 for the week ended October 6. Economists polled by Reuters had forecast claims slipping to 206,000. The Labor Department said claims for North and South Carolina were affected by Hurricane Florence.

- U.S. consumer prices rose less than expected in September, held back by a slower increase in the cost of rent and falling energy prices, as underlying inflation pressures appeared to cool slightly. The Consumer Price Index (CPI) increased 0.1 percent last month. In the 12 months through September, CPI increased 2.3 percent, slowing from August's 2.7 percent advance. Excluding the volatile food and energy components, CPI edged up 0.1 percent for the second straight month. Economists polled by Reuters had forecast both overall and core CPI to climb 0.2 percent in September.

- The cost of goods imported into the U.S. rose in September for the first time in four months. The import price index climbed 0.5 percent last month, driven up by higher costs of imported fuel. This was above Wall Street expectations of a 0.2 percent increase, according to Econoday.

Opportunities

- Concern that the U.S. economy will overheat and inflation will accelerate is becoming “the prevailing attitude of Wall Street,” according to Jim Paulsen, Leuthold Group Inc.’s chief investment strategist. Paulsen cited the 52-week correlation between the S&P 500 Index and yields on 10-year Treasury notes in a report on Monday. The gauge is poised to turn negative, which means stocks and bonds are starting to move in lockstep for only the fourth time since the late 1990s. Such a move amounts to a “toggle switch,” he wrote, that shows when investors are no longer focused on slower economic growth or a contraction.

- Retail sales numbers out of the U.S. on Monday are likely to point to stronger consumer spending in September. Retail sales are forecast to have grown by 0.5 percent month-on-month in September, accelerating on the prior 0.1 percent rate.

- The New York Fed’s Empire State manufacturing index comes out Monday with the Philadelphia Fed’s manufacturing gauge to follow on Thursday. Industrial output figures are expected to show steady growth of 0.3 percent month-on-month in September.

Threats

- The International Monetary Fund (IMF) downgraded its outlook for the world economy. Citing concerns about trade and emerging markets, the international lender lowered its global growth forecast for this year and next in its World Economic Report. The IMF says the global economy will grow at a 3.7 percent pace this year and next, down 0.2 points from what it predicted in July. It sees the U.S. economy growing at a 2.9 percent rate in 2018. However, they see it slowing to a 2.5 percent rate next year in part due to the one-time impact from President Donald Trump's tax cuts.

- President Donald Trump reiterated threats this week that have further escalated trade tensions with China. When asked if he was ready to impose additional duties on Chinese goods if Beijing retaliated, he told a reporter, "Sure, absolutely." The next round of proposed tariffs would place an import tax on every product the U.S. imports from China.

- Building permits and housing starts due for release next week will be watched carefully amid worries of a slowdown in the housing sector.

Gold Market

This week spot gold closed at $1,217.95 up $15.00 per ounce, or 1.25 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 6.04 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index came in off 1.00 percent. The U.S. Trade-Weighted Dollar Index reversed course this week and fell 0.41 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-10 | PPI Final Demand YoY | 2.7% | 2.6% | 2.8% |

| Oct-11 | CPI YoY | 2.4% | 2.3% | 2.7% |

| Oct-11 | Initial Jobless Claims | 207k | 214k | 207k |

| Oct-12 | Germany CPI YoY | 2.3% | 2.3% | 2.3% |

| Oct-16 | Germany ZEW Survey Current Situation | 74.3 | -- | 76.0 |

| Oct-16 | Germany ZEW Survey Expectations | -12.0 | -- | -10.6 |

| Oct-17 | Eurozone CPI Core YoY | 0.9% | -- | 0.9% |

| Oct-17 | Housing Starts | 1210k | -- | 1282k |

| Oct-18 | Initial Jobless Claims | 210k | -- | 214k |

| Oct-18 | China Retail Sales YoY | 9.0% | -- | 9.0% |

Strengths

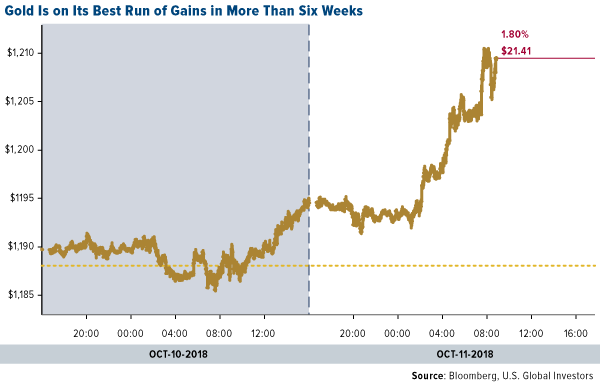

- The best performing metal this week was platinum, up 1.82 percent as hedge funds cut their net bearish position to a five-month low this week. For the eighth consecutive week, gold analysts and traders have reported holding a bullish outlook on the yellow metal in Bloomberg’s weekly survey. This attitude is supported by gold being on its best run in six weeks, as the dollar dropped to its lowest since October 2. Additionally, on Wednesday, exchange-traded funds (ETFs) saw the biggest one-day increase in gold holdings since March 22, totaling 259,116 troy gold ounces according to Bloomberg.

- Recent U.S. inflation data came in slower than expected. In light of this, gold investors took the opportunity to pile into bullion this week according to Bloomberg. “Gold bulls were unstoppable on Thursday as global risk aversion sent investors sprinting to safe-haven assets,” said FXTM research analyst Lukman Otunuga. Thursday marked the third straight day of gains for gold futures, the longest rally in seven weeks, and December gold contracts were over ten times the 100-day moving average.

- India, the world’s second-largest gold market, more than doubled its gold imports for the second consecutive month in September, receiving 93.8 metric tons in 2018, up from 43.6 tons the year prior, according to Bloomberg. These massive inflows are largely due to the country’s strong Love Trade, as Diwali and wedding season are both traditionally golden affairs. British art dealer Sotheby are likewise preparing for celebration as its first ever “The Midas Touch” is scheduled for October 17. The auction will include a 1977 Ferrari 512 Berlinetta Boxer, an armchair from Tuileries Palace and a life-sized, golden sculpture of Kate Moss’ head.

Weaknesses

- The worst performing metal this week was palladium, down 0.38 percent despite hedge funds boosting their bullish position to a four-month high and Evercore ISI saying “There will be blood” in the automobile sector due to falling worldwide auto sales. Despite the Asian equity market seeing the largest selloff since February on Thursday, naysayers were a bit too early in their morning calls saying gold would not benefit as a haven asset. Despite starting the day weak, futures for the yellow metal managed to end Thursday up 1.5 percent, suggesting that analysts’ consistent call for gold not to perform may be getting long in the tooth.

- Used car and truck prices took a tumble in September, experiencing a 3 percent monthly decline, the most in 15 years, according to government data. This dramatic change played a part in denting the core consumer price index, which slowed to 2.3 percent annual gain compared to the 2.4 percent forecast. August’s CPI also had a highly unusual anomaly where apparel prices plunged the most in almost seven decades, dropping the CPI to 2.2 versus the consensus estimate of 2.4.

- South Deep, owned by Gold Fields, continues to frustrate shareholders as the company has yet to curtail losses from the massive South African deposit. While South Deep is the second-largest known body of gold-bearing ore, it continues to miss output targets, with July being its tenth consecutive month of falling production. Chief executive officer Nick Holland expressed his understanding at shareholders’ frustrations, but insisted “we are not far away, we just need more time.” To date, the company has spent over 9 billion rand ($620 million) on the mine, in addition to 22 billion rand spent to purchase the land in 2006.

Opportunities

- Despite negative headlines surrounding slowing global growth, this trend has the potential to benefit gold according to precious metals analyst Jim Steel. “During periods when world trade is very strong, gold tends to be very weak,” said Steel. “When the world trade contracts the gold market takes off, there’s a bit of a lag, but it does really well.”

- After the International Monetary Fund (IMF) cut its global growth forecast on Monday, gold futures rose, supporting the yellow metal’s position as a haven asset. The IMF cited building trade war tensions and stressed emerging markets as reasons for its conclusion that the world economy is plateauing. IG analyst Joshua Mahony notes that “heavy U.S. debt burden” is likely to dissuade traders from viewing the dollar as a safe haven asset, especially if bond yields continue to rise.

- TOMRA’s new COM XRT 2.0 could be a game changer for mining and for TOMRA too. TOMRA is one of the few publicly listed companies that sell these high-tech sorting machines for mining. These machines offer a rapid way to separate waste from ore as the material leaves the crusher circuit. The rejection of waste material from entering the milling circuit offers companies a way to process more materials in a more efficient, compact plant. In addition to its mining capabilities, TOMRA’s sorting machinery has gained attention from the European Commission which intends to use the machinery to sort plastic and aid in environmental clean-up efforts. “We have enormous potential to secure a more sustainable world for future generations,” says Harald Henriksen, head of TOMRA Collection Solutions. The company hopes to hire 2,000 new employees globally over a five-year period as their growth trajectory increases.

Threats

- After the big stock market selloff on Wednesday, one clear trend has emerged, according to Bloomberg. Investors are selling their growth shares and moving to value, which are shares that trade at a discounted price. Charlie McElligot, Nomura Holdings Inc. strategist, said this week that investors are unwinding their momentum positions, much of which are growth shares that post consistent earnings, and are instead going to value. Growth shares are vulnerable to rising bond yields and interest rates because of their long-duration characteristics. Bank of America found that more than two times as many S&P 500 company projections were below Wall Street estimates than above – the most shortfalls in two-and-a-half years, a sign that analysts are too bullish on the market.

- Just as borrowing costs are rising, a new supply of debt is slated to hit the $15.3 trillion Treasury market. The U.S. budget deficit is set to swell to roughly $1 trillion sometime in fiscal year 2019. Plus, interest on that debt is forecast to triple in the next 10 years to nearly a $1 trillion a year, according to the Congressional Budget Office. Demand at a recent Treasury debt action also fell to a decade low, writes Bloomberg’s Liz Cap McCormick and Alexandra Harris. Additionally, U.S. mortgage rates rose the most since the week President Trump was elected, rising to 4.9 percent, up from 4.71 percent the week prior. This is the highest rate since mid-April 2011, according to Freddie Mac. Rising mortgage rates cut into the affordability for buyers, which has led to a slowdown in sales, writes Bloomberg’s Prashant Gopal.

- On Wednesday, the U.S. Department of Justice (DOJ) unsealed charges against a Chinese Ministry of State Security operative for conspiring to commit espionage and steal trade secrets from U.S aviation and aerospace companies. The U.S. went one step further and extradited the Minister to the U.S. from Belgium this week. The DOJ press release said “This case is not an isolated incident. It is part of an overall economic policy of developing China at American expense.”

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 12 was Moeda Loyalty Points, up 287.09 percent.

- French retail giant Carrefour SA is partnering with IBM to adopt blockchain ledger technology to track and trace some fresh produce such as chicken, eggs and tomatoes, as they travel from farm to retail stores, reports Reuters. The IBM Food Trust will allow the company to track and share information on how products are grown, processed and shipped. Blockchain technology could be very useful when it comes to salmonella outbreaks linked to eggs and poultry by quickly identifying the origin of the contaminated food. Carrefour said they expect to widen its use to 300 fresh products around the world by 2022.

- The United Arab Emirates (UAE) announced on Monday that they plan to permit initial coin offerings (ICOs) as a fundraising method for domestic companies, writes CoinDesk. They plan to introduce rules in 2019 that would allow companies to raise capital using cryptocurrencies versus traditional IPOs. Reuters reports that low oil prices and lackluster equities markets in recent years have hurt IPO activity in the country and across the region. More positive news comes out of the UAE as local Dubai media reported this week that city residents will soon be able to pay for their bills, retail purchases and other utilities using the state-backed cryptocurrency emCash. The coin is issued by the Credit Bureau of Dubai and will be partnering with payment provider Pundi X.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended October 12 was Bytecent, down 71.54 percent.

- U.K.-based cryptocurrency exchange Coinfloor will be reorganizing its operations and cutting staff members in response to the sell-off in digital currencies, reports Bloomberg. On Monday, Financial News reported that the exchange will cut a majority of its 40-something employees, citing two people familiar with the situation. “We are currently working on a business restructure to ensure that we focus on our competitive advantages in the marketplace,” said Coinfloor’s CEO Obi Nwosu.

- Although some nations are taking steps to increase ICO activity, Autonomous Research has found that global ICO activity has dropped over 90 percent so far this year, reports Bitcoin.com. The research firm notes that investments were less than $300 million in September, which is a steep drop from $2.4 billion in January.

Opportunities

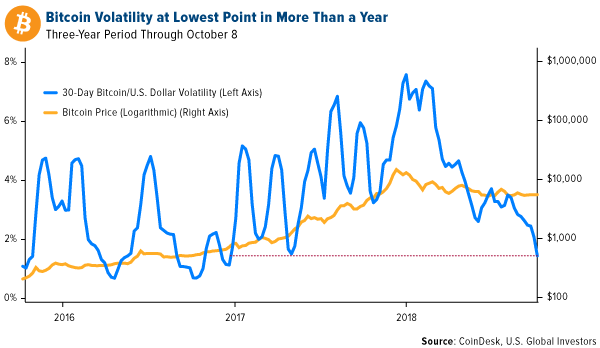

- As bitcoin’s volatility falls to its lowest in more than a year, many are speculating that it could be an inflection point demonstrating the coin’s maturity. Bloomberg Intelligence commodity strategist Mike McGlone said that the cryptocurrency market “is a maturing market, so volatility should continue to decline.” Gil Luria, director of research at DA Davidson &Co., says that stabilization in bitcoin’s price has led to a decline in speculative investments. Luria said that “volatility and volumes are two sides of the same coin” and that “as speculator involvement is diminished, volumes go down and volatility goes down as well.” Although bitcoin fell 6 percent on Wednesday, along with most other cryptocurrencies, its volatility had been muted up until then with a trading range of $300 for several weeks.

- According to a report from Crypto Fund Research, 90 hedge funds focusing on cryptocurrencies launched in the first three quarters of this year, with 30 more expected to launch before year end. Around 600 hedge funds of all types are set to launch in 2018 and the expected 120 cryptocurrency funds would comprise 20 percent of those, a small increase from 16 percent of all new hedge funds the prior year, writes CoinDesk. Although many cryptocurrencies have fallen into bear markets, Joshua Gnaizda, founder of Crypto Fund Research, says that “these seemingly unfavorable market conditions have not deterred managers from launching new crypto hedge funds at a record pace.”

- The People’s Bank of China is hiring more blockchain technology and legal experts as it continues to develop its own central bank digital currency, reports CoinDesk. Job descriptions posted on Tuesday show that engineers will be tasked with developing a fiat-linked digital currency software, a cryptography and security model and a chip processor for making end-point digital currency transactions. The search for new talent signals that China is ramping up its efforts to launch a yuan-based digital currency with the core features of cryptocurrencies.

Threats

- While some have positive forecasts for the market, Juniper Research is warning that many metrics in the cryptocurrency world are pointing to a market implosion, writes Bloomberg. Juniper estimates a further 47 percent quarter-on-quarter drop in transaction values in the third quarter, as transaction values fell by 75 percent in the second quarter of this year. They also note that daily transaction volumes for bitcoin were around 360,000 a day in late 2017 and are just 230,000 in September 2018. The firm writes that “given our concerns around both the innate valuation of bitcoin, and of the operating practices of many exchanges, we feel that the industry is on the brink of an implosion.”

- On Wednesday the U.S. stock market saw its biggest drop since February, with bitcoin falling 6 percent along with it and XRP and ethereum also falling 10 percent. Cryptocurrencies lost $13 billion in value in a matter of hours, according to CoinMarketCap. While some proponents have called bitcoin the “digital gold,” a safe haven asset uncorrelated to the larger market, this week’s sharp decline proves otherwise, writes CNBC.

- South Korean officials reaffirmed the country’s ban on ICOs during the annual government audit in a parliamentary meeting on Thursday, reports CCN. Financial Services Commission Chairman Choi Jong-ku said during the meeting that “although many people call for the government to allow initial coin offerings, there are still uncertainties related to such a move as well as the possibility of serious fallouts.” South Korea issued a ban on all ICOs in September 2017, however the legislature moved forward with a proposal to lift the ban in May this year.

Energy and Natural Resources Market

Strengths

- Nickel was the best performing major commodity this week, remaining essentially flat. The commodity rallied after LME Stocks continue to draw down over 2018 with the decline accelerating over the last six months, particularly as demand has increased.

- The best performing sector this week was the NYSE Arca Gold Miners Index. The index rose 0.07 percent as the global equity sell-off spurred a second consecutive weekly advance for gold prices.

- The best relative performing stock for the week was Fresnillo PLC. The Mexican producer of precious metals was down only slightly 0.16 percent as struggling miners continued to outperform as investors bet the sector will benefit from a renewed appetite for gold.

Weaknesses

- Gasoline was the worst performing commodity this week. The commodity dropped 0.48 percent after market analysts revealed there are abundant supplies of refined products globally, with the U.S. having the highest level of inventories for this time of year since 1990.

- The worst performing sector this week was the S&P 1500 Container & Packaging Index. The index was up slightly 0.24 percent after BMO analyst Mark Wilde downgraded the sector, citing a looming capacity surge that could "easily" be the biggest in two decades.

- The worst relative performing stock for the week was Packaging Corp of America. The manufacturer of containerboard products was up marginally 0.26 percent. This is despite BMO stating it is the best-run containerboard player in their coverage with a strong balance sheet, while warning that it remains unclear over how the incremental capacity will be absorbed, with demand growth already slowing.

Opportunities

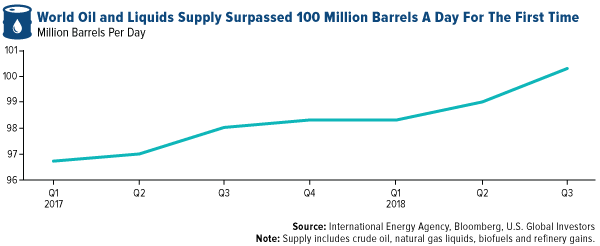

- The world is pumping out more oil and other petroleum liquids than ever before. Global supply rose to 100.3 million barrels a day in the third quarter, the International Energy Agency said Friday. The new quarterly output record underscores how growing demand in the developing world requires new sources of supply.

- China's trade surplus with the United States widened to a record $34.1 billion in September as exports to the American market rose by 13 percent over a year earlier despite a worsening tariff war. Chinese exports to the United States have at least temporarily defied forecasts they would weaken after being hit by punitive tariffs.

- Gold could climb to over $1,300 an ounce, says Bank of America. According to the bank, gold is set to climb over the next year due to the constant cloud of uncertainty with regards to the U.S budget deficit alongside concerns over trade wars. “In the short run, the effects of a strong dollar, higher rates dominate. But in the long run, a huge U.S. government budget deficit is pretty positive for gold,” said Francisco Blanch.

Threats

- China optimists see risk to their thesis of a strong economy in spite of the trade war. According to Cornerstone Macro analysts, Beijing has opened the door to the currency breaking below the critical level of 7 yuan to the U.S. dollar. Further devaluation would require tighter capital controls, and even greater fiscal stimulus to stabilize the economy. As a result, the analysts suggest there are now tangible risks to their optimistic China view.

- Crude oil rose to four-year highs, unless you’re a Canadian producer. Welcome to Canada, where crude prices haven't recovered, says Bloomberg. Western Canada Select slumped below USD$20 a barrel on Thursday, the lowest in more than two years, continuing a brutal streak of declines for the country's main grade of crude. The drop has come as rising production from Canada's oilsands overwhelms the nation's pipeline capacity and as new planned pipelines encounter environmental and political opposition.

- OPEC cut global oil demand growth forecasts. Weaker economic growth across developed and emerging markets will lower demand for crude and derivative products for 2018 and 2019, said the organization. In addition, OPEC increased its expectations for crude supply growth for the same period, suggesting the global crude market is adequately supplied.

China Region

Strengths

- Indonesia’s Jakarta Composite Index rose 43 basis points for the week, while India’s NIFTY and SENSEX indices climbed 1.51 and 1.04 percent, respectively.

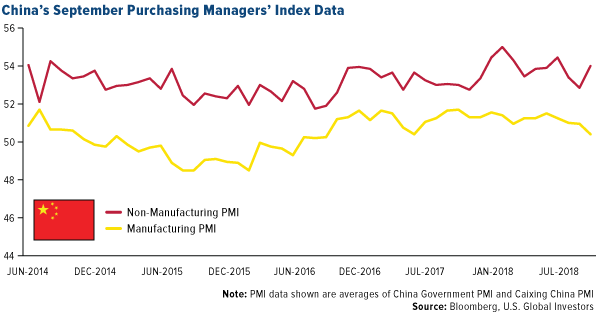

- The Caixin China services PMI clocked in better than anticipated (echoing the beat in the official non-manufacturing PMI) at 53.1, ahead of analysts’ expected 51.4 showing and up solidly from August’s 51.5 print. Thus while the manufacturing PMIs have surprised to the downside, note that non-manufacturing/services readings have beaten to the upside.

- Telecommunications was the top performing sector amid a generally risk-off and red week, climbing 42 basis points—the only sector in the Hang Seng Composite to finish in the green over the last five trading days.

Weaknesses

- China’s Shanghai Composite tumbled 7.6 percent following its reopening after Golden Week holidays during the first week of October.

- China’s monthly reading on foreign exchange reserves for September missed expectations, coming in at $3.087 trillion, down from $3.109 and below expectations for a $3.105.

- Information technology was the worst performing sector in the Hang Seng Composite Index for the week, falling 6.78 percent.

Opportunities

- Despite pressure from President Donald Trump, the U.S. Treasury Department’s staff has stated that China is not manipulating the yuan, reports Bloomberg. The International Monetary Fund (IMF) appears to agree with this conclusion, stating that the depreciation witnessed earlier this year “has a lot to do with the strength of the dollar.” Should Mnuchin accept these findings, it could potentially avert further trade war escalation or help ease tensions.

- President Xi Jinping is set to meet with President Trump at the end of November during the G20 summit in Buenos Aries, according to White House economic advisor Larry Kudlow. This meeting could potentially start a thaw in the China-U.S. tensions.

- Mike Pompeo, U.S. Secretary of State, reported making “significant progress” with Kim Jong Un on the creation of a denuclearization plan for North Korea. “Kim Jong Un appreciated the positively developing situation on the Korean peninsula,” reported the Korean Central News Agency (KCNA), which stated the Asian leader “expressed satisfaction over the productive and wonderful talks.”

Threats

- Trade war concerns remain central as the U.S.-China spat deepens. This week it was revealed that China hit a record trade surplus with the U.S. of $34.13 billion in September. Reuters calculations show that China’s trade surplus with the U.S. for January to September was $225.79 billion, up from $196.01 billion in the same period last year. Chinese Commerce Minister Zhong Shan said this week that the U.S. shouldn’t believe that ever rising tariffs can induce China to back down. Zhong said “The U.S. should not underestimate China’s resolve and will.”

- Pressure continues on the Chinese yuan as the economy shows more possible signs of slowing. The currency fell as much as 0.53 percent on Thursday after the central bank weakened fixing for a ninth session, setting the daily reference rate weaker than expected, reports Bloomberg. The yuan has fallen more than 9 percent against the U.S. dollar over the past six months, including a drop of 0.6 percent last month, which makes it one of the world’s worst performing currencies.

- Chinese home buyers were angry and demonstrated at two real estate offices last week demanding they get their money back after learning that apartments were selling for far less than what they paid for them. Prices were as much as 30 percent lower in one city in Jiangxi province. China’s Golden Week, which fell last week, is normally a strong period for new home sales as holiday makers spend big. However, transactions this year were their lowest since at least 2014, according to China Securities Co. Bloomberg writes that this unrest is a further sign that China’s property market is beginning to cool.

Emerging Europe

Strengths

- Turkey was the best relative performing country this week, gaining 1.87 percent. Optimism over the hearing for the imprisoned American pastor and the court’s decision to let him free had a positive effect on equities trading on the Istanbul exchange.

- The Turkish lira was the best performing currency this week, gaining 3.5 percent against the U.S. dollar. The currency appreciated the most among emerging markets on the expectation that imprisoned American pastor Andrew Brunson would be released at Friday’s hearing. He has been held for almost two years for his role in the failed 2016 coup, according to the Turkish administration.

- Real estate was the best performing sector among eastern European markets this week.

Weaknesses

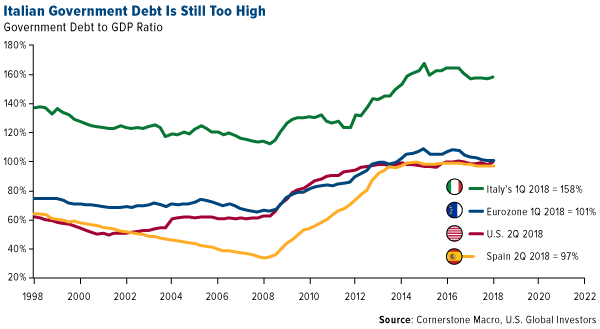

- Greece was the worst performing country this week, losing 4.65 percent. Worries over growing Italian debt and trade tensions had the most negative effect on stocks trading on the Athens exchange. Greek banks were the biggest laggards.

- The Czech koruna was the worst relative performing currency this week, gaining 12 basis points against the U.S. dollar. The central bank’s rate hikes support the koruna and the Czech Republic has increased rates six times since August 2017.

- Information technology was the worst performing sector among eastern European markets this week.

Opportunities

- While the IMF cut its global growth forecast for the first time in more than two years on trade concerns, it actually raised Poland’s economic expansion forecast to 4.4 percent this year, up from the prior forecast of 4.1 percent. The IMF predicts the Greek economy will grow at a rate of 2.4 percent this year versus the prior forecast of 1.8 percent growth. The IMF also revised upwards its expectations for the 2018 primary surplus to 3.5 percent of GDP. The debt level is expected to settle at 151.1 percent of GDP in 2023.

- Danske Bank lost almost 40 percent of its value year-to-date, after the bank was accused of laundering Russian money through its small unit in Estonia. The Danish bank has admitted that about $235 billion should be treated as suspicious transactions. The bank’s shares could rebound after the large sell off, however investors should be aware that there are uncertainties regarding the size of potential fines.

- Turkey’s finance minister proposed a plan to cut the country’s inflation, which reached above 24 percent in September compared to a year ago. According to the announcement, banks will start cutting rates by 10 percent on some outstanding loans and some businesses will cut prices by 10 percent until the year-end. There will be no price hikes in electricity and natural gas until the end of the year as well.

Threats

- Italy has become the center of news in recent days after the nation’s new administration proposed a budget deficit of 2.4 percent of GDP in 2019, much higher than expected. Italy’s government debt to GDP ratio is almost at 160 percent, much higher than the 101 percent eurozone average. Reuters cited senior lawmaker Alberto Bagnai of the League party, who said a downgrade of Italian debt by credit rating agencies is possible, as market concern over the financial sustainability of the government budget targets mounted.

- Eurozone investor confidence weakened in October, largely due to uncertainties surrounding fiscal policy in Italy and the automobile industry in Germany. The investor sentiment index fell by more than expected to 11.4 in October, down from 12.0 in September.

- Minutes released this week revealed that the European Central Bank is increasingly concerned about the deceleration of GDP growth. However, the slowdown has not been pronounced enough to alter monetary policy for the euro area. Wage growth accelerated, but did not produce higher inflation.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All