Chart of the week

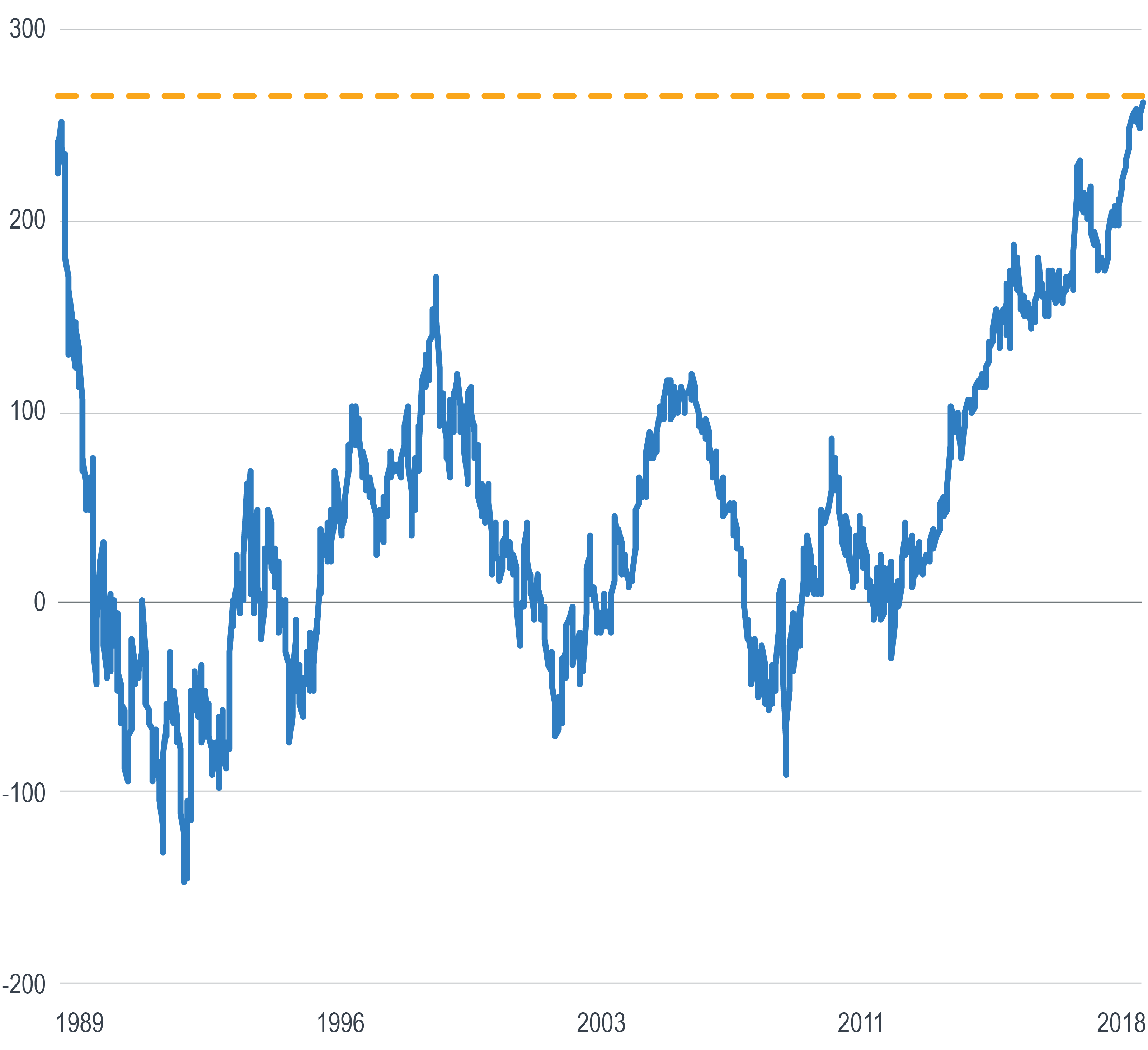

US/German 10-Yr Yield Spread (bps)

This chart shows that the yield on the 10-year U.S. Treasury bond (which hit its 2018 high this week) now exceeds the yield of the 10-year German government bond by 264 basis points, its widest margin in almost 30 years.

There are of course several reasons why two bonds with the same maturity should have different yields.

Credit risk: One explanation could be a growing difference in credit risk. Data from the International Monetary Fund (IMF) show that from 2012 to 2017, Germany’s debt to GDP ratio fell from 79.8% to 64.1%. In the U.S. over the same period, the ratio increased from 103.5% to 107.8%.

Even though higher leverage generally coincides with higher borrowing costs, this explanation seems unlikely, as the risk of the U.S. defaulting on its debt remains extremely low.

Inflation: The most recent readings of inflation are 2.3% in Germany and 2.7% in the U.S. More importantly, 10-year breakeven inflation rates (inflation expectations) are 1.3% and 2.1%, respectively.

All else equal, higher expectations of inflation generally demand to be compensated with higher bond yields. Inflation expectations have risen in both countries in 2018, but have risen faster in the U.S. This is likely a contributing factor in the widening yield spread.

Monetary Policy: The Federal Reserve is now nearly three years, eight rate hikes and $200 billion into its normalization of U.S. monetary policy. The European Central Bank, on the other hand, continues to hold its policy rate at 0% and is still conducting quantitative easing via asset purchases to keep yields low.

Growth: Germany’s economy grew more than the U.S. economy in 2017, but the IMF predicts that over the next five years the U.S. will grow faster on both a real (net of inflation) and nominal basis.

With longer-term yields generally considered reflective of growth expectations, perhaps the strongest signal from this widening yield spread is a confirmation of the IMF’s view that the U.S. is likely to grow faster than Germany (and perhaps by extension much of the rest of Europe) in the years to come.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.