Key points:

- The financial sector has gained over 7% from June lows. It has swung back to life after lagging the broad market at times this year and is now up 2.1% year-to-date.1

- The macroeconomic backdrop is supportive of corporate earnings, major banks are delivering their highest returns on equity in a decade, and deregulation should benefit regional banks.

- Risks include further yield curve flattening and any repercussions of rising protectionism.

- Attractive valuations and exchange traded product outflows suggest that the sector may be overlooked.

Overview

This year we have favored financial stocks on the basis of earnings momentum, deregulation, a steepening yield curve and the value factor. So far, two out of four have aligned with expectations: The sector has posted over 20% year-on-year earnings growth and regulations were cut. Yet the yield curve flattened, and value didn’t outperform.2 Within the sector, financial services firms are outperforming by 1.4%, followed by regional banks at 1.2% above the broad sector. Broker-dealers and exchanges are only slightly ahead at 0.4%, while insurers are languishing and underperforming by over 4% (see Chart 1).

Chart 1: Financial subsectors versus sector performance (1/1/18-8/31/18)

Index performance is for illustrative purposes only. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results. Sources: BlackRock, Bloomberg, August 31 2018. Performance depicted is that of the Dow Jones U.S. Financial Services Index, Dow Jones U.S. Select Regional Banks Index, Dow Jones U.S. Select Investment Services Index, Dow Jones U.S. Select Insurance Index, relative to the Dow Jones U.S. Financials Index, year to date.

A positive backdrop

We consider that three key drivers currently provide support for the financial sector:

1. A bustling macro environment

The U.S. economy is enjoying above-trend growth, stoking solid business and consumer spending. The Federal Reserve’s steady policy normalization has only slightly tightened financial conditions in the domestic economy and interest rates remain supportive of risk appetite. Banks have also benefited directly from the government’s fiscal policies: The 2017 tax cut alone gave them a $6.4 billion windfall in second quarter 2018 earnings.3

2. A healthier banking industry

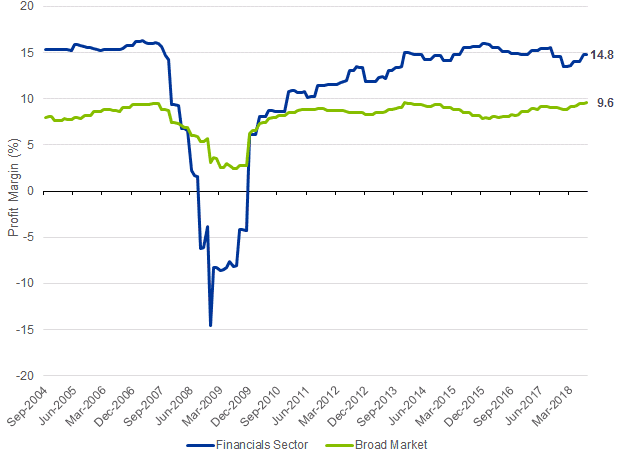

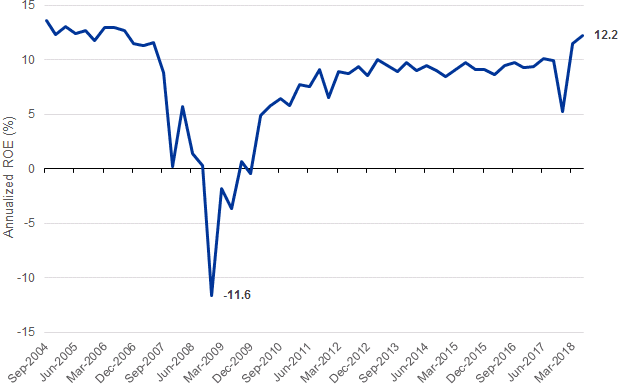

Banks operating in the U.S. — representing one third of the broad financial sector4 — have become much more robust in the decade since the 2007-2008 global financial crisis, responding to regulatory changes. The largest 35 — representing 80% of the assets — have added about $800 billion in tier 1 capital since 20095 and the Fed in June adjudged that all would be able to continue lending in the event of a severe global recession. Banks are also increasingly profitable: Profit margins are in excess of the broad market after diving into negative territory in 2008 (see Chart 2), while returns on equity are at their highest levels since 2009 (see Chart 3). They are returning capital liberally to shareholders in the form of dividends and buybacks — declaring 33% more dividends than a year before, coming after a record $121 billion in 2017.6

Chart 2: Financials versus broad market profit margins (2004-2018)

Index performance is for illustrative purposes only. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results. Source: Bloomberg, August 28 2018. Earnings depicted are for the MSCI USA Financials Index and the MSCI USA Index, over the past 5 years.

Chart 3: FDIC-insured institutions annualized quarterly return on equity (2004-2018)

Source: Federal Deposit Insurance Corporation, Quarterly Banking Profile, June 30 2018.

3. The deregulation agenda

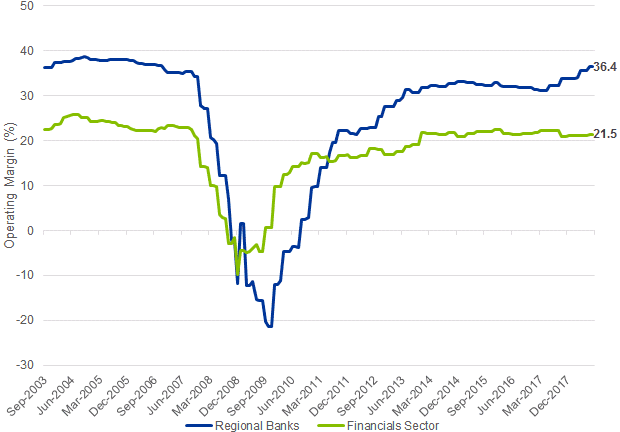

Lawmakers have scaled back requirements of the Dodd-Frank Act that were seen as overly burdensome on small and mid-sized banks. The threshold for needing stress tests to determine capital and liquidity requirements was lifted to $250 billion from $50 billion. This increases the potential for regional banks to return capital (potentially lifting dividend payout ratios) or to accelerate M&A activity. The latter was made easier after the Fed raised the combined assets threshold requiring regulatory review of proposed deals to $100 billion from $25 billion last year.7 Initial signs are positive: Regional banks reported year-over-year earnings growth of 29.5% in Q2 compared to 21% for financials. They have also improved efficiency after the crisis, with operating margins exceeding those of the broad sector from mid-2011 onwards (see Chart 4).

Chart 4: Regional banks versus financial sector operating margins (2003-2018)

Source: Bloomberg, August 29 2018. Operating margins are for the S&P 500 GICS Level 4 Regional Banks Index and MSCI USA Financials Index over the past 15 years.

The swing factor: yield curve dynamics

On the "risks" side of the ledger, U.S.-led protectionism and ensuing trade disputes have the potential to upset the macro backdrop by dampening business confidence and affecting lending growth. Yet arguably the more interesting dynamic is the shape of the yield curve.

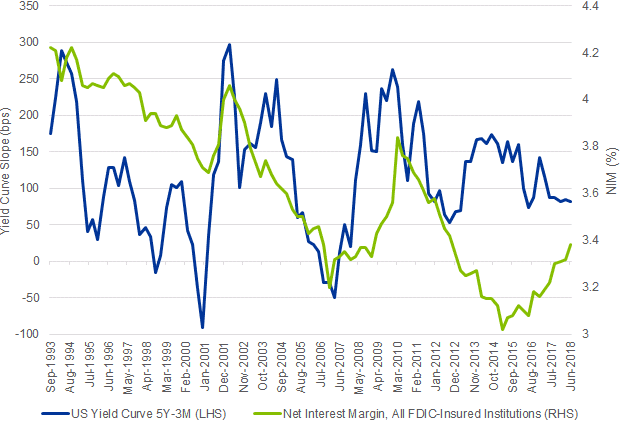

The “yield curve” plots the yields to maturity of bonds of the same credit quality across different maturities. Bonds that mature later typically yield more than shorter duration bonds. The slope of the U.S. Treasury yield curve is often used to understand the cost of borrowing/lending, investor risk sentiment and changes in economic conditions. A common measure of the slope of the curve is the difference in yield between two- and 10-year Treasuries, which has flattened by about 60 basis points (bps, or 0.6 percentage points) over the past year. The curve has broken below 20 bps for the first time since 2007 as market pricing has come around to the Fed’s plans to push short-term interest rates higher.

The shape of the yield curve has significant implications for the financial sector. A flatter curve is usually seen as a signal that bank net interest margins (NIMs) might contract because banks typically fund themselves with shorter duration instruments and lend at longer durations. Yet stepping back, a longer-term view suggests a different relationship (see Chart 5). The sensitivity of NIMs depend on how quickly bank assets reprice relative to their liabilities in response to yield curve shifts, on top of factors such as regulatory capital requirements and how borrowers respond to rapid interest rate changes. While there have been periods of curve flattening and contracting NIMs the 2000s, in the past five years NIMs have increased despite the curve flattening, in this case the three-month/five-year curve.8 Indeed, over 70% of banks reported NIM increases in the 12 months to June 30, 2018. The aggregate industry NIM rose 16 bps from a year earlier to 3.38% thanks to yields on assets rising more quickly than average funding costs.9

Chart 5: Bank net interest margins versus Treasury 5y-3m yield curve

Source: Bloomberg, FDIC, as of June 30 2018.

Investor positioning

Both valuations and flows suggest that financial equities are underappreciated:

- The sector is trading at the second deepest discount to the market (after telecom) at 12.7 times forward earnings compared with the S&P 500’s 16.7 times. This aligns with a style factor based view of the sector: financials stocks make up the largest component of the Russell 1000 Value index, accounting for almost a quarter of the index.10

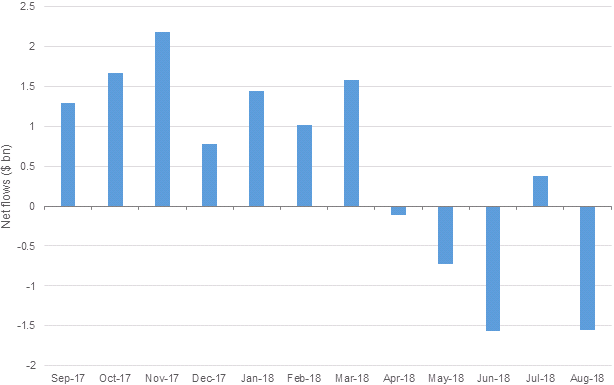

- After seven consecutive months of significant inflows, U.S.-listed financial sector ETF flows turned negative in the second quarter. Outflows totalled over $1 billion in June and August, shrinking year-to-date inflows down to $950 million.

Chart 6: U.S.-listed financial sector ETF flows

Source: Flow data sourced from Markit and calculated by BlackRock, August 31, 2018. ETP groupings and categories are determined by BlackRock.

The bottom line

The financial sector is supported by strong macroeconomic drivers, a resilient banking industry and targeted deregulation. Investors taking a more tactical approach may consider regional banks, which appear particularly well placed to benefit from deregulation. Investors taking a more tactical approach may consider regional banks, which appear particularly well placed to benefit from deregulation. Risks include the uncertain impact of the flattening of the U.S. Treasury yield curve and the uncertainty stemming from trade disputes on the global macro picture.

© iShares

Read more commentaries by iShares