Weighing the Week Ahead: Do Rising Interest Rates Signal the Beginning of the End?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThere is a light economic calendar with a focus on inflation data. This is timely given the growing fear about rising interest rates. While these reports have been benign in recent years, even a modest uptick could fuel concerns. If the focus remains non-political, pundits will be asking:

Do rising interest rates signal the beginning of the end for stocks – and the economy?

Last Week Recap

In my last edition of WTWA I anticipated that the punditry would pay little attention to a week chockful of important economic data. That was accurate until Fed Chair Powell’s answers to some questions seemed to indicate a change in Fed policy. I analyzed four key market questions; that should be helpful even though my guess for the week missed the mark.

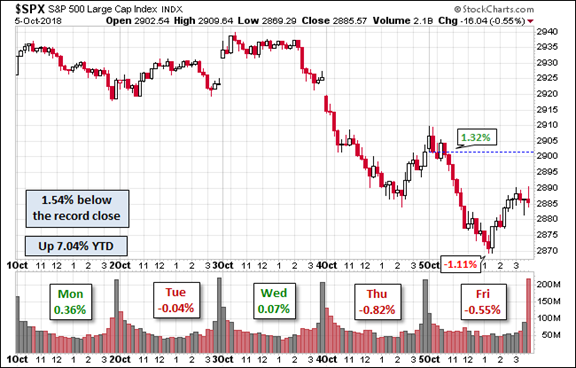

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the version updated each week by Jill Mislinski. She includes a lot of valuable information in a single visual. The full post has even more charts and analysis, including commentary on volume. Check it out.

The market declined 1% on the week. The weekly trading range was about 2.6%, much larger than we have recently seen. From a historical perspective, volatility is still low. I summarize actual and implied volatility each week in our Indicator Snapshot section below.

Really?

Suze Orman opines that you need about $5 million to retire early.

Noteworthy

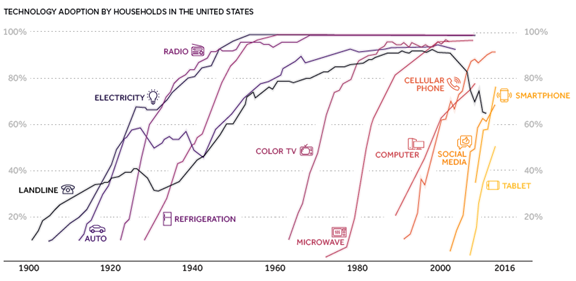

Jeff Desjardins of Visual Capitalist observes that “the world is changing faster than ever before.” This excellent analysis shows eight forces behind global growth, with important details about each trend. (Did you know that there were 100 cities in China with a population over 1 million? One of the charts compares the GDP of Chinese cities with equivalent countries. Fascinating!] Everyone will find something interesting in this article, so sit back and enjoy it. Here are two examples.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

When relevant, I include expectations (E) and the prior reading (P).

The Good

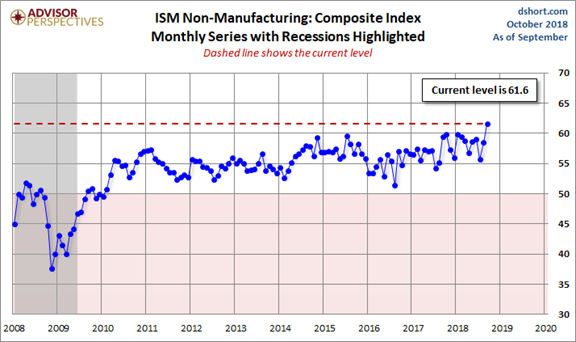

- ISM Non-Manufacturing recorded 61.6 beating expectations of 58.2, P 58.5. (Jill Mislinski).

- Factory orders for August increased 2.3% E 1.8% P -0.5%.

- Strong rail growth continues. Steven Hansen (GEI) provides his customary analysis, examining the data from several viewpoints. The rolling averages all show increases of about 3%, although the rate is decelerating.

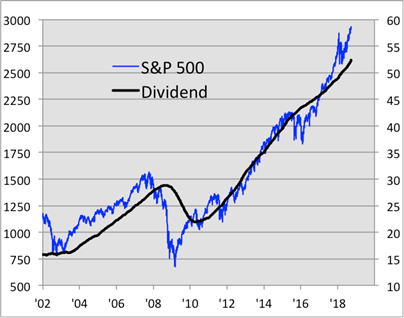

- Dividends are growing. Eddy Elfenbein notes that the 3rd quarter rate of growth was 10.96, the strongest in more than three years. His chart shows the significance.

- Earnings for Q3 are likely to show 20% growth for the third straight quarter. (FactSet).

-

Employment reports showed continuing strength

-

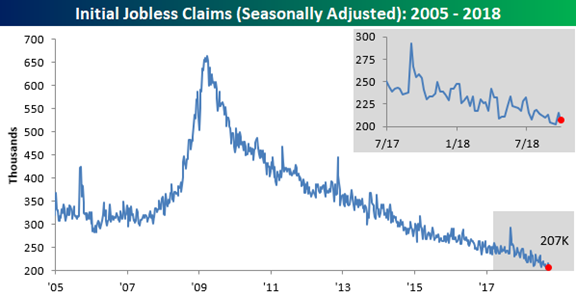

Initial jobless claims declined to 207K E 210K P 215K. (Bespoke)

-

Initial jobless claims declined to 207K E 210K P 215K. (Bespoke)

- ADP private employment showed a gain of 230K E 184K P 168K

- Unemployment declined to 3.7%

- Nonfarm Payrolls increased only 121K with difficult-to-measure effects from Florence and major revisions to the prior two months. (Most people do not understand that the BLS estimates the total number of jobs and then compares it to the prior month total. When there is a big revision to the prior month, the change is determined from a higher base). As usual, the WSJ has excellent report coverage via charts. Here are some examples.

The Bad

As has been the recent case, some of the “bad” news consists of indicators slightly off the best levels.

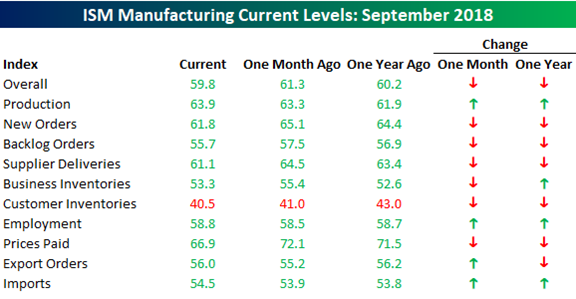

- ISM Manufacturing recorded 59.8 E 60.4 P61.3. Bespoke has excellent coverage of the report, highlighting the comments about tariffs from survey respondents. Here is the analysis of the index components.

- Construction spending for August increased only 0.1%. E 0.4% P 0.2%.

- Fed Chairman Powell’s message about rates being “far from neutral” generated a negative market reaction. Fed authority and leading economist Tim Duy provides great coverage of this story. He writes as follows:

Meanwhile, Federal Reserve Chairman Jerome Powell did a Q&A today. I was not surprised that he maintained the continued “gradual rate hike” mantra. I was surprised when he said “we’re a long way from neutral, probably.” That seemed like it was a bit of a slip. And a hawkish one at that. What seems remarkable to me is that I keep hearing a dovish interpretation of the Fed’s recent disavowal of r-star and the related demise of forward guidance. But what Powell let slip is that he clearly still has an estimate of neutral and we are nowhere near it. That’s hawkish.

Prof. Duy concludes: Bottom Line: You know the bottom line. The US economy is on a roll, and that will induce the Fed to keep adding pressure – gradually – to the brakes.

- The interest rate effect was great enough to move New Deal Democrat’s long-leading indicators to “neutral.” Short and coincident indicators remain positive. I always review this extremely helpful compilation of high frequency indicators. Check it out.

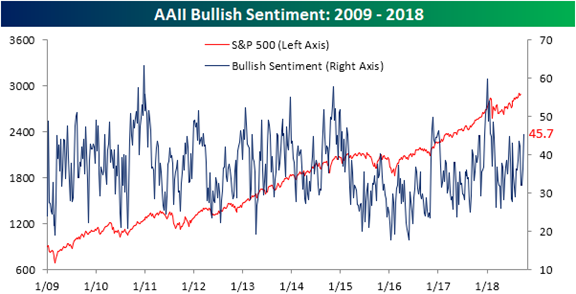

- Bullish sentiment, usually interpreted as a contrarian indicator, has moved significantly higher among individual investors. (Bespoke).

The Ugly

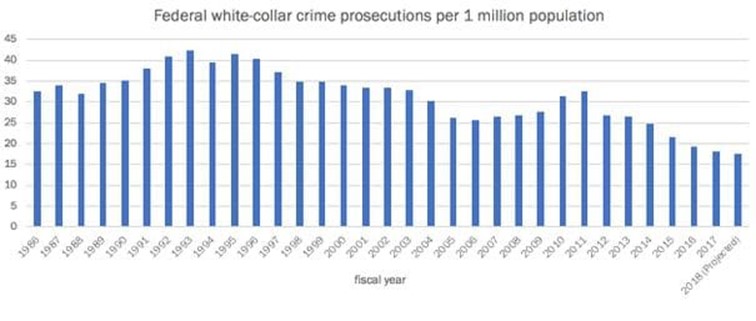

Investors are indignant about the lack of accountability for financial executives who contributed to the financial crisis. It is part of a trend toward dramatically reduced prosecutions of white-collar and public corruption crimes. (Catherine Rampell, Washington Post).

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

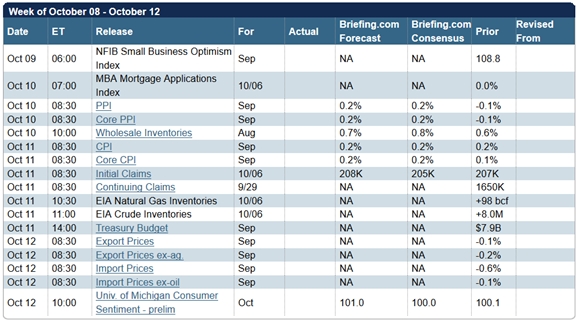

After last week’s bevy of big reports, this week’s calendar is pretty light. Inflation data will take center stage. The NFIB small business optimism index is also garnering a lot of attention.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

As often happens, I expect last week’s news to linger into the week ahead. The interest rate increase and emphasis on Fed policy changes could be underscored by the PPI and CPI reports. There are plenty of scary predictions about interest rates and stocks. I expect pundits to be asking:

Do rising interest rates signal the beginning of the end for stocks – and the economy?

The story is already being played from several viewpoints. As usual, I will show a representative range, beginning with the bears. I provide sources to help you reach your own conclusions.

The Basic Bearish Case

Seeking Alpha provides links to some commentary on the interest rate question. Featured among these is the leading “scare bear” piece by Gary Gordon. It is a good summary of every bearish viewpoint from the Fed to debt to stock buybacks.

Competing for the bearish leadership is Albert Edwards, who gets favorable coverage in MoneyWeek, the best-selling financial magazine in the UK. (but see the Alan Steel analysis in my “Final Thoughts.”)

Only stimulus and stock buybacks are keeping the market afloat. Financial Sense suggests that there are “rolling bubbles.”

Some Bullish Refutation

Bill Kort analyzes CNBC commentary from the reliably bearish Peter Boockvar, noting that the CNBC headline is even scarier than the commentary. There was an “unscientific” poll at the end of the CNBC post asking if you thought there would be a recession next year. 61% said “yes.” I’m not sure if this reflects the persuasive power of Boockvar or the need for confirmation bias for the readers!

Wade Sloame recaps important economic indicators and wonders why there is so much angst among investors. Can it be that things have been so good for so long that many feel we are “due” for bad news. The problem? Such news does not arrive on a schedule, nor does the end of a market cycle.

Avi Gilburt uses data [Jeff – “Insist on data. Don’t invest without it!”] to debunk the fears about quantitative tightening.

Psychological Considerations

Brian Gilmartin makes a great point. Most Americans under 40 have never seen a bond bear market. His speculation is that small declines in bond funds after a great run will not attract much attention.

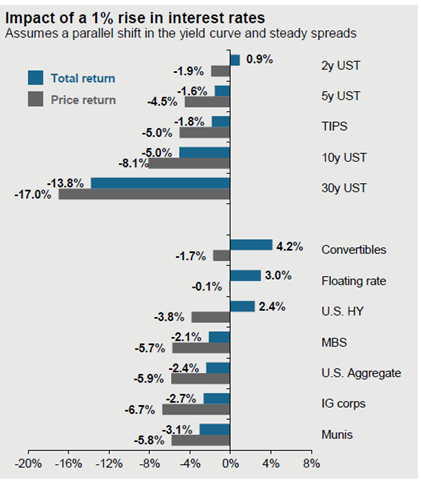

Higher rates are fine

Scott Grannis explains that rising rates are not important when based upon a strong economy – not inflation. Among his collection of charts, he includes a comparison of real yields to real GDP growth. His conclusion is that 5-year TIPS could have a yield of 2.5% with inflation at 2% and the 10-year Treasury note at 4-5%. Most would be very surprised by this conclusion, no matter how logical.

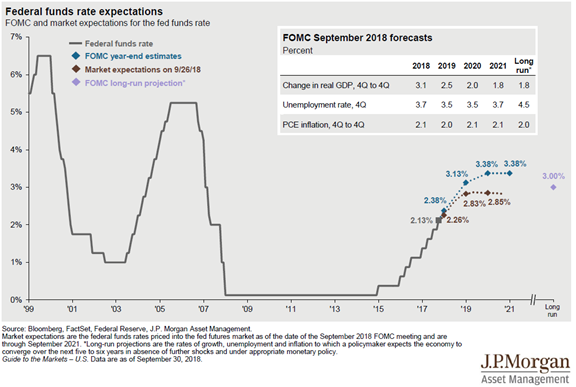

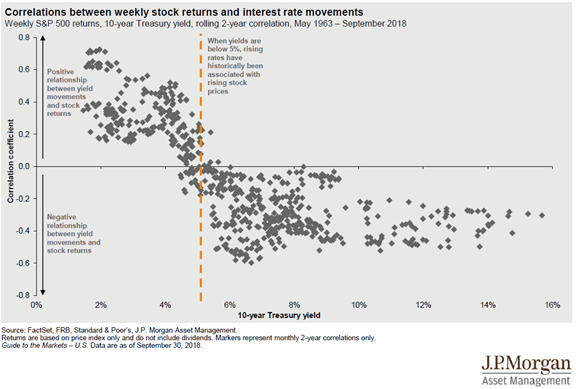

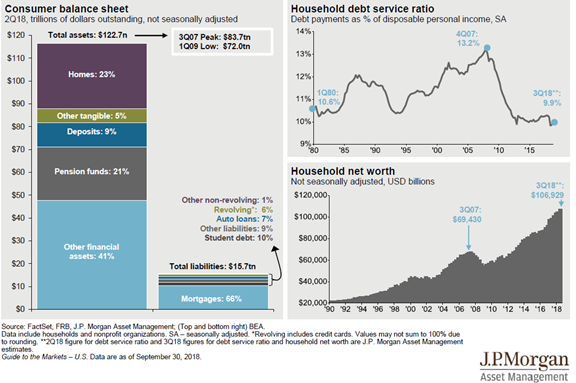

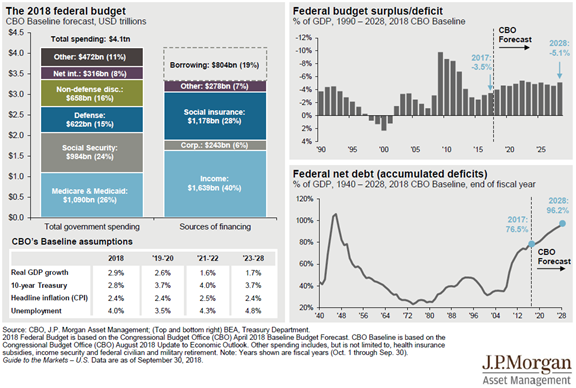

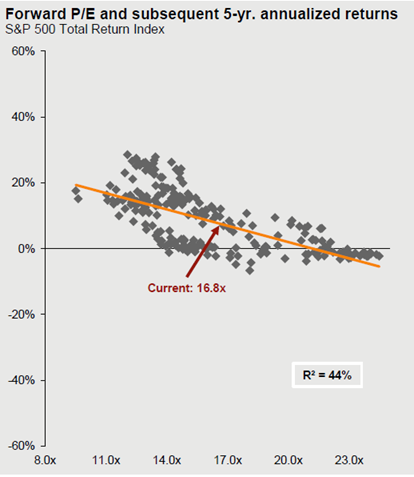

JP Morgan Charts

As noted in the Quant Corner, this is a terrific resource. Take some time to study the entire collection of charts. I have focused only on those most relevant for today’s post.

First, how much of an increase should we expect?

What is the effect of rate increases on stocks? Supportive of rising stock prices if yields are below 5%.

What about the debt concerns? Not that bad for consumers.

Not that good for government.

Earnings expectations suggest continuing solid market gains for five years.

The psychology of rising rates might be surprising. I doubt that many expect the value of their 10-year Treasuries to fall by eight percent with a 1% increase in rates.

In today’s Final Thought, I’ll add a few of my own observations.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

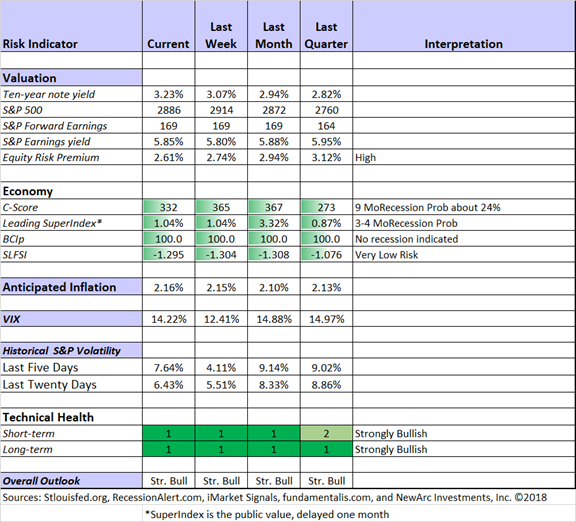

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

Short-term trading conditions continue at highly favorable levels. Actual volatility remains very low. While many argue that the low VIX level is a sign of complacency, it remains higher than realized volatility. Options traders “selling volatility” are making money. The 3% yield has been solidly surpassed, leading to questions about how high it can go.

My team has been working on the historical indicator snapshot project. I’ll try to post something soon.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Georg Vrba: Business cycle indicator and market timing tools. None of Georg’s indicators signal recession. Here is the latest chart on the Business Cycle Index.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis. It is time for an update of their key summary of theBig Four economic data points.

Guest Commentary

New Deal Democrat exposes the poor reporting of last week’s auto sales data. Essentially, some were doing a year-over-year comparison of the Florence-affected period now with the post-Harvey effect of last year. One serves to depress sales and the other to increase them. Some sought to use this as a recession indicator.

Michael Batnick examines warnings about market breadth and divergences. Here is the key quote:

The average stock is currently 12% off its 52-week high. It feels like I’ve run this number a half dozen times over the last few years when the bad breadth conversation comes up, and the numbers today are consistent with what I’ve seen in the past. Of course, this is anecdotal, and the current edition could be the one that resolves itself to the downside, but every negative divergence over the last few years has proven to be a false alarm.

With the median S&P 500 stock just 10% off its 52-week high, we’re hardly at the stage where small stocks are crashing and the weakness is hidden by a handful of giant stocks.

The new JP Morgan guide to the markets has been released. I was included in a webinar for advisors where many of the highlights were discussed. BTW, a pre-webinar poll showed that concern about a market correction led the concerns of our clients. Astute reader who sit back for a while and look at the data will be less concerned. I have sprinkled some of the most important charts throughout this post.

Insight for Traders

Check out our weekly Stock Exchange post. We combine links to important posts about trading, themes of current interest, and ideas from our trading models. This week we discussed the impact of breaking news – opportunity or noise? We shared advice by top trading experts and discussed some recent picks from our trading models. Our ringleader and editor, Blue Harbinger, provided fundamental counterpoint for the models, all of which are technically-based.

We have been getting good results from the models. Since the gains are short-term, the treading may be suitable for adding some octane in a retirement account. Check out the weekly post (including results) and write to us at main at newarc dot com if you want more information or a portfolio consultation.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility.

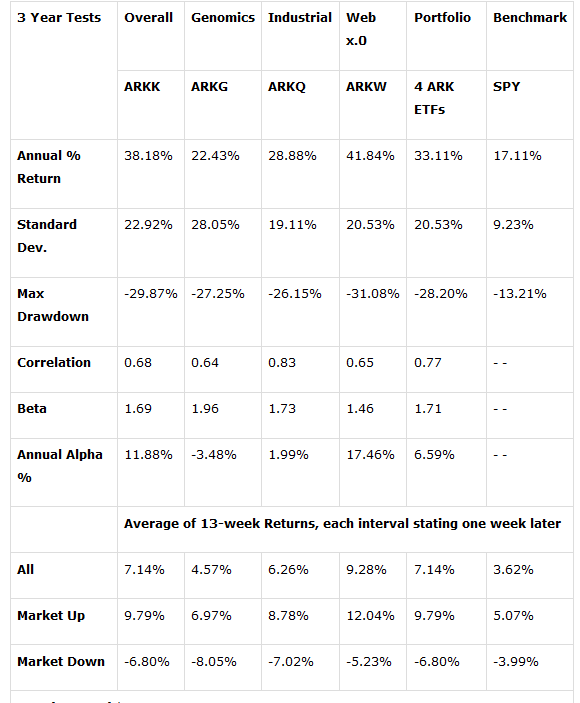

Best of the Week

If I had to pick a single most important source for investors to read this week it would (once again) be the work of Marc Gerstein. He takes a difficult topic of widespread interest. He analyzes it carefully, explaining each step. The result is not a recommendation, but an analytic result you can use for your own decisions. This is a model for other analysts and writers.

His topic is how to invest in disruptive innovation, using the ETFs from ARK Invest. They provide four actively-managed ETFs focused on genomics, industrial innovation, web x.o, and a generalized concept of innovation. How have they done?

This is just the beginning. Marc goes on to make comparisons with emerging biotechs and the overall market. He carefully navigates the waters when earnings are non-existent – a typical case for emerging companies. Instead he summons data about sales, sales growth, and book value. A key question is growth.

“The historical and projected growth rates for the ETFs are a lot higher than for the S&P 500. That’s to be expected given the nature of the businesses in which these funds invest. But compare the projected growth rates with the historical numbers (particularly Sales, which tends to be less prone to the accounting impact of odd events)”.

He next turns to gross margin and operating margin, a good way to judge both current status and potential. There are several more indicators, but you need to review this for yourself. If you do, my guess is that you will add at least one of these to your portfolio. I am taking a close look for our aggressive program.

Stock Ideas

Chuck Carnevale provides a lesson about earnings as the driver of total stock returns and of dividend growth. These are important distinctions which many get wrong. This post deserves a careful reading for appreciation of the examples.

Concerned about the effect of interest rates on high-yield stocks? You should be! Blue Harbinger screens 100 that have recently sold off, identifying five attractive candidates. In another post, Mark provides a full analysis of Triton (TRT), one of the five identified in the screen.

Colorado Wealth Management provides a lesson in choosing between preferred shares and baby bonds.

Have an interest in Brazil? DM Martins Research analyzes Brazil air carrier Azul (AZUL), describing the effect of the upcoming election on a well-operating company. Here is a broader overview of Brazil and the Presidential election.

RoseNose explains her selection criteria along with an update and analysis of the portfolio. This is always interesting, providing many ideas.

Barron’s thinks that “the high-yield bond market appears to be the best option for investors who need yield and can tolerate risk—at least until the next recession hits”. [I disagree. It is stock-like risk for a lower return, part of the multi-year chase for yield.] Undervalued stocks?

Morningstar has a list of 28. I own four or five of them and think there are many more candidates.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich’s Asset Allocation Daily is consistently both interesting and informative. In one post last week he asked, “Are You Really a Rational Investor?” Gil’s “Thought of the Day” section is a valuable addition to his regular review of important articles, includingING’s analysis of slowing Iran oil flows.

Abnormal Returns is an important daily source for all of us following investment news. His Wednesday Personal Finance Post is especially helpful for individual investors. As always, there are many great links on various topics. I especially liked the warning about universal life from Blair duQuesnay, responding to critics of an earlier post. She provides an explanation, which she expects will have your head spinning. The key point? Hers is clearer than you would ever hear from a sales person! Meanwhile, expect that you will need to initial each page of the contract.

Watch out for…

GameStop (GME). Kirk Spano combines a traditional (and good) analysis of the company business plan and financials with his boots on the ground report. This, and the pics from his travels, make for a story that is both interesting and informative.

Interest rate sensitive holdings. Barron’s has an article on how to protect your portfolio from rising rates. The answers seem to be the following:

- Keep maturities short

- Mix in some bonds.

Beer. Boston Beer (SAM), that is. Morningstar finds that the valuation is too frothy.

Final Thought

Every time the market makes a small move we are bombarded by observers predicting the worst. It is important to remember that declines of 15-20% happen regularly and without any particular reason. No one can predict these accurately, so the average investor should learn to take advantage of the movement rather than falling for the persistent pseudo-warnings. Alan Steel calls it the Fear Economy, and reviews the history of predictions by one prominent uber-bear.

Investors can fight this psychology. It is an especially good time to remember the legendary Ben Graham’s Mr. Market allegory. If you are not already familiar with this important concept, the Wikipedia summary is pretty good. Mr. Market has some human behavioral manic-depressive characteristics:

- Is emotional, euphoric, moody

- Is often irrational

- Offers that transactions are strictly at your option

- Is there to serve you, not to guide you.

- Is in the short run a voting machine, in the long run a weighing machine.

- Will offer you a chance to buy low, and sell high.

- Is frequently efficient…but not always.

This behavior of Mr. Market allows the investor to wait until Mr. Market is in a ‘pessimistic mood’ and offers low sale price. The investor has the option to buy at that low price. Therefore, patience is an important virtue when dealing with Mr. Market.

I reviewed several of the current inefficiencies in last week’s post. Let’s update the efficiency concept a bit, since the market microstructure has changed a lot since 1949. I tried to capture the changes in my post, Trading, Fast and Slow. I identified the current process, starting with an event and ending with your evening news:

- There is a news-driven stimulus. These are all actual examples.

- There is a raid on the office of the President’s lawyer;

- One semiconductor company provides a clouded outlook;

- A tweet or an overnight speech hints at a change in trade talks;

- A news conference suggests higher (or lower) tensions with Iran or Russia.

- Traders react. Most people do not understand the basic trader approach. You often “take a leg” leaning in a direction that seems to capture the mood of the market. If it goes your way, you ride it. If not, you try to scratch it for even or a small loss. Every piece of news has a simple evaluation: bullish or bearish.

- Algorithms react. The top computer systems have learned the key words that are associated with market moves. These are even faster than the traders.

- Technical traders react. The market reaction may send stock prices through levels widely viewed as important support or resistance.

- ETFs that hold the key stocks plummet. Other companies in that ETF get slammed, even though their fundamentals are essDentially unchanged.

- Financial TV brings in the chartists, who cite the temporary breach of the 200-day moving average, the move of averages into “correction territory”—more than a ten percent decline, and the level of decline possible in a Fibonacci retracement. Take your pick!

In terms of market efficiency, we can see an important effect, one that provides opportunity to Graham’s patient investor:

Market reactions are often correct in direction, but not in magnitude.

[Are you stuck in some safe but stodgy stocks – so called value traps? We generate extra yield from such positions by selling near-term calls. If you need more income, you might want to get our free description of this method].

I’m more worried about:

- Polarization in the upcoming mid-term elections. At a time when compromise would be especially helpful on many fronts.

- Chinese hardware hacking. As Barron’s notes, this threatens the use of China in the supply change, a possible $250 B bill for US companies. And of course, more pressure on trade talks.

I’m less worried about:

- Earnings growth. Can it be a catalyst again this month?

- Finding attractive stocks. Conditions are improving for some sectors, and Mr. Market does not seem to notice. David Templeton (HORAN) notes the relative performance of small cap stocks, cyclical stocks, and defensive sectors. “Economic and company fundamentals continue to be positive and should be supportive of a favorable economic and market environment”.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits