Key points:

- The value of the U.S. dollar has climbed since April, and its rise has been one of the biggest drivers of asset performance in 2018. The stronger dollar is both a consequence of, and catalyst for, tighter financial conditions.

- The impact has been felt most severely within emerging markets (EMs), although escalating trade tensions have played a role in EM performance. As a result, EM assets have cheapened considerably year-to-date. But rising dispersion underscores the need for selectivity, in our view.

- We now see limited upside for the U.S. dollar and expect currencies to remain stable for the rest of 2018 barring a material escalation of trade risks.

- We are constructive on EM equities, with a preference for EM Asia. We see cheap EM valuations, strong earnings growth, and investor underpositioning supporting inflows and equity performance for the remainder of 2018.

Overview

The U.S. dollar’s rally, underpinned by strong U.S. growth expectations and widening interest rate differentials versus other economies, has key driver of tighter global financial conditions. The dollar is a central transmission channel for financial conditions, as well as an important measure of risk appetite. As such, softer growth expectations outside the United States in the first half of 2018 combined with the Federal Reserve raising interest rates, led to tighter financial conditions and weaker risk appetite. This impacted EM assets in particular, which, along with concerns over trade tensions, led to a selloff and investor repositioning out of the asset class. The rise in short-term U.S. rates beyond the rate of inflation has provides a nascent alternative to risky assets, and in our view has led to a longer drawdown. However, the EM selloff has slowed, the U.S. dollar has stabilized and EM valuations have cheapened, creating potential attractive entry points.

Cross-asset impact

The dollar is the nexus between asset classes. It affects borrowing costs and commodity prices, is a proxy for risk appetite, and influences global capital flows.1However, the dollar’s impact, while global, is unevenly distributed: country fundamentals also matter and are increasing the dispersion of country equity markets. For example, this year, EM countries with large financing needs, such as Turkey and Argentina, saw the greatest jump in borrowing costs and steepest foreign exchange (FX) losses. Countries with strong balance of payments saw their currencies and borrowing costs largely contained.

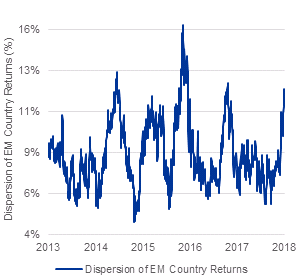

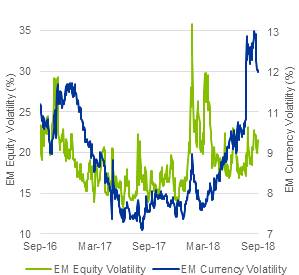

Commodity dynamics — key for many emerging markets — are also at work. Historically, oil prices and the dollar are negatively correlated. However, this year oil prices rallied alongside a stronger dollar. Commodity importers faced even tighter financial conditions as weaker currencies amplified the inflationary pass-through effects of higher oil prices. On the other hand, oil producers have reaped the benefit. For example, the MSCI Saudi Arabia 25-50 IMI Index has steadily climbed 12.1% year-to-date with little volatility, while the MSCI Turkey Index is down -49% year-to-date.2 Compared to the past five years, EM country dispersion is at its 94th percentile. Rising dispersion across EM countries underscores the importance of selectivity and the value of a country-by-country approach.

Figure 1: Currencies in the driver seat, but country fundamentals driving dispersion

Source: Thomson Reuters, CBOE, J.P. Morgan. As of September 18, 2018. Notes: The left chart measures the rolling six month dispersion of returns for countries in the MSCI Emerging Markets Index. Higher dispersion signals greater potential for country selectivity. The right chart shows the volatility of the MSCI Emerging Markets Index using CBOE’s EM VIX Index; currency volatility shown using the J.P. Morgan EM FX Volatility Index. Index performance is for illustrative purposes only. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results. Index performance does not represent actual iShares Fund performance. For actual fund performance, please visit www.iShares.com or www.blackrock.com.

Flows and positioning

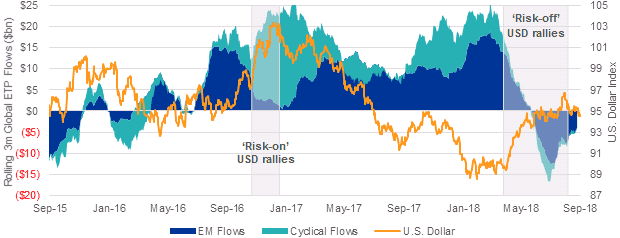

EM equity flows suggest investor positioning is now much more defensive than at the start of the year. U.S.-listed EM equity exchange traded product flows experienced their worst quarterly outflow in the second quarter since the 2013 Taper Tantrum, and the strengthening dollar shows why. EM equity flows exhibit a tight relationship with the U.S. dollar, and suggest investors are currently more concerned a stronger U.S. dollar may tighten financial conditions further. However, it is important to note that international developed market (DM) equity markets experienced similar outflows as did cyclical sectors. In other words, this wasn’t merely a retrenchment in EM positions, but a broader defensive repositioning.

EM equity outflows accelerated during June but have since rebounded. In fact, EM equity flows have since stabilized alongside EM exchange rates and higher equity prices. By mid-July, the 11 week stretch of outflows was broken and U.S. listed EM equity ETPs gathered over $2 billion of inflows.

Still, EM equity positioning is now lighter than at the start of the year. Valuations have become more attractive, while fundamentals are still intact and we believe there is limited scope for future U.S. dollar appreciation. This suggests a potentially attractive entry point for the asset class and we remain overweight EM equities. However, with dispersion rising, we maintain a preference for EM Asia.

Figure 2: EM equity flows are tightly linked with the U.S. dollar

Source: BlackRock, Bloomberg. As of September 18, 2018. Flows measure U.S. listed EM equity ETP flows. Flows are shown on a rolling three month sum. U.S. dollar is measured with the DXY index. Cyclical flows measure U.S. listed ETP flows into cyclical sectors.

Outlook

We believe EM assets currently look attractive relative to DM assets. EM equity, credit, and currency valuations suggest softer global growth expectations, tighter financial conditions, and weaker risk appetite are already reflected in current prices. Meanwhile, the U.S. dollar’s upside appears limited from here, in our view, and EM equity positioning investors looks far less crowded than at the start of the year. Trade tensions remain a key risk for investors, but with the MSCI Emerging Markets Index currently trading at 11.5 times earnings, there appears to be a fair amount of risk already priced into valuations.3

Looking out, we see the potential for global growth stabilizing in the second half. Chinese policymakers have eased monetary policy and liquidity conditions to support growth, and the ongoing technology-led capital expenditure cycle in the U.S. should continue supporting EM Asia export growth, in our view. Taken together, we find EM Asia’s attractive fundamentals, strong earnings growth led by the region’s technology firms, and currently cheap valuations attractive. With currency markets on a firmer footing and investor positioning leaning defensive against what is still a strong global expansion, the market may find itself under-invested in emerging markets given analysts expect earnings to grow 13% over the next twelve months.4

1 Note: The USD relationship with risk appetite is non-linear though, and known as the ‘USD smile.’ The USD smile theory says the USD can appreciate during both extreme risk-on periods and risk-off periods. The U.S.’s perceived safe haven status leads to dollar appreciation during heightened risk aversion, and the USD can appreciate during extreme risk-on periods, such as the fourth quarter of 2016. However when international growth is strong, foreign currencies historically tend to appreciate vs the USD, as we saw in 2017.

2 Source: Bloomberg. As of September 18, 2018.

3 Source: Thomson Reuters. As of September 18, 2018.

4 Source: Thomson Reuters, I/B/E/S. Data as of September 18, 2018. Based on the MSCI Emerging Markets Index.

© 2018 BlackRock, Inc. All rights reserved.

Read more commentaries by iShares