There are 26 constituents in the S&P 500 Communication Services Select Sector Index, but only one was on the minds of investors in late July — Facebook. A disappointing earnings release on July 25 led to a 21.35% drop in the stock’s price over the next five days.1 Because of Facebook’s outsized presence in the index, that drop had a huge effect on overall returns. The index fell 7.02% over the same time frame — and 66.11% of that loss was due to Facebook.1 This is what’s known as concentration risk. It’s a common risk that’s embedded into many indexes, but there are strategies built specifically to eliminate it.

Market-cap weighting can lead to concentration risk

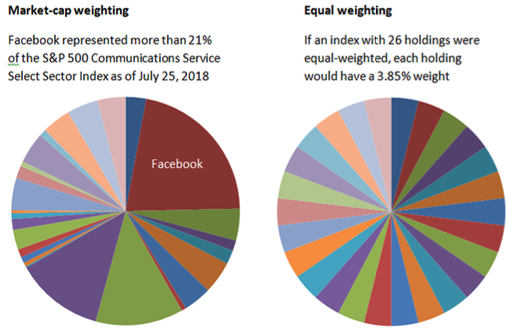

The S&P 500 Communication Services Select Sector Index has a definite concentration in Facebook — the company represented 21.73% of the index on June 25, which is why the company’s loss was so impactful.1 But why does the index hold so much of one company? Because its weightings are based on each company’s market capitalization, and Facebook had the biggest market cap of all the companies in the index. Many traditional benchmark indexes are weighted in this manner.

An alternative to market-cap weighting is equal weighting. If this index were reshuffled into an equal-weight structure, Facebook — just like each of the other holdings — would have a 3.85% weight in the index. If that were the case, Facebook’s late July loss would have had much less of an impact on the overall index. The index would have fallen 3.23% from July 25 to July 30, with Facebook representing 25.41% of that loss.1

Market-cap weighting vs. equal weighting

Examining the other side of the coin

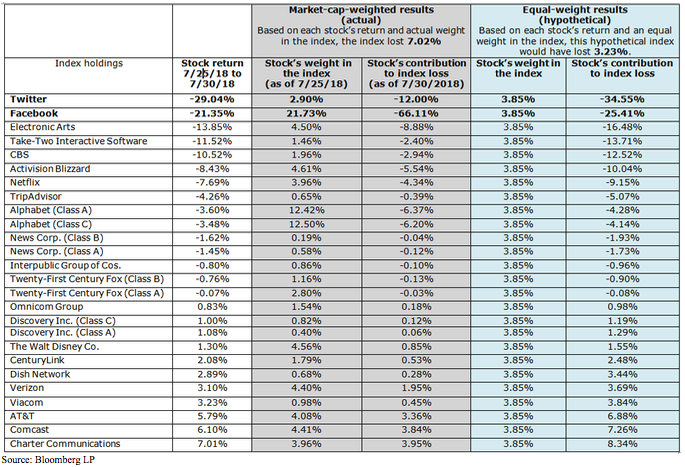

It’s important to note that there may be cases where a company’s adversity can have a larger impact on an equal-weighted portfolio than on a market-cap-weighted portfolio. Twitter is an example. From July 25 to July 30, as Facebook lost 21.35%, Twitter declined even more — by 29.04%. But, because Twitter had an only 2.90% weight in the market-cap-weighted S&P 500 Communication Services Select Sector Index, its loss had a much smaller impact on the whole (representing 12.00% of the index’s loss).

In an equal weight scenario, Twitter would have a higher weight (3.85%), and a higher impact (34.55% of the index’s loss).

Examining the effect of Facebook’s and Twitter’s July losses

Comparing the actual results of the S&P 500 Communication Services Select Sector Index with a hypothetical index that gives equal weight to the same holdings.

Key takeaway

Investors in market-cap-weighted indexes may not be quite as diversified as they think they are due to concentration risk. Equal weighting is a potential solution. Learn more about Invesco’s equal weighted exchange-traded funds.

1 Source: Bloomberg, L.P.

Important information

Blog header image: Guitar photographer/Shutterstock.com

Investments focused in a particular sector, such as communications and information technology, are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.

The S&P 500® Communication Services Index comprises those companies included in the S&P 500 Index that are classified as members of the GICS® communication services sector.

Nick Kalivas

Senior Equity Product Strategist

Nick Kalivas is a Senior Equity Product Strategist representing Invesco’s exchange-traded funds (ETFs). In this role, Mr. Kalivas works on researching, developing product-specific strategies and creating thought leadership to position and promote the smart beta equity line up.

Prior to joining Invesco, Mr. Kalivas spent the majority of his career in the futures industry, delivering research, strategy and market intelligence to institutional and high net worth clients centered in the equity and interest rate markets. He was a featured contributor for the Chicago Mercantile Exchange, and provided research services to a New York-based global macro commodity trading advisor where he supplied insight on equities, fixed income, foreign exchange and commodities. Nick has been quoted in the Wall Street Journal, Financial Times, Reuters, New York Times and by the Associated Press, and has made numerous appearances on CNBC and Bloomberg.

Mr. Kalivas has a BBA in accounting and finance from the University of Wisconsin – Madison and an MBA from the University of Chicago Booth School of Business with concentrations in economics, finance, and statistics. He holds the Series 7 and Series 63 registrations.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2018 Invesco Ltd. All rights reserved.